Is Airbnb in Turmoil?

People "hate" the company. Local governments work to suppress it. They just keep growing.

YouTube

Spotify

Apple Podcasts

Airbnb is a company I would love to own. Obviously, at the right price.

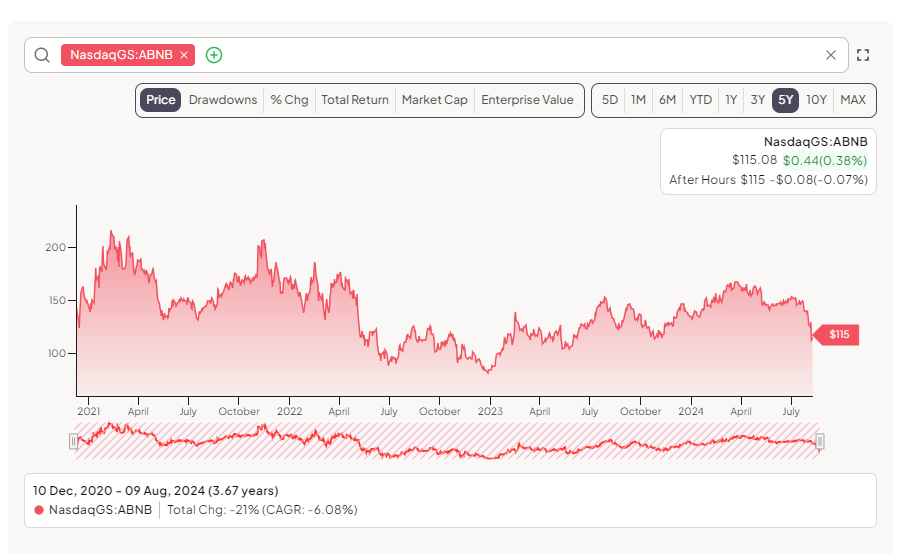

That “right price” got a little closer this week:

All charts from our friends at Finchat.io. Check them out!

The stock fell after management discussed shrinking lead times and slowing growth in North America. Shrinking lead times mean people are not willing to throw out money for vacation rentals until closer to the vacation date.

Investors didn’t like this, so the stock fell.

Bookings keep growing. Over the long term, Nights and Experiences Booked have grown at north of 20% per year. Growth has slowed down to closer to 15% post-COVID and 9% year-over-year last quarter.

Gross Booking Value (GBV, dollars flowing through Airbnb) has grown at a 30% rate since 2015 despite a pandemic:

I think Airbnb is a great business:

Persistent above-average growth

Founder-led who is focused on a “mission” as well as profits/shareholders

A widening moat that is easily trackable. The more supply listed on the platform, the harder it is to replicate. The more customers spend on Airbnb, the more valuable it is to that supply. A network effect that can expand for a long time. Wonderful.

A brand that has become a verb

A lot of investors hate Airbnb. I am excited about this fact. My conviction that I am right is pretty high and keeps getting proven quarter after quarter.

You hear a lot of similar bear theses on Airbnb:

“Who wants to stay in someone’s home anymore? Hotels are better in every way.”

“Governments are cracking down on them. Locals hate them and will drive them away.”

“What’s stopping a host from sidestepping the platform? The business model is fragile.”

“Who wants to pay for an overpriced stay with cleaning fees after I cleaned myself?”

If you asked someone five or ten years ago, they would have the exact same concerns. And yet, the business has grown its GBV at a 30% annual clip since 2015.

Now, why is that?

My conclusion is that these bear cases are overrated and/or incorrect. Follow the numbers, not your feelings.

Airbnb is too powerful for local governments to kill them. Too many hosts rely on them for income, and too many consumers love using the platform (myself included). Similar to Visa/Mastercard/American Express, this power only grows the more money is sent through its platform.

This summer, Paris saw a huge increase in Airbnb supply for the Olympics. It helped more people attend the event without paying exorbitant hotel prices or (I’m assuming) staying far away from the city center. What a terrible company ruining the local economy!

Look, no company is perfect. But I think Airbnb is one of the best businesses in the world with a good manager. Check and check.

Now, my third item on the investing checklist is valuation. Is Airbnb cheap today?

It has a market cap of $73 billion. The company has a ton of cash on the balance sheet, but a lot of that comes from holding customer deposits. So, I will use the market cap to be conservative.

Earnings before taxes — which includes net interest income on customer deposits — was $2.3 billion over the past 12 months. This is a 22% profit margin. Given the nice net interest income dynamics and fantastic unit economics, I think Airbnb’s EBT margin can approach 30% without any herculean assumptions.

On the 22% profit margin (the actual figures), Airbnb trades at a P/EBT of 31.7. Assuming a 30% margin, that comes down to a P/EBT of 23.

I think it gets into my buy zone at a P/EBT under 20. This would require another significant drawdown from the current price of $115 and/or earnings growth, but I am willing to be patient. I like the other stocks I own better than Airbnb at current prices.

20x earnings is more than I would usually pay, but I think Airbnb has a long runway to grow its GBV, has optionality with the creative R&D/product development team, and has plenty of room for profit margin expansion.

This is one I will be keeping up on every quarter. If the narrative gets worse and worse, it might be time to take the plunge on Airbnb.

But I don’t think that day is today.

Brett

Chit Chat stocks is presented by:

Public.com just launched options trading, and they’re doing something no other brokerage has done before: sharing 50% of their options revenue directly with you.

That means instead of paying to place options trades, you get something back on every single trade.

-Earn $0.18 rebate per contract traded

-No commission fees

-No per-contract fees

Options are not suitable for all investors and carry significant risk. Option investors can rapidly lose the value of their investment in a short period of time and incur permanent loss by expiration date. Certain complex options strategies carry additional risk. There are additional costs associated with option strategies that call for multiple purchases and sales of options, such as spreads, straddles, among others, as compared with a single option trade.

Prior to buying or selling an option, investors must read and understand the “Characteristics and Risks of Standardized Options”, also known as the options disclosure document (ODD) which can be found at: www.theocc.com/company-information/documents-and-archives/options-disclosure-document

Supporting documentation for any claims will be furnished upon request.

If you are enrolled in our Options Order Flow Rebate Program, The exact rebate will depend on the specifics of each transaction and will be previewed for you prior to submitting each trade. This rebate will be deducted from your cost to place the trade and will be reflected on your trade confirmation. Order flow rebates are not available for non-options transactions. To learn more, see our Fee Schedule, Order Flow Rebate FAQ, and Order Flow Rebate Program Terms & Conditions.

Options can be risky and are not suitable for all investors. See the Characteristics and Risks of Standardized Options to learn more.

All investing involves the risk of loss, including loss of principal. Brokerage services for US-listed, registered securities, options and bonds in a self-directed account are offered by Open to the Public Investing, Inc., member FINRA & SIPC. See public.com/#disclosures-main for more information.

Great take. Bold Founder & CEO, growing Brand Value, expansion into new verticals, outstanding free cash flow margin, and constantly increasing take rate make me bullish on the stock in the medium/long run. If the regulatory noise with local governments can find a peaceful resolution, I can see some upside here. Time will tell!