Is This Restaurant Stock The Next Chipotle? (Portillo's Stock Report, Ticker: PTLO)

It has a lot of the same characteristics. But also some flaws...

YouTube

Spotify

Apple Podcasts

Chit Chat stocks is presented by:

Public.com just launched options trading, and they’re doing something no other brokerage has done before: sharing 50% of their options revenue directly with you.

That means instead of paying to place options trades, you get something back on every single trade.

-Earn $0.18 rebate per contract traded

-No commission fees

-No per-contract fees

Options are not suitable for all investors and carry significant risk. Option investors can rapidly lose the value of their investment in a short period of time and incur permanent loss by expiration date. Certain complex options strategies carry additional risk. There are additional costs associated with option strategies that call for multiple purchases and sales of options, such as spreads, straddles, among others, as compared with a single option trade.

Prior to buying or selling an option, investors must read and understand the “Characteristics and Risks of Standardized Options”, also known as the options disclosure document (ODD) which can be found at: www.theocc.com/company-information/documents-and-archives/options-disclosure-document

Supporting documentation for any claims will be furnished upon request.

If you are enrolled in our Options Order Flow Rebate Program, The exact rebate will depend on the specifics of each transaction and will be previewed for you prior to submitting each trade. This rebate will be deducted from your cost to place the trade and will be reflected on your trade confirmation. Order flow rebates are not available for non-options transactions. To learn more, see our Fee Schedule, Order Flow Rebate FAQ, and Order Flow Rebate Program Terms & Conditions.

Options can be risky and are not suitable for all investors. See the Characteristics and Risks of Standardized Options to learn more.

All investing involves the risk of loss, including loss of principal. Brokerage services for US-listed, registered securities, options and bonds in a self-directed account are offered by Open to the Public Investing, Inc., member FINRA & SIPC. See public.com/#disclosures-main for more information.

Show Notes

What is Portillo’s?

Portillo’s is a fast-casual restaurant serving Chicago-style street food. The main “unique” items are the Italian beef sandwiches and Chicago-style hot dogs. However, they also sell burgers, chicken sandwiches, and salads (according to management, the salads are wildly popular).

For sides and extras, they sell crinkle-cut fries and their “famous” chocolate cake and milkshakes. As you can tell by now, this is not a fast-casual chain focused on healthy eating. It is hardy food with an entirely different marketing spin than someone like Chipotle or Cava. They focus on saying things like Portillo’s is “crave-able” or for a fun family dinner without breaking the bank. It is somewhere one might stop for lunch during the workday for a hot dog lunch but also with the kids on a Sunday evening for a sit-down meal.

One last thing to note is that most Portillo’s have unique designs. While management is pairing back on the importance of this as they scale, Portillo’s works to serve each market they enter with unique local qualities to a restaurant. This doesn’t mean changing up the menu (it is always Chicago-style street food) but adding in something the locals will like. For example, they have Ford-related stuff in their Detroit location and Desert themes in Arizona.

Units are built at a large size to achieve high sales volumes. They offer all channels for customers including digital pick-up, delivery, drive-through, and even a catering business.

If you haven’t been to Portillo’s, you might ask: is the food even good? That was one of my main questions looking at this business. If the food is good and customers enjoy eating there, it will likely scale to all parts of the country. If it is just marginal, there are concerns it is riding off of its Chicago heritage and will struggle in other parts of the country.

I think there are a few indicators we can use to determine whether Portillo’s is considered “good” by the majority of customers:

The sky-high AUVs in Chicago and durability in that market

People pay to ship Portillo’s across the country

Huge openings in new markets + strong AUVs

More details on these factors will continue throughout this report.

Relevant history for investors today

There are three important periods for Portillo’s from an investing perspective: founding, private equity, and post-IPO.

Portillo’s began in 1963 when Dick Portillo opened a hot dog stand in Chicago. For the next few decades, the company became a staple in the Chicago area with an intense focus on serving this market (you can see the results with Chicago AUVs today).

Then, in 2000 they started nationwide shipping (yes, you can get Portillo’s delivered all around the country) and expanded to California. Only two stores remain open in California and management today admits it was a mistake to go there so early.

If you look at the chart below, the 2000s Portillo’s didn’t do much with store expansion. From my seat, it looks like a business that was thriving in Chicago where the founder and longtime management team didn’t care about getting bigger.

But then, in 2013 Berkshire Partners (not affiliated with Buffett, but cheeky name choice) acquired Portillo’s in a private equity deal. From then, they decided to grow store count across the Midwest and a bit into the Sunbelt. You’ll see details in the unit economics section, but the rest of the Midwest has not been as strong as management would have liked.

In 2021, Portillo’s went public to pay down debt and repurchase what are called “Opco Units.” Essentially, they transferred ownership from Berkshire Partners to public shareholders. From then on, they have decided to expand the unit count at a 10%+ rate throughout the Sun Belt (Arizona, Texas, and Florida).

The chart below visualizes this trend. Portillo’s was a small restaurant brand for many years (perhaps the In-N-Out of Chicago?) and now wants to go national. Can they do it successfully?

What do the unit economics for a restaurant look like? How might this change in the future?

Unit economics for an expanding restaurant concept is THE question to understand. If they are strong, it will lead to high ROIC + a huge reinvestment runway. If they aren’t, it will likely do poorly.

Porillo’s unit economics are a bit tricky. We need to separate the Chicago restaurants from the non-Chicago restaurants. Luckily, at the 2023 Investor Day, management did this for us.

First, we need to look at the two metrics Portillo’s uses to handicap itself for its restaurant-level unit economics: average unit volumes (AUVs) and restaurant-level profit margins.

AUV is defined as this:

“AUV is the total revenue (excluding gift card breakage) recognized in the Comparable Restaurant Base, including C&O, divided by the number of restaurants in the Comparable Restaurant Base, including C&O, by period”

Only stores that have been open for 24 months are included in the comparable restaurant base. Most companies will use 12 months, but Portillo’s likes to use 24 months due to the huge pent-up demand a location has in its first few months of opening (creating a huge headwind to comp sales even if the location is doing fine).

One might argue they are trying to manipulate the number but I think it is ~fantastic~ that there are already existing fans of Portillo’s across the country waiting for the opening day of a new location. Would you rather have it the opposite and each location needing to kickstart demand from a cold start? Obviously not.

This is the definition of restaurant-level margin:

“Restaurant-Level Adjusted EBITDA is defined as revenue, less restaurant operating expenses, which include food, beverage and packaging costs, labor expenses, occupancy expenses and other operating expenses. Restaurant-Level Adjusted EBITDA excludes corporate level expenses and depreciation and amortization on restaurant property and equipment”

In plain terms, it is the operating cash flow of a restaurant. One gripe is that D&A is not included here, but management says that maintenance Capex is only 10% - 15% of total capex due to the heavy growth investments they are making into new properties. I think this is a fine metric to measure the profitability of restaurants and how much firepower Portillo’s will have to pay its corporate expense and interest payments and then invest in new locations.

As of the September 2023 Investor Day, Chicago locations had:

$10.8 million AUVs

Restaurant-level margins of 31.1%

These are phenomenal numbers that generate a lot of cash flow for Portillo’s. This market is fairly saturated, and management said they will likely only open about one location in this region every year as long as a good location pops up. They are also investing in smaller pick-up locations to supplement busy areas.

In the Sun Belt in September 2023, Portillo’s had:

$6.6 million AUVs

20% restaurant-level margins

While not as good as the Chicago area locations, these are still solid numbers. Investors should remember though that the comparable store base doesn’t start until 24 months, so a lot of the new Sun Belt locations are not included here. However, the new locations actually seem to have better unit economics given management’s learnings from prior openings. It is an important number to track given that this is where the majority of new stores will be going for the next five years.

In Q1 of 2024, Portillo’s blended unit economics were:

AUVs of $9 million (up from $8.7 million a year ago)

Restaurant-level adjusted EBITDA margin of 24.2% over the last twelve months (chart below)

What have comp sales looked like historically? Are you worried about the recent slowdown?

In Q1, Portillo’s posted negative 1.2% comparable store sales. Comp sales have trended in the wrong direction for five quarters. This is a slight concern for me, but in Q1 of last year comp sales were positive 9.1%, making it a really tough quarter a year later.

Two other things for anyone worried about comp sales:

Yes, it does impact the unit economics. However, Portillo’s locations already have such strong margins it is not the end of the world if they take a slight hit. There are still positive ROICs that can do fine through a tough environment for restaurants.

A lot of restaurants are struggling with the same issue right now (Starbucks, McDonald’s). I don’t think these comparable sales developments are anything specific to Portillo’s and are not a huge concern for me unless they are negative for multiple quarters while other restaurant chains are thriving.

What improvements do you think Portillo’s can make to improve their per-store returns?

So we know the revenue/profit side of the equation. Now, let’s look at the cost of a restaurant. I am not looking at existing Chicago locations because those are already fully depreciated and need minimal maintenance Capex. They are great assets that can provide steady cash flow to the parent company.

As the management team gets more professional and goes for these new markets, it is looking to “optimize the box” to improve building costs. Portillo’s builds out all of its restaurant locations and therefore is capital intensive. They have to spend a decent amount of money upfront with the hopes of generating sold cash flows for many decades into the future.

Due to building cost inflation, the Class of 2022 locations cost an average of $7 million per location to build (graphic below). However, with $8 million in AUVs and 20% restaurant-level margins, these locations are still producing 23% cash returns each year. Not a bad ROIC.

With building costs coming down and a more optimized restaurant design, management thinks costs can come down to $5.5 million or lower for future locations. This would bring the cash returns to ~30% per year if AUVs and margins can remain stable. Even if this is not achievable, the unit economics are strong.

The big question is: Will these unit economics stay the same as they move nationally? I think they can. The Arizona, Texas, and Florida locations have shown promise. While they are not as strong as the Chicago units, they can still generate AUVs in the $7 million - $8 million range with solid restaurant-level margins.

Remember, Portillo’s already has fans spread out around the country. They are clamoring for a location to open up in their city. Portillo’s also specifically chose Arizona, Texas, and Florida as states to expand first because of the current population tailwinds to these markets. I think that is a smart move.

With an impressive management team (discussed fully in the below section) making incremental improvements to their opening process, I have confidence the unit economics will remain solid over the long term. Of course, each quarter is subject to the health of the consumer, and comp sales will have some inconsistencies.

Company expansion plans and financial modeling: Are we confident a national expansion will work?

Alright, we know what a Portillo’s is and what each box generates in cash. Now, let’s look at its expansion plans and try to put together a basic financial model for restaurant-level EBITDA.

Portillo’s gives out varying estimates for how many restaurant locations it can have in the United States. Sometimes it says 800, sometimes 900 (if you include pick-up, airports, and colleges). With just 85 locations at the end of Q1, I am going to go for a round number of 500. It will be many years before they hit any of these numbers anyway.

What is important is that there is a lot of room to grow the supply of Portillo’s restaurants around the country.

Management believes it can grow its locations at 10%+ a year, achieve slightly positive comp sales growth (remember Chicago vs. Sun Belt headwind), and hit 22% restaurant-level margins.

This is a fairly simple model. I ran some estimates to see what this could spit out from restaurant-level profitability in the future.

Assuming:

10% unit growth

$8 million AUVs that start growing at 3% from 2026 onward (as Chicago becomes less relevant, AUVs might fall. It is hard to pinpoint exactly what my starting estimate should be here)

22% restaurant-level margins

$7 million per new location build cost

Portillo’s will generate $1.66 billion in restaurant-level profits from 2024 - 2030. Its new restaurants will cost $558 million to build. So, it will have approximately $1.1 billion in cumulative cash flow to help pay G&A, interest expense, debt principal payments, and other corporate/overhead costs. Or, it gives them room to increase the unit count growth.

If we expand a 10% annual unit growth to 2035, it will generate $2.87 billion in cumulative cash flow after including new build costs.

By 2035, it should have around 264 locations. This is still around half of my conservative estimate of a 500-location saturation across the country, and much less than half of management’s 800-location assumption.

The fact Portillo’s has a chance to grow unabated for (potentially) multiple decades with strong ROICs is one of the most exciting things about this stock. Of course, the numbers could come in a lot worse than we think, but the potential for durable growth is exciting here.

Charts from our estimates

Is the balance sheet a concern?

Portillo’s runs a lean balance sheet. They had just $13 million in cash on the balance sheet at the end of Q1 2024, which is not abnormal.

The company has a variable-term loan and credit facility (the credit deal was done in tandem) due in 2028. Here are the key points investors need to know:

$300 million for term loan

$100 million for revolving credit facility ($32 million taken out right now)

“As of March 26, 2023, the effective interest rate was 8.09%”

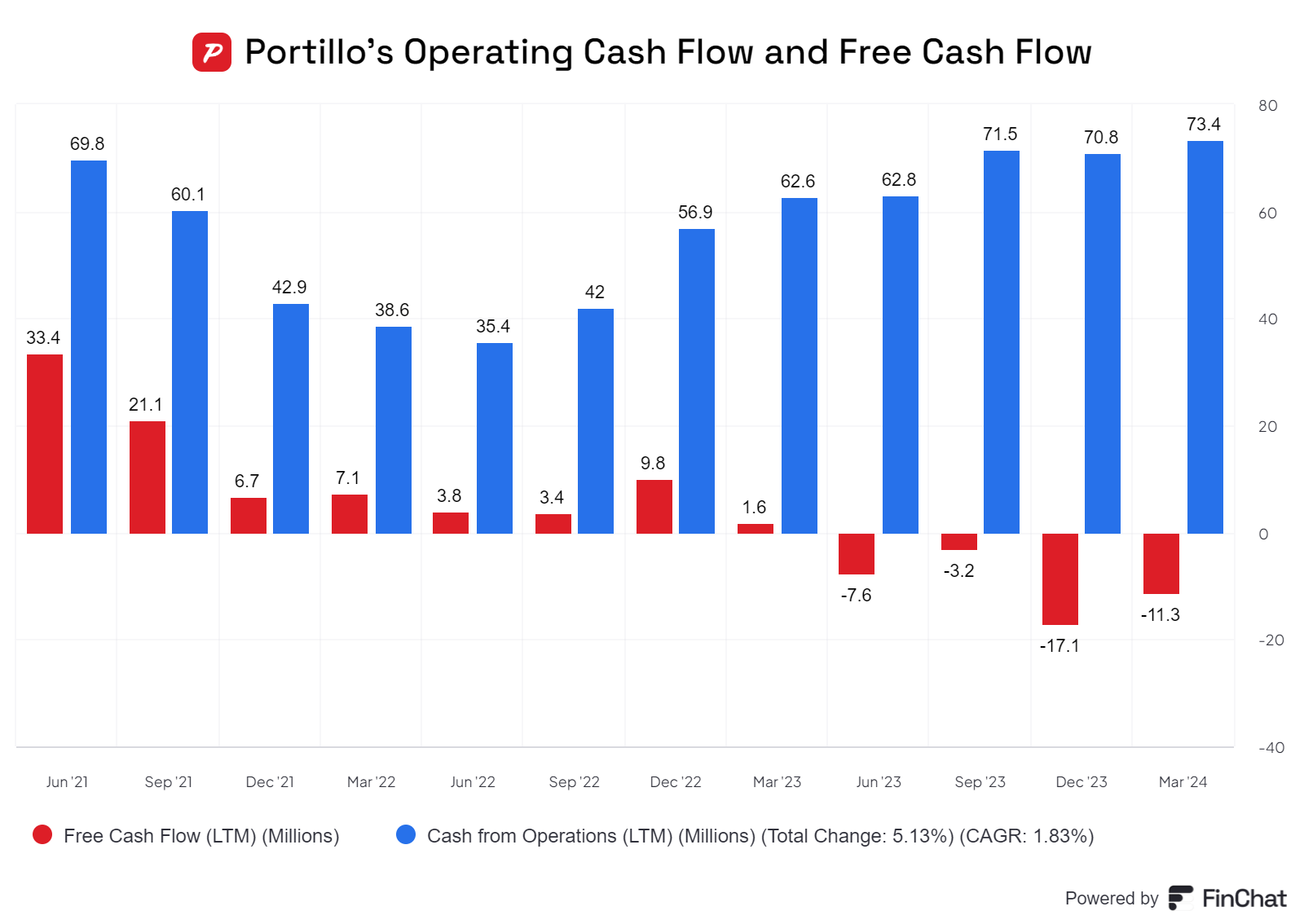

The company generates positive operating cash flow but is around break even on free cash flow. I don’t think the debt is a concern today but it is something investors clearly need to keep track of. The company wants to pour a lot of its operating earnings into more unit expansion. Eventually, it will need to pay down this debt. As they hold a small cash position, they may need to increase the usage of the revolving credit facility in order to finance unit count growth.

This makes the profitability and cash generation from these new builds vital.

Part of me would like them to pay down this debt when they can. Make the balance sheet cleaner and eliminate the interest expense. However, given the PE background, that may be wishful thinking.

Overall, the balance sheet is perhaps a yellow flag for me. I don’t mind an efficient balance sheet for companies that are consistently profitable. However, a low cash position combined with aggressive unit expansion adds some uncertainty.

Thoughts on the management team and ownership: can this box be checked?

I want to look at the management team, ownership, and any proxy statement concerns with Portillo’s.

After reading the transcript for the 2023 investor day, I came away highly impressed with the management team put in place here.

The CEO is Michael Osanloo. Osanloo comes from P.F. Changs, where he was the CEO of a brand with 300 restaurant locations. I think that is good for a company looking to eventually have this many locations under its umbrella.

More impressive may have been the other executives.

In 2022, they hired Mike Ellis as the Chief Development Officer. He has multiple decades of experience in the restaurant development space, recently at Cracker Barrel. He seemed very sharp to me at the Investor Day.

Quote from Ellis:

“And an example I want to give that kind of illustrates that is from our Class of 22 in Gilbert, Arizona, that's just opened and is estimated to do about $8.4 million. But as you look at Gilbert and its site characteristics and the things that makes it successful for us is we're surrounded by 1.1 million square feet of national retailers, right. So, that's going to drive people, that's going to drive foot traffic, that's going to bring people to that market. We have excellent visibility from the main street. We have great building signage. We have spaces on the shopping center pylon signs. We've got great visibility from that standpoint. I've got two access, an ingress and egress points. I can easily get in and I can get out. I've also got sufficient parking for my dining guests and we've got a great drive-thru stack which helps us efficiently operate our drive-thru. Another thing that we really liked about this market is we know through our research and our data that the national restaurants and retailers around us perform much better than their average through mass mobile data and understanding that. So, all those, all things being equal, if others are outperforming in the market, we feel we can get that same performance as well.”

The CFO joined in 2020 after working for 17 years at Domino’s Pizza. I think that is a good place to learn how to be a finance executive.

The COO joined in September 2020, and previously worked at Starbucks and McDonald’s. I think that is a great place to learn how to be a good overseer of a lot of restaurant units and getting them to run smoothly.

I came away very impressed with the COO Derrick Pratt from the Investor Day. His presentation was thorough and showed he was dedicated to improving the Portillo’s operations and understands the relationship between executives, employees, customers, and shareholders. Some quotes:

“And then we're going to talk about how we continuously monitor that right, matching up capability and demand to shape that honeymoon curve in a way that is accretive financially, long term and experientially. I'm also going to talk about our new restaurant opening, our NRO team, their capability. This team was built, right, to do simultaneous openings and it's built out ahead of our pipeline. My commitment to Michael, to our team, to our brand, to you as investors is that we will not let people development, our capability as an operating group to be a gating factor to our growth. We will stay one year, at least out in front of his pipeline from a capability standpoint”

“It cannot be hard to do our business. It has to be easier to do our business. Easier to do it right. Michael talked about all those steps back and forth, conveyance, waste, not adding value, but more importantly, it creates fatigue and delay. People will walk out. We've seen people at times look at the daunting task of operating our business and have second thoughts. We want to treat those people like gold and help them be successful.

And so, operational efficiency is important. It's about satisfying our guests because when we do that, then we have the underpinning for our people to take care of our guests, right. And it's about fulfilling the obligation we have to our shareholders.”

Osanloo owns 3.76% of the stock, so a sizable chunk. Most importantly, Berkshire Partners owns around 20% of the outstanding shares. I am not sure what their plan is, but as a PE firm that made the investment a decade ago, they will likely want to get out of the investment at some point.

The largest concern from the ownership standpoint is this tax receivable agreement they (assumingly) have with Berkshire Partners:

“Under the Tax Receivable Agreement, we are required to make cash payments to certain of our pre-IPO LLC Members (the "TRA Parties") equal to 85% of the income tax benefits”

So they have over $300 million in tax liabilities to pay to these other shareholders of the “OpCo” and will be paying $7.2 million to them for 2023 liabilities. Call me crazy, but as an outside shareholder, I am not a fan of this.

To be conservative, I have added this tax receivable liability to my enterprise value calculation.

More information:

If we look at executive compensation, it is pretty standard for a company of this size. The board gets paid too much, the executives get comped bonuses on adjusted EBITDA (75% of bonus targets according to proxy). It’s not optimal, but it’s fine.

Note: When looking at shares outstanding, the aggregators are misleading due to the exchange of LLC OpCo Units to Class A common stock. They do around $15 million in stock-based compensation per year on $700 million in revenue. SBC has come down since the IPO, which is a good thing.

While neither are screaming red flags, the balance sheet and the ownership/proxy filing give me the most concern when doing research on Portillo’s.

Is the stock cheap?

If you believe in the unit growth formula, stable restaurant-level margins, and single-digit comp sales growth, Portillo’s stock is cheap.

If I add in the debt and TRA Liability, Portillo’s has an enterprise value of $1.37 billion. It has a market cap of $736 million (fully diluted).

Through 2030, I think the company can generate restaurant-level cash flow AFTER accounting for build-out costs of over $1.1 billion. With only $78.8 million in overhead opex in 2023, I think Portillo’s can generate a good amount of excess cash flow while still reinvesting heavily to grow the business.

We will not be seeing bottom-line free cash flow for a while. Or if we do, it will be understated. But that is okay given the solid ROIC they are getting with new locations I expect to continue.

Will I be purchasing shares?

Portillo’s has made it on my watchlist. I am not certain I will be purchasing shares for my portfolio. I think there are 3 - 5 other stocks I have higher on my watchlist ranking right now (reminder to self: need to update this ranking) but I could see myself owning Portillo’s in the future. Given the reinvestment runway, there is a chance this is a 10-bagger over the next 10 years.

Do I think this is a good business? Yes. I believe they can achieve strong ROIC for many years to come.

Do I think the valuation is cheap? Yes. Looking at excess restaurant-level cash flow vs. current EV.

Do I trust the management team? Yes. However, I have some concerns on this ownership structure, the TRA liability, and how this PE investor will treat minority shareholders.

Major risks I am watching

As with all our stock episodes, I want to close with the major risks any investor should be watching for Portillos:

Deteriorating Comp Sales Growth. This means the new units in the Sun Belt are not performing as we hoped or the consumer trend away from restaurants is continuing. Either way, it would be bad news for the business especially with an “efficient” balance sheet.

Free cash flow remains negative. Portillo’s claims it is self-funding but currently has negative free cash flow on a consolidated basis. I would hope they can turn this to neutral and then slightly positive even as they invest in new restaurant locations.

Overall, I worry that this is a stock that has to “run on the treadmill” and will work really hard but not actually create value for the class A shareholders. Sure, the restaurants should generate some solid cash flow that will grow as the company grows. However, I could see the majority of this cash flow going to interest expense, debt paydown, executive payments, the TRA Liability, and BOD salaries. They certainly have been running on the treadmill ever since going public. TBD if that changes.

Thanks - this is a great primer into this popular chain. Any thoughts on Engaged Capital's recent 9.9% stake and setup into 2H24 and next year (2025)? Stock seems on the way up do you think Engaged's proposals (sale/leaseback, opening smaller stores, etc...) can bring positive value to the company and shareholders?