Nicotine, Valuations, and Patience

New podcasts, in case you missed them

Reminder: these are show notes that should be read in conjunction with the podcast. Do not expect these notes to be a polished research report. Enjoy the episode and listen wherever you get your podcasts!

Last week, I had the pleasure of interviewing Devin LaSarre — author of the Invariant newsletter — on the state of the nicotine market. If you have any interest in nicotine or tobacco, you need to subscribe:

Make sure to check out the full episode on your podcast player of choice (YouTube, Spotify, Apple, etc.) as well as all our latest episodes. We’ve done analysis on GoGo, interviews on small-cap value investing, and an overview of British investor Terry Smith. Subscribe, subscribe, subscribe. We’d greatly appreciate it (and it’s free!).

After publishing our episode with Devin and reading through Phillip Morris International’s Q1 earnings, my thoughts have further crystallized on the company.

Chit Chat stocks is presented by:

Public.com just launched options trading, and they’re doing something no other brokerage has done before: sharing 50% of their options revenue directly with you.

That means instead of paying to place options trades, you get something back on every single trade.

-Earn $0.18 rebate per contract traded

-No commission fees

-No per-contract fees

Options are not suitable for all investors and carry significant risk. Option investors can rapidly lose the value of their investment in a short period of time and incur permanent loss by expiration date. Certain complex options strategies carry additional risk. There are additional costs associated with option strategies that call for multiple purchases and sales of options, such as spreads, straddles, among others, as compared with a single option trade.

Prior to buying or selling an option, investors must read and understand the “Characteristics and Risks of Standardized Options”, also known as the options disclosure document (ODD) which can be found at: www.theocc.com/company-information/documents-and-archives/options-disclosure-document

Supporting documentation for any claims will be furnished upon request.

If you are enrolled in our Options Order Flow Rebate Program, The exact rebate will depend on the specifics of each transaction and will be previewed for you prior to submitting each trade. This rebate will be deducted from your cost to place the trade and will be reflected on your trade confirmation. Order flow rebates are not available for non-options transactions. To learn more, see our Fee Schedule, Order Flow Rebate FAQ, and Order Flow Rebate Program Terms & Conditions.

Options can be risky and are not suitable for all investors. See the Characteristics and Risks of Standardized Options to learn more.

All investing involves the risk of loss, including loss of principal. Brokerage services for US-listed, registered securities, options and bonds in a self-directed account are offered by Open to the Public Investing, Inc., member FINRA & SIPC. See public.com/#disclosures-main for more information.

If you’ve owned Phillip Morris International (PM) for the last 10 years, the results have been lacking. In fact, it has gotten much worse in the past 5 years when the stock’s total return started to greatly underperform the S&P 500:

(Courtesy of our friends @finchat.io)

I think this underperformance is set to reverse in the next 10 years.

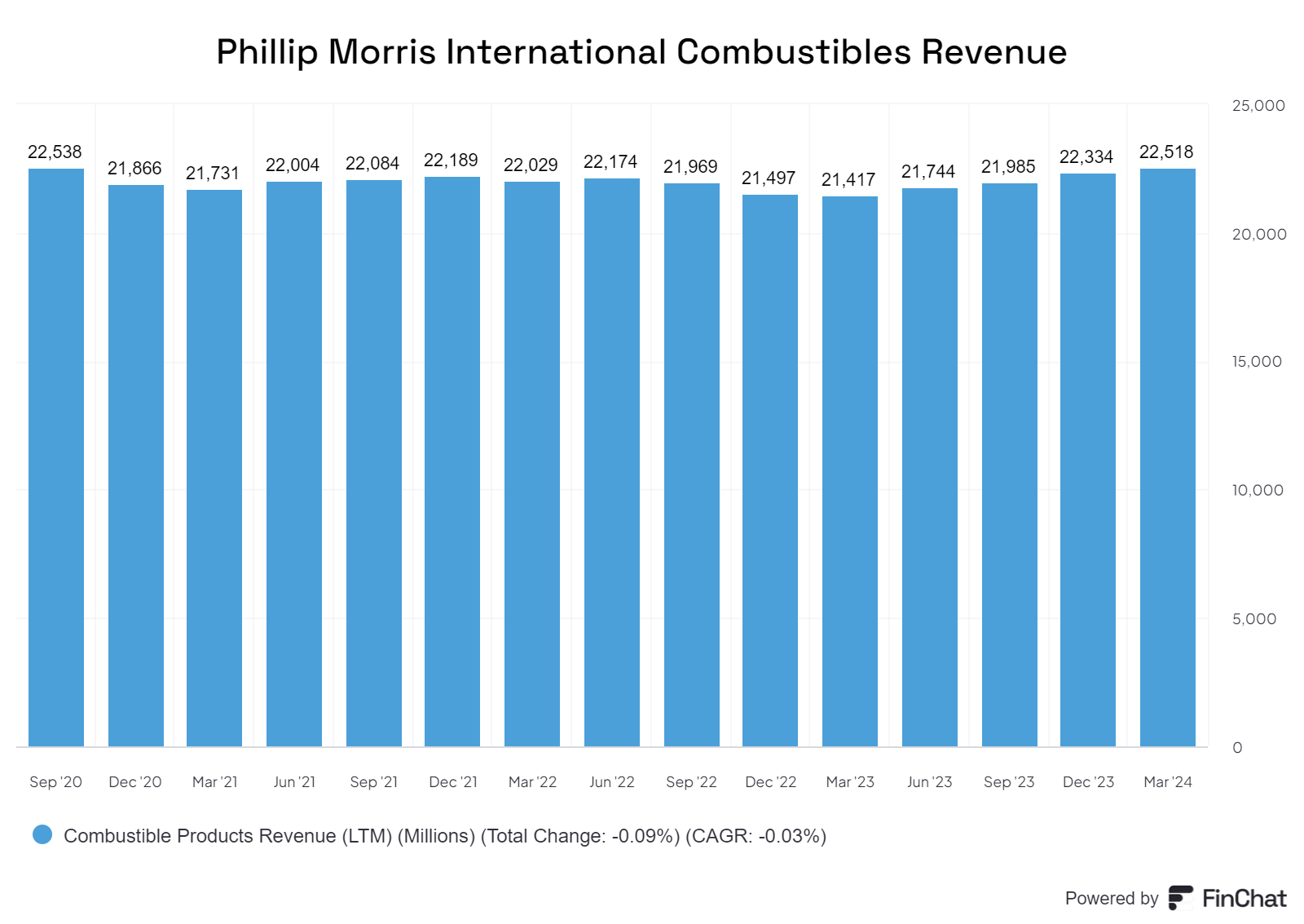

Phillip Morris’s combustibles revenue (i.e. cigarettes) has remained stable since September 2020:

Since this revenue stability is coming along with volume declines, earnings from combustibles have risen and should remain stable even if volume declines accelerate around the globe. I would bet on a lot of cash getting thrown off by the international combustibles business in the next 10 years.

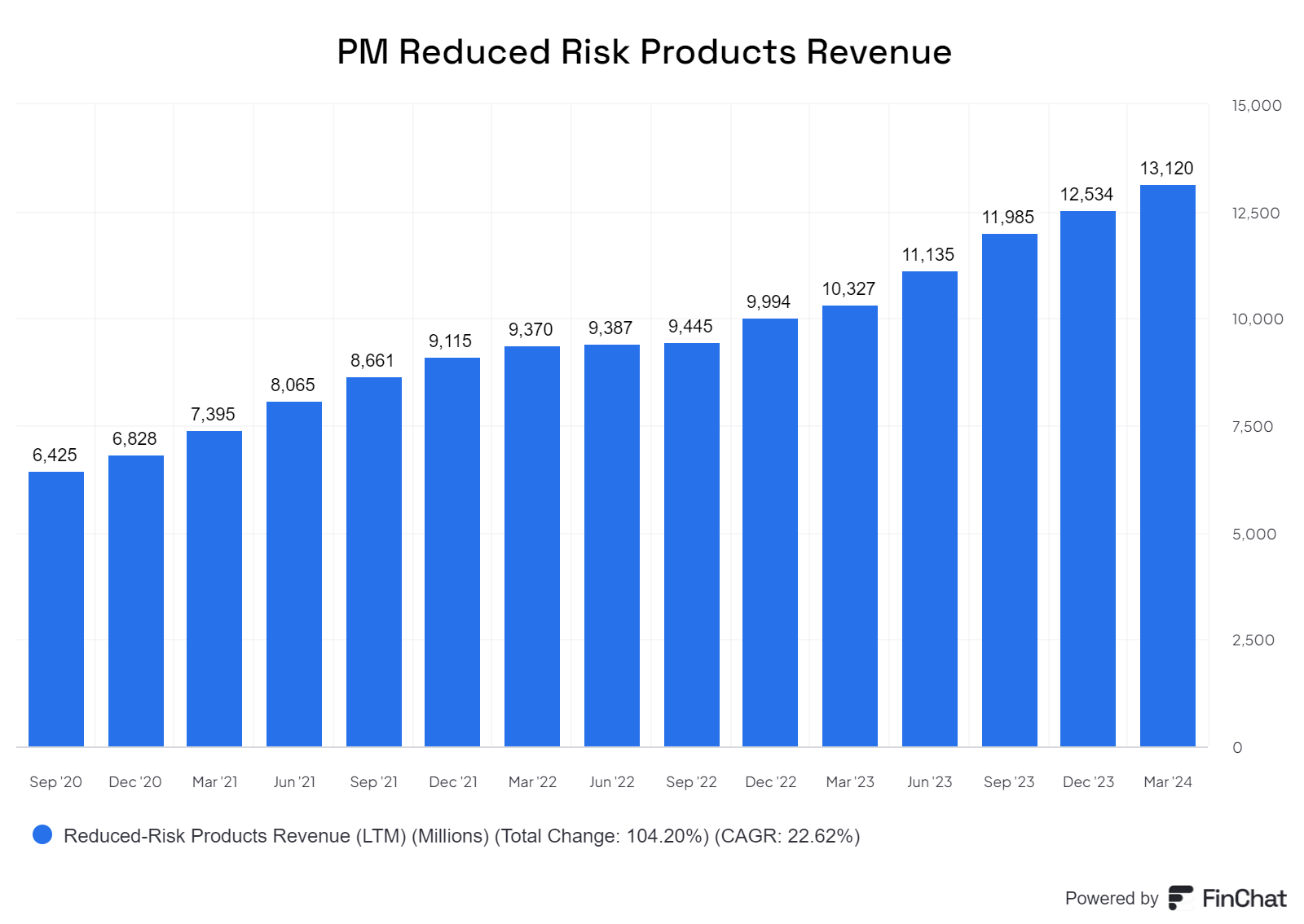

PM’s reduced-risk products continue to shine, with revenue growing at a 22% rate since September 2020:

At $13 billion in revenue, PM has established itself as the premier nicotine RRP business in the world. As it takes market share (from itself and others) in the coming years, it seems likely that this segment will hit $20 billion in revenue and eventually pass the combustibles segment in size.

The unit economics for RRPs should be similar to combustibles, if not better. Zyn nicotine pouches in the U.S. have better unit economics, but I am not sure how confident I am this holds up over the long term or across the other product categories.

Either way, what matters is that PM will have its combustibles business generate a lot of cash in the next decade — probably over $100 billion in total — while building another business in RRPs that is well on its way to generating $10 billion in annual earnings.

Today, you can buy PM for a market cap of $150 billion and a dividend yield of 5.5%.

I think it will prove very difficult for investors to lose money owning PM over the long term at these prices. Which is why it remains in the top 5 of stocks I want to buy once I get more cash into my account.

Hope everyone has a great week, and thank you for listening to Chit Chat Stocks!

- Brett