Is Brett Buying Altria Group Stock? (Ticker: MO)

What will Marlboro volume declines look like over the next five years?

Reminder: these are show notes that should be read in conjunction with the podcast. Do not expect these notes to be a polished research report. Enjoy the episode and listen wherever you get your podcasts!

YouTube

Spotify

Apple

Charts

Chit Chat Money is presented by:

Potentially you! Reach out to our email chitchatmoneypodcast@gmail.com if you are interested in doing a sponsorship on our podcast network. Check out our media kit for more information.

Show Notes

What is Altria Group?

Altria Group is a sin stock conglomerate focused on the tobacco and nicotine space. It has a long history, which we’ll get to in the next section.

Smokeables: This is the largest segment and is dominated by the Marlboro brand. Importantly, Altria is only Phillip Morris USA (PM USA) and does not sell cigarettes internationally. There is also the “Black and Mild” cigar brand that is smaller but can have an impact on the financials.

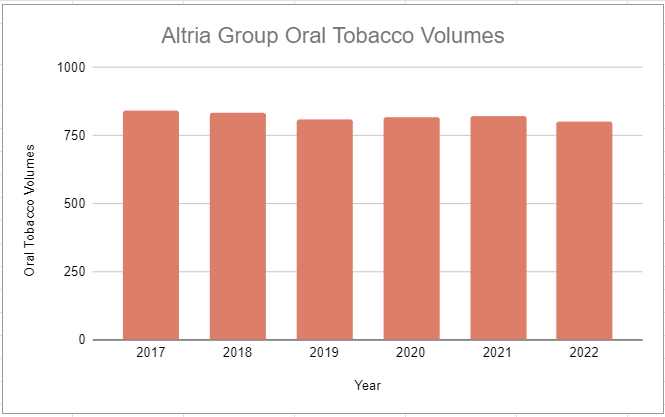

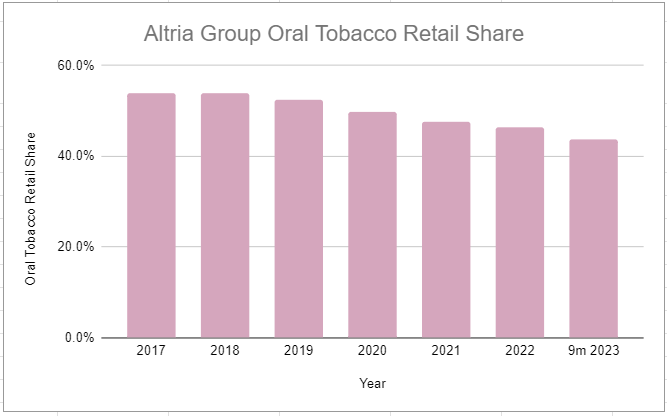

Oral Tobacco: This includes Coppenhagen, Skoal, and the On! Nicotine pouch brand. Altria has historically dominated the oral tobacco market in the United States with over 50% market share. However, in recent years that has fallen due to the proliferation of the new Zyn nicotine pouch brand, now owned by Altria’s past subsidiary Phillip Morris International. Altria’s market share is down to under 44% for this category.

Vaping: Altria has spent around $3 billion buying NJOY, its next foray into the vaping category. It previously bought a $12.8 billion stake in Juul that has now been written down to zero (zero!). With the chaos of this category, I am assuming no value here.

Investments: Altria owns 10% of Anheuser Busch and a large stake in Cronos Group. The most important of these by far is the ABI stake. We can debate/discuss on the show whether they should sell this investment. The total value of the Investments section is ~$12.5 billion by my count.

With a little cash and $25 billion in long-term debt, Altria’s enterprise value comes to around $85 billion.

Here’s how I think about the stock:

What will smokeable revenue look like five years from now?

What will oral tobacco revenue look like five years from now?

Will management be smart capital allocators? (lol)

Assign no value to vaping and other RRP initiatives

What capacity will management have to pay the dividend and repurchase stock?

Important parts of the history that led it to today:

Phillip Morris is a longstanding cigarette company. It started out over 100 years ago and has been running with the Marlboro brand for a long time.

In 2008, it spun off the Phillip Morris International business (Ticker: PM) and focused on the United States market.

In 2007, it acquired John Middleton (the cigars business).

In 2016, Anheuser Busch merged with SAB Miller, with Altria Group maintaining a ~10% stake in this conglomerate since then.

In 2018, Altria took a sizable stake in Juul Labs

In 2019, Altria took an 80% stake in Helix Innovations (nicotine pouches, subsequently bought the whole thing) and a large stake in Canadian Cannabis maker Cronos Group.

In 2021, Altria sold its wine business St. Michelle Estates.

In 2022, Altria announced a joint venture with Japan Tobacco to commercialize a tobacco heat stick product. TBD what will come of this.

In 2022, the company gave back the rights of the heat-not-burn IQOS product to Phillip Morris International for over $2 billion so PMI could operate in the United States. This change begins in 2024.

Earlier in 2023, Altria completed its acquisition of NJOY, its new vaping venture.

Those were Altria’s business decisions that led it to own the assets it has today. From a tobacco/nicotine industry perspective, there are a few important things to know.

First, the usage rate of cigarettes in the United States has steadily declined over the past half-century. However, in recent years usage of “new age” reduced-risk products such as vaping and nicotine pouches have been rising in popularity. So the volume of cigarettes has been declining at an accelerating rate, but nicotine usage has stabilized.

Second, in 1998 the Master Settlement Agreement (MSA) was signed by the four big tobacco companies, including Altria Group. This was a signed agreement that would pay the government and other stakeholders based on the harm tobacco products had on society. Here is a quote from an interview from Fortune Financial Advisors with author Gene Hoots on the deal (link in our sources below):

“It, with other supplemental agreements, provided for payments to the state governments, their attorneys, tobacco farmers, and the Food and Drug Administration, billions of dollars annually in perpetuity, based on cigarette consumption and inflation. Over a fifty year period, the total could reach $1.7 trillion. Such a staggering sum would seem to toll the death knell for any industry, but not so for tobacco. Two things happened that show its resilience. With a mere shrug, the industry was able to cover all these added costs by raising cigarette prices by only $.45 a pack, even allowing them to increase profits slightly. All tobacco companies benefitted because the MSA reduced the risk of health-related lawsuits that had plagued them for decades. But to Philip Morris’ great advantage, the MSA called for all cigarette promotion to cease, virtually locking in place the coveted market share that is the lifeblood of the industry. Since Philip Morris controlled by far the greatest market share, this stand-still arrangement benefitted it the most.”

The post-MSA environment and the rise of RRPs are the two big stories of the nicotine sector in the last 30 years. It has been fairly boring outside of this.

Where Cigarette businesses have competitive advantages:

I think nicotine businesses generally have competitive advantages. First, nicotine is addictive, which keeps consumers coming back and buying more. Second, consumers get comfortable with a specific form of nicotine consumption as well as the taste/feel of a certain product, leading to brand loyalty.

From my seat, Marlboro has the best brand in the nicotine space (talk to me in 10 years, it might be Zyn). Over decades, it built up mindshare with consumers with the Marlboro Man advertisements and stuff like that. You can’t underestimate the constant reinforcement of a quality product to an addicted customer base.

Then, government regulation led to further widening of the moat for Marlboro. Essentially, the tobacco companies are banned from advertising. This “freezing” of the market has led to minimal changes in market share in the last 30 - 40 years. Great news for Marlboro as the leading brand in the United States. It also prevents disruption risk. Who the hell is trying to build a cigarette brand these days? Nobody.

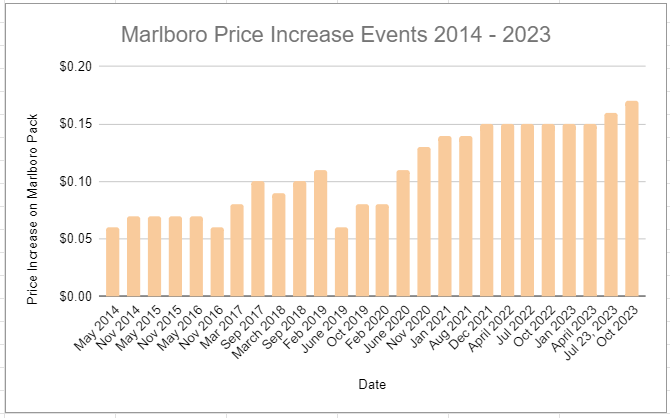

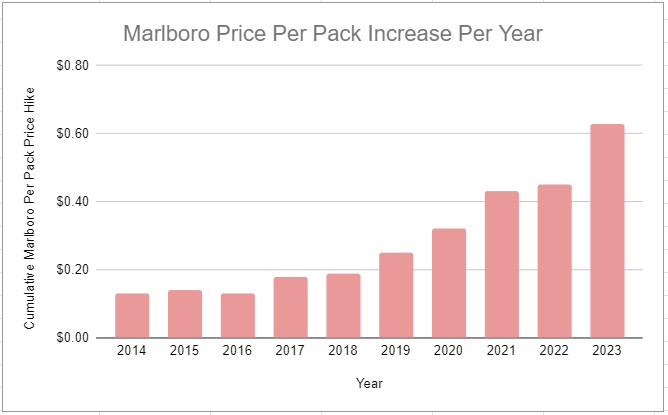

You can see this competitive advantage show up in the pricing power. Altria Group has consistently raised the price on a pack of Marlboro’s but has not seen any significant changes in market share.

The big concern shouldn’t be brand durability within the tobacco space. It should be the rise of risk-reduced products (RRPs) and management blunders.

Tobacco volume declines in the United States:

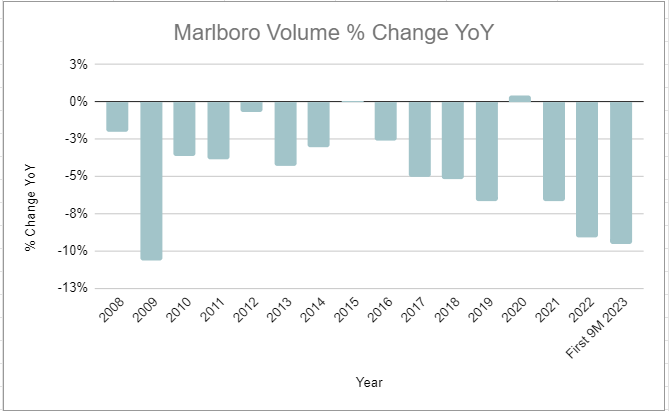

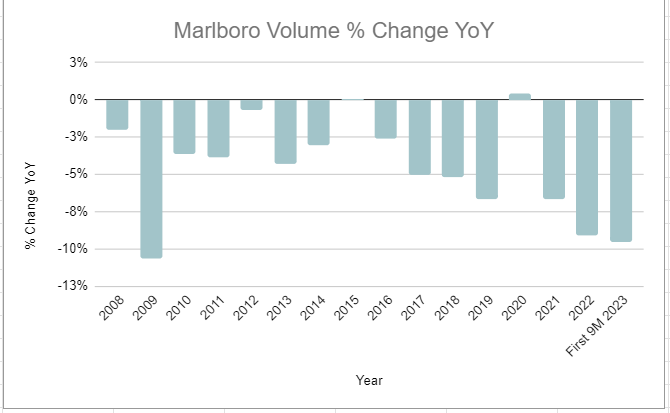

In order to value Altria stock, we need to look at tobacco volume declines in the United States and make a bet on what the rate of volume declines will be in the future. We can do so by looking at YoY Marlboro volume declines:

The concern is the change in the rate of volume declines for Marlboro. The value of this stock is materially higher if Marlboro unit volumes decline at 4% per year compared to 8%. Post GFC, it looked like you could bet on around 4% volume declines each year. Since the pandemic, we’ve actually seen a few periods at over 8% volume declines. Things have gotten worse through the first nine months of 2023.

Could some of this be due to Altria accelerating price increases in recent years? Perhaps. But I think the price increases are more of a reaction to the accelerating volume declines. In order to hit their numbers, management is getting forced to be more aggressive with price hikes. Not the end of the world (profits are actually going up, more on that later), but definitely something to be concerned about over the long term.

I think some of the declines in the last few years are due to normalization from the COVID-19 pandemic. However, some are undoubtedly due to the rise of vaping and nicotine pouches. I think an assumption of a 7.5% volume decline for Marlboro over the next five years is reasonable. I don’t think betting on getting back to 4% volume declines is smart.

Will non-smokeables create any value?

I want to be clear here. I do not assign any value to vaping. I am assigning no value to the Japanese Tobacco thing (everything else should show up in the EV). What matters after smokeables is the smokeless segment. This can be split up into traditional tobacco products and new-age products.

I think it is clear that the traditional oral tobacco business is getting crushed in the United States by the healthier tobacco-free nicotine pouches. This is why Altria’s market share of smokeless has started consistently declining. There’s no secret here, and this should continue over the next five years.

However, if Altria’s nicotine pouch business can at least maintain some market share within nicotine pouches and the company can put through price hikes. I think it is possible revenue starts to decline at a consistent rate for the overall segment despite these price hikes, with operating income also slowing due to lower margins at nicotine pouches at the moment.

This segment generated $1.6 billion in operating income for Altria last year. Not nearly as important as smokeables, but still important. I wouldn’t be optimistic about this business growing much over the next few years unless we see a fundamental change with Zyn vs. the other nicotine pouch brands in the United States.

Thoughts on this management team:

I am going to keep this short: I do not like this management team besides its focus on returning capital to shareholders. This is great, and I actually like the dividend growth target because it will keep them from wasting money.

However, they have a clear track record of getting in their own way. I am putting a $1 billion handicap from “stupidity” under my assumptions for this business each year for the next five years.

One of the key things we look for in a stock is trusting management. Since I have little trust in management I want a big discount on this stock. However, I don’t think they are shady and the business is damn good, so at the right price I think the stock is a buy.

Putting the numbers together, can the dividend per share payout grow over the next five years?

This is a bit of a unique situation. Typically, I wouldn’t want to buy a stock just for the dividend. But with the yield approaching 10%, Altria can provide solid returns if you only have confidence the dividend remains stable over the next five years.

I also want to make clear: I would only buy Altria Group in a Roth IRA (or other tax-advantaged account) and not reinvest dividends. I want to evaluate whether this can be treated as a “bond-like” equity and then use the dividend to fund other investments from businesses I think have higher quality.

Here are my assumptions for the next five years. I want to be conservative:

7.5% volume declines counteracted with price increases to keep revenue stable for smokeables

Smokeless segment sees stable revenue BUT declining margins (due to lower margins at On!)

Operating income grows by 2% per year due to the consistent margin expansion at smokeables on stable revenue

$1.3 billion spent each year on interest expense (conservatively pricing in higher interest rates)

20% corporate tax rate (no need to haggle on details, who knows what will actually be paid)

$1 billion spent on share repurchases each year, net of any stock-based compensation

$1 billion handicap for dumb management decisions per year

Rest gets spent on the dividend

Let me hit a second on why smokeables margins can easily hit something like 70% under this scenario. Altria will be doing 7.5% less volume every year, but will see no decline in sales. This means selling less of the same product than the year before, but for more money per product. Costs are not going to materially change. Excise tax risk is not going to materially change. So they will see improving unit economics and margins will likely climb higher.

Now, this is just an illustrative assumption. If we run this through the last twelve months, there would only be a $3.51 per share dividend payout capacity from free cash flow, but its actual payout was $3.80. Now, some of the rest can come from cash on the balance sheet or divestitures, but it is supposed to be a conservative assumption because I want to know what I can earn as an investor if things go poorly.

This means that even if we still run at high-interest expense, have a 20% tax rate, a $1 billion buyback, and a $1 billion handicap for management each year, the dividend per share “capacity” will still grow to $4.96 in Year 5. From Year 1 - Year 5, the stock would have a cumulative dividend per share payout of just above $20. For a stock price slightly above $40, I don’t think this is a bad deal. To me, this is a pessimistic scenario.

So what price would I buy the stock at? I’m not exactly sure. I probably need a little lower price than today, given how little trust I have in management. At $40? Maybe. But I know for a fact I am crushing the buy button at $35. So I think if it gets into the high 30’s I need to plug my nose and buy. I think five years from now I will be happy with the cash it generates for my portfolio which I can use opportunistically to buy other stocks.

Risks to watch:

For me, there are two big risks with Altria Group:

Rise of RRPs that they don’t own. It would be great if Altria could drive Marlboro users to quit while raising profits and bring them over to their own RRPs in nicotine pouches and vaping. However, British American Tobacco is leading with vaping in the United States and Phillip Morris International is dominating with the Zyn nicotine pouch. Altria has had decent success with its nicotine pouch brand but is still much smaller than Zyn. NJOY could have some success but I have no idea. What if IQOS starts gaining momentum once PMI gives it a full marketing push next year? Altria is not out of the RRP race, but it is well behind. Management has a goal of the smokefree business (including Coppenhagen, Skoal) of hitting $5 billion in sales by 2028. If the smokeables business is truly getting crushed by then, we probably have a $2.5 billion operating income business left if they can hit these goals. How much value is left? Probably not the end of the world with all the value from the dividend payments, but it would put Altria in a precarious spot.

Altria’s management making dumb decisions. It is no secret that the tobacco businesses can’t seem to get out of their own way. I would argue this is the result of the businesses being too good. They have so much cash coming in that they can’t stay disciplined and just pay dividends and repurchase stock. If they did, the TSR would look even better. I am pricing around $1 billion in value destruction from management each year, but I think that could easily be higher. The Juul acquisition was $12.8 billion in wasted money + the extra debt it laid on the balance sheet. What’s the NPV of that money when you include the value lost that could have been plowed into buybacks? A lot higher than $12.8 billion.

Sources and Further Reading

Fortune Financial Advisors: https://fortunefinancialadvisors.com/blog/discussing-going-down-tobacco-road-with-gene-hoots/

Various Invariant Substack posts:

Altria Investor Day 2023: https://www.altria.com/investors/events-and-presentations/investor-day-2023?src=topnav