2 Stocks I Bought Last Month (Homebuilder Sector Analysis)

A podcast covering a boring (but profitable) sector

Reminder: these are show notes that should be read in conjunction with the podcast. Do not expect these notes to be a polished research report. Enjoy the episode and listen wherever you get your podcasts!

YouTube

Spotify

Apple Podcasts

Chit Chat stocks is presented by:

Public.com just launched options trading, and they’re doing something no other brokerage has done before: sharing 50% of their options revenue directly with you.

That means instead of paying to place options trades, you get something back on every single trade.

-Earn $0.18 rebate per contract traded

-No commission fees

-No per-contract fees

By sharing 50% of their options revenue, Public has created a more transparent options trading experience. You’ll know exactly how much they make from each trade because they literally give you half of it.

Activate options trading at Public.com/chitchatstocks by March 31 to lock in your lifetime rebate.

Options are not suitable for all investors and carry significant risk. Certain complex options strategies carry additional risk. Options can be risky and are not suitable for all investors. See the Characteristics and Risks of Standardized Options to learn more.

For each options transaction, Public Investing shares 50% of their order flow revenue as a rebate to help reduce your trading costs. This rebate will be displayed as a negative number in the “Additional Fees” column of your Trade Confirmation Statement and will be immediately reflected in the total dollars paid or received for the transaction. Order flow rebates are only issued for options trades and not for transactions involving other assets, including equities. For more information, refer to the Fee Schedule.

All investing involves the risk of loss, including loss of principal. Brokerage services for US-listed, registered securities, options and bonds in a self-directed account are offered by Open to the Public Investing, Inc., member FINRA & SIPC. See public.com/#disclosures-main for more information.

Show Notes

These are show notes written by Ryan in conjunction with his report on homebuilders for this week’s podcast - Brett

What got you interested in looking at the Homebuilding industry to begin with?

A couple of months ago, we took a look at an investor named Norbert Lou. And Norbert Lou has this now very famous writeup on Value Investors Club about NVR.

He made a huge bet on NVR in the 90’s and held it for almost 20 years. That investment ended up basically being the only success he ever needed. He had several other successful investments, but none were better than NVR.

And when you look back at that NVR writeup, it really checked all the possible boxes you’d want in an investment. It generated good returns on capital, it had some competitive advantages in its local markets, it had room to further deploy that capital, management seemed sensible, there was very little chance of disruption from technological innovation, and the valuation was dirt cheap.

So I just thought homebuilders could be a place to find some durable companies.

2nd thing that attracted me. I have been a big believer that we were going to have some sort of a crash in housing prices (and we actually did to some extent), so I would have thought homebuilders were screwed. And yet, most homebuilders actually saw continued strength in demand. So I think they’ve weathered a pretty important test (not over yet).

That made me want to dig into a couple of homebuilders.

So here are the three I’ve researched:

NVR

D.R. Horton

Dream Finders Homes

What do homebuilders actually do?

I’m going to steal a quote from my friend Drew at Speedwell Research, because he describes homebuilders (most homebuilders) really well.

“Referring to homebuilders as “homebuilders” can be a bit of a misnomer because they don’t actually build homes. Instead, they outsource to a network of subcontractors who are responsible for building the homes. Thinking of homebuilders as “home coordinators” would perhaps be more apt as their role is to vet subcontractors, order home designs, locate desirable land, procure materials, oversee the building, provide capital, and then find buyers.”

Now certain homebuilders (typically the larger ones) will do some of the manufacturing themselves. NVR for example has some manufacturing facilities that prefabricate walls, build trusses, and do millwork.

But for the most part, homebuilding is a relationships business. Do you have good partners and subcontractors that you can rely on in your area? Most of the scaled players do.

Explain land options vs. the raw land strategy: Why is it bad to have land on your balance sheet if you’re a homebuilder? Why doesn’t everyone use land options?

One thing that has become more common over the years, I think largely because of the success of NVR, has been the “land-option model”. This means that instead of going the traditional route of acquiring large plots of land and holding that land on your balance sheet while you develop homes on it, you would instead purchase an "option" on the land.

This typically means you pay 5%-7% of the land value upfront and then could exercise the right to pay the remainder once the lot was finished and you found a buyer. This model is considered “asset-light” as it keeps the inventory off of your balance sheet, which helps during market downturns. However, there is a caveat here.

You (as the homebuilder) have to have a partner that’s willing to hold the land. As far as I know, not all homebuilders have access to that. The other part, is I believe in some agreements, you’re paying the land bank or whoever your partner is, interest for their willingness to own the land. So it’s also important to get the homes assembled and sold as quickly as possible. That’s where certain companies really differentiate themselves.

So why is it bad to have land on the balance sheet? Well land, at best, probably appreciates 3%-4% a year in value. And it’s not earning anything just sitting there. And even though people probably wouldn’t think of land as a volatile asset, it can really swing depending on the overall housing market. I’ll use the founding story of Dream Finders Homes as an example here.

Patrick Zalupski, who is the founder of DFH, started the company in 2008 right in the heart of the housing crisis. He took out a $200,000 loan from the Clay County Housing Finance Authority to help build affordable homes. With the loan, Zalupski bought 3 homesites in the Jacksonville area for ~$25,000 a piece. Pre-GFC, that land was going for $80,000 a plot. So, yes, there can be huge swings. And you’d have to write down the inventory value on the balance sheet which would really hurt your GAAP earnings.

Now my first thought when I heard of this was why doesn’t the whole industry do this now? Well, for one, you have to have a partner that’s willing to hold the land. I don’t know if that’s really that easy to find. Secondly, you can probably acquire land for cheaper using a bulk land-buying strategy. And some managers think it’s worth the risk or they think they can buy and develop the land at a lower cost than others. So not everyone does it.

Why are the big builders well positioned? What competitive advantages do they have?

I think this is an underappreciated aspect of the homebuilding business.

When you are one of the largest players (D.R. Horton, Lennar, NVR, PulteGroup) you have a real advantage in your costs vs. the little guys.

You can buy your land cheaper/better: You can buy bigger plots, get bigger discounts for buying more plots, and you are probably more likely to have land bank partners that are willing to help you option the land.

They get better rates from subcontractors: Think about it from the subcontractors’ POV. You can go from house to house to house with little to no downtime. You can bring all your materials to one place. It’s like an assembly line.

Your materials are cheaper per unit: Ed Wachenheim used this example when talking about DR Horton. He said “Horton buys its appliances from Whirlpool. They are now buying 90,000 dishwashers a year. They used to buy 30,000 or 40,000. They're getting a better price.”

And then there are the generic scale advantages as well. You can spend more money on marketing, you have cheaper access to capital, more resources, etc.

Let’s go through each business. I’ll finish with the two I actually own:

NVR

NVR really pioneered the land-option model. They are a homebuilder in the DC metro area that went bankrupt in 1993 and emerged from bankruptcy with this totally new model.

I’ve already talked a bit about them, but they are the 3rd largest homebuilder in the United States by market cap. They sell single-family homes primarily in the northeast, but they’ve got some operations elsewhere.

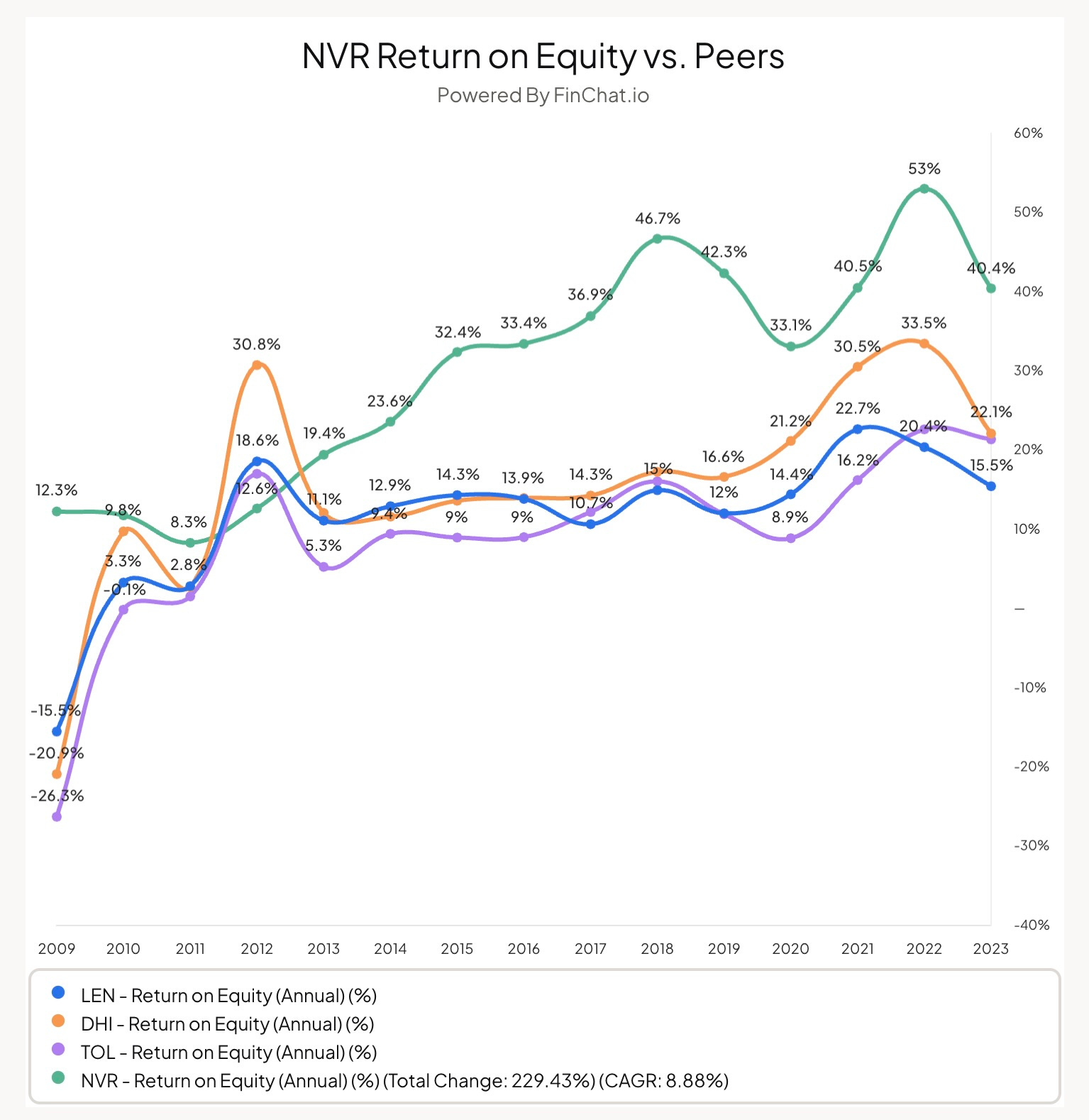

Because they are a purely land-option model, they’ve been very resilient over the last 3 decades. They were the only public homebuilder that was profitable throughout the entire GFC. But that’s not the only part that’s unique about them. They also have the highest inventory turns of any public homebuilders. So they generate significantly higher returns on equity than pretty much everyone else.

10-yr EPS CAGR: 25%

EV/EBIT: 12x

D.R. Horton – Explain the operations and the financials of the business:

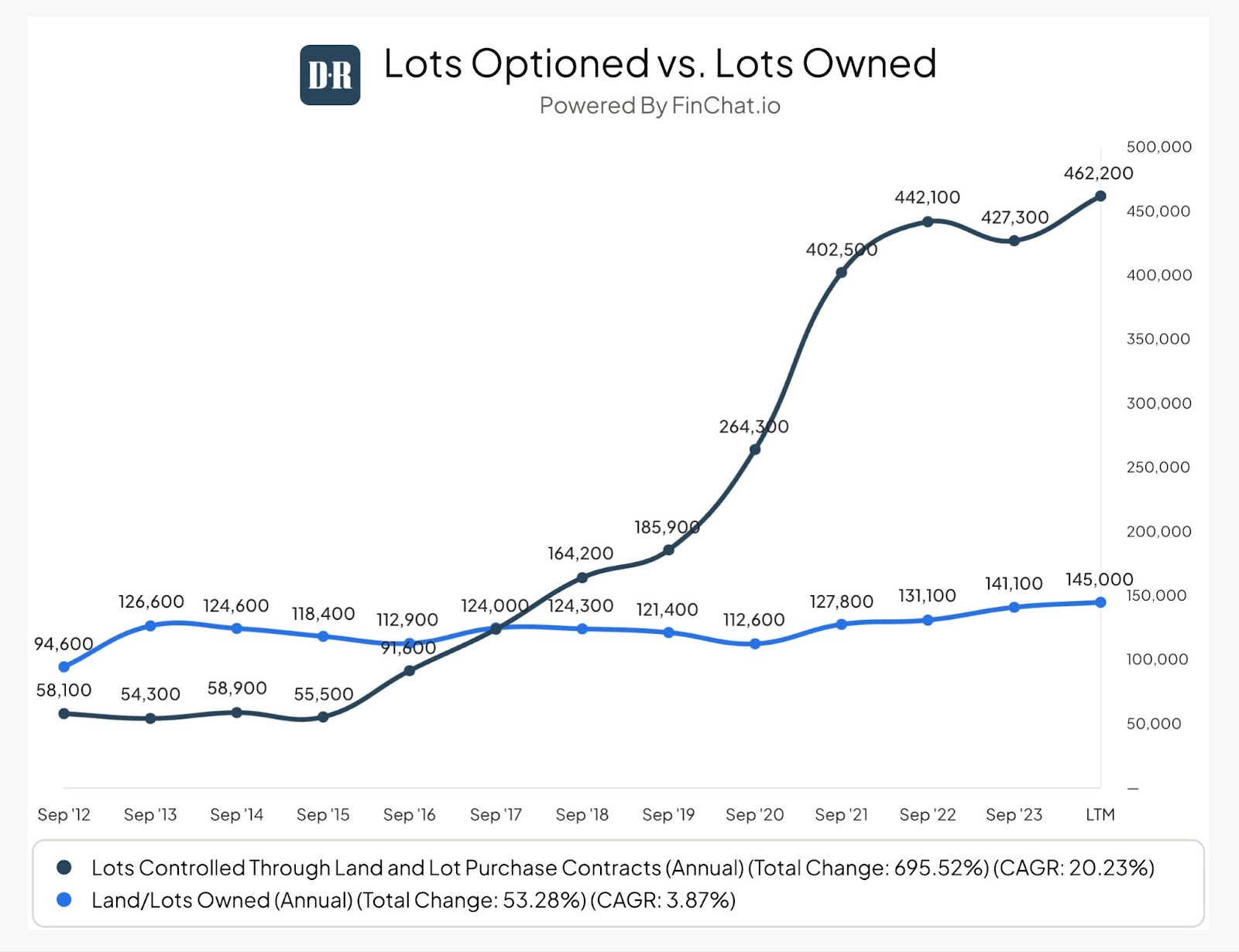

DR Horton is the largest homebuilder in the US by volume. Last year they closed 85k homes.

And they sell primarily entry-level homes (70% of their homes are below $400k). They sell in 33 different states, but 50% of their volume comes from the south-central and southeast, so Texas to FL.

D.R. Horton is one of the businesses in the industry that has really undergone the most change. They have largely pivoted from a land-heavy model to this newer asset-light model. And that (along with improving inventory turns) has really helped them grow their returns on equity over the last decade.

Over the last 5 years, DR Horton has averaged a 27% return on equity. Meanwhile, their Net Debt to EBITDA has shrunk from 3.3x in 2014 to 0.4x.

So it has been a pretty sizable business model shift. This has given them real cash flow that they can now put into buybacks, and that’s exactly what they’ve been doing. Over the last couple of years, they’ve accelerated the buyback program a bit, reducing share count by ~3% a year.

10-yr EPS CAGR: 27%

EV/EBIT: 9x

Dream Finders Homes

Dream Finders Homes is by far the smallest of the bunch that I’ve considered, but they’ve grown faster than pretty much any homebuilder I’ve come across.

Like DR Horton, Dream Finders Homes sells primarily entry-level homes and first-time move-up homes. But they’re a little more concentrated than the others. They really focus on the east/southeast, with their roots being in Jacksonville, FL.

And it’s got a bit of a unique founding story. I mentioned that Patrick Zalupski started with that loan. But he literally didn’t have enough money to buy the land outright when he made the purchase of those 3 plots, so he arranged a deal with the land owner at the time where he would buy all of it once he had actually sold the home. That was the beginning of their asset-light model.

Since that time they have expanded rapidly. Home closings have grown by 60%+ annually since 2008. Last year, they closed on just over 7k homes and earned just under $300 million in net income.

Now here’s the interesting part. Why have they grown so quickly? Well, I think it’s largely a choice. They choose to invest most of their cash flow into new land options. And part of this is in new, less established markets like what they’re doing in Denver.

They generate some top-notch returns on equity (30%+), so they’re betting on themselves to successfully expand. And, they’re taking on slightly more leverage than some of the others to do it, but if it pays off, there could certainly be some big returns.

It helps to know that Patrick Zalupski, the CEO and founder, is in his early 40’s and owns 65% of the shares outstanding.

5-yr Revenue CAGR: 50%

EV/EBIT: 10x

What are the risks:

Dream Finders Homes has some risks that I think are specific to them, but I’m probably more concerned about the macro environment.

Everyone already knows that mortgage rates jumped from 3%-8% in quick succession. That didn’t hurt demand quite as much as anticipated. However, part of the reason for that is because existing home supply dropped. People didn’t want to move and take on a new mortgage at that higher rate, so the demand that was there was more skewed to newly built homes.

If people start moving out of their existing homes and those start to come online, there could be more options for buyers and that could potentially hurt ASP’s and order volume. That would obviously hurt lots of homebuilders.

With DFH more specifically, there have been lots of reports about bad build quality. That could eat away at them a bit, and they’re more levered, so they could be at a bigger risk if there were a downturn in demand for their homes.

In summary:

“In today’s market, it seems that companies with above-average growth, high-ROEs, and good balance sheets come with the expected burden of very rich-P/Es. One industry presents the combination of 20-30% ROEs, net-cash balance sheets, double-digit EPS growth, little threat from technological disruption (or aggressive Chinese competition). And, the said industry is trading at 10x earnings”

Sources and Further Reading

NVR write-up: https://www.valueinvestorsclub.com/idea/NVR_Inc./1871818862

NVR IR page:

DR Horton IR Page:

Dream Finders Home IR Page:

https://investors.dreamfindershomes.com/