Consumer Brand Landmines

Investing in sectors where trends change frequently is by definition going to be difficult

YouTube

Spotify

Apple Podcasts

If you buy a stock, you are making a prediction about the future. Generally, I like to find companies where I can (hopefully) predict customer demand will be similar 10 or 50 years from now. That way, you only have to be right once and can buy and hold a winner forever. Easier said than done, of course.

This is why apparel, fashion, and upstart consumer brands scare me. They all seem wildly unpredictable:

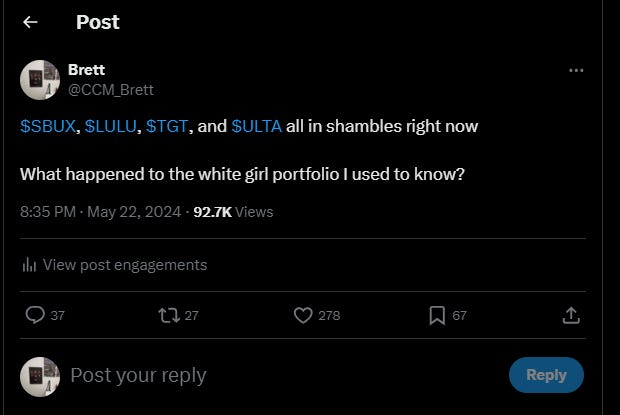

If you asked me five years ago, I would have guessed that Lululemon and Starbucks would still be firing on all cylinders today. Both are now going through major drawdowns and trailing the S&P 500 over the last five years.

Elf Beauty is taking a huge share from legacy players like L’oreal.

Dutch Bros and whatever else are eating share from Starbucks (Dutch Bros is too small to be the whole culprit, but clearly Starbucks is losing share).

Decker Outdoors is up 500% in the last five years because of the rise of Hokas and the resurgence of Uggs. Tell me you could have predicted this.

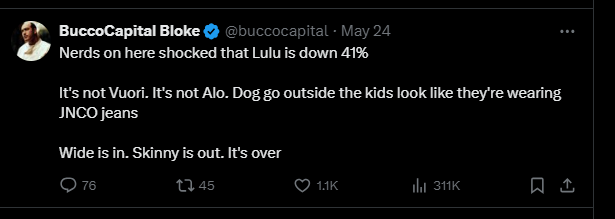

Alo and Vuori are growing quickly and young women are now wearing baggy pants:

I don’t think any of this is in my circle of competence. There is no rhyme or reason to finding the next trendy apparel/consumer brand stock. And if you have some semblance of skill here, you have to make a ton of decisions in order to succeed. You have to buy at the right time, sell at the right time, then find a new idea and repeat the process.

I’d rather find one idea with durability and hold it forever.

My recommendation: investors should generally stay away from something where the entire moat is “the brand.” There has to be something else to get you excited. And if you want to mess with these stocks, stay within an area you actually understand.

I’m speaking to the 90% of our listeners who are dudes: do you really think you can predict women's fashion trends and consumer habits? Is that the game you want to be playing?

Today, Lululemon looks cheap. It trades at under 20x earnings and will reward shareholders if revenue can keep growing at a double-digit rate. I have no clue if it will, though. None whatsoever.

Why would I buy Lululemon over American Express at similar earnings multiples when the latter has a much wider moat and much longer durability in the consumer’s mind? That’s a game I’d rather play, because I think I can win.

This is why I like looking at grocery stores and restaurants. These companies have more than just a brand driving them and have shown much more durability — on average — over the last hundred years compared to other consumer retail niches.

Or, why studying luxury businesses can be insightful:

Brand “moats” are the weakest moats. Typically, successful brands have another competitive advantage that allows them to generate outsized profits with much more security. The most successful brand ever (Apple) has multiple advantages.

I’ve seen a lot of investors struggle to make bets on consumer brands. Hopefully, we can learn from them. I think these people are getting into trouble because they are stepping outside their circle of competence (unknowingly) and buying narrow moat stocks that they think have wide moats.

On average, this seems like a recipe for failure.

Chit Chat stocks is presented by:

Public.com just launched options trading, and they’re doing something no other brokerage has done before: sharing 50% of their options revenue directly with you.

That means instead of paying to place options trades, you get something back on every single trade.

-Earn $0.18 rebate per contract traded

-No commission fees

-No per-contract fees

Options are not suitable for all investors and carry significant risk. Option investors can rapidly lose the value of their investment in a short period of time and incur permanent loss by expiration date. Certain complex options strategies carry additional risk. There are additional costs associated with option strategies that call for multiple purchases and sales of options, such as spreads, straddles, among others, as compared with a single option trade.

Prior to buying or selling an option, investors must read and understand the “Characteristics and Risks of Standardized Options”, also known as the options disclosure document (ODD) which can be found at: www.theocc.com/company-information/documents-and-archives/options-disclosure-document

Supporting documentation for any claims will be furnished upon request.

If you are enrolled in our Options Order Flow Rebate Program, The exact rebate will depend on the specifics of each transaction and will be previewed for you prior to submitting each trade. This rebate will be deducted from your cost to place the trade and will be reflected on your trade confirmation. Order flow rebates are not available for non-options transactions. To learn more, see our Fee Schedule, Order Flow Rebate FAQ, and Order Flow Rebate Program Terms & Conditions.

Options can be risky and are not suitable for all investors. See the Characteristics and Risks of Standardized Options to learn more.

All investing involves the risk of loss, including loss of principal. Brokerage services for US-listed, registered securities, options and bonds in a self-directed account are offered by Open to the Public Investing, Inc., member FINRA & SIPC. See public.com/#disclosures-main for more information.