Not So Deep Dive: BigCommerce Stock (Ticker: BIGC)

A company trying to become the Shopify for enterprise merchants

Reminder: these are show notes that should be read in conjunction with the podcast. Do not expect these notes to be a polished research report.

As always, listen to the episode on Spotify, Apple Podcasts, or wherever you are subscribed to the show.

Charts

Show Notes

(Ryan) What they do: BigCommerce is a software-as-a-service website building and hosting platform. Similar to the other CMS businesses we’ve looked at this month, anyone can go to BigCommerce and set up a website and instantly begin selling online. However, BigCommerce has found the most adoption among enterprise customers (71% of ARR currently comes from enterprise accounts).

To lean into its enterprise focus, BigCommerce offers lots of solutions purpose-built to meet the needs of larger customers. Things like multi-language displays, extensive partner integrations, plug-ins to other sales channels (Amazon, eBay, and POS), multiple storefront functionality, and 24/7 technical support. This means BigCommerce often has longer sales cycles that include migrating over existing websites. Enterprise customers are classified as any business with more than $50 million in annual online sales. For reference, some BigCommerce customers include Skullcandy, SC Johnson, and Ben & Jerry’s.

In terms of revenue, BigCommerce charges has 4 pricing tiers. Standard ($29.95/month), Plus ($79.95/month), Pro ($299.95/month), and Enterprise (custom), and there are additional BigCommerce products that teams can sign up for, but they don’t charge anything on a per transaction basis.

(Ryan) History: BigCommerce was founded by Eddie Machaalani and Mitchell Harper who met in an online chatroom in 2003. Following the meeting, the two Australians ended up starting their own email marketing software business together called Interspire. While running Interspire, a part of the company was working on building easy e-commerce website software for non-technical business owners. This would eventually become BigCommerce. In 2009, this segment was spun out and relocated from Sydney, Australia to Austin, Texas.

Shortly after, BigCommerce raised $15 million in venture funding and began to invest heavily in its sales staff. By 2015, the business began shifting its focus towards enterprise customers and the two founders actually decided to name a new CEO, Brent Bellm. The company eventually raised 6 total private funding rounds and joined the public markets in 2020. Shares are down 63% versus the initial listing price.

(Brett) Industry/Landscape/Competition:

The SaaS e-commerce applications market is expected to reach $7.9 billion in 2025, up from $3.2 billion in 2020. That is 20% annual growth

Competitors in SaaS: Shopify, Wix, Squarespace

Competitors in enterprise: Magento, Oracle, SAP (a big list of legacy software companies)

(Brett) Management and Ownership:

Brent Bellm is the CEO, taking over the role in 2015. He has previous experience at HomeAway (VRBO) and Paypal. He worked at Mckinsey from 1993 - 2000.

They have a lot of VC investors on the board, and none of them take a salary, which is nice. Director compensation is negligible as a % of gross profit

They have 12 executive officers listed on their leadership page. For a company doing just a few hundred million in revenue, this feels like a lot. When looking at SG&A expenses as a % of gross profit, I think this concern checks out.

Total executive compensation was $18.3 million in 2021 or 10.7% of gross profit. And they wonder why SG&A expenses are not scaling.

Can you guess how compensation is structured? BigCommerce executives get a base salary, annual cash bonuses, and long-term equity awards. Thank you, compensation consultants!

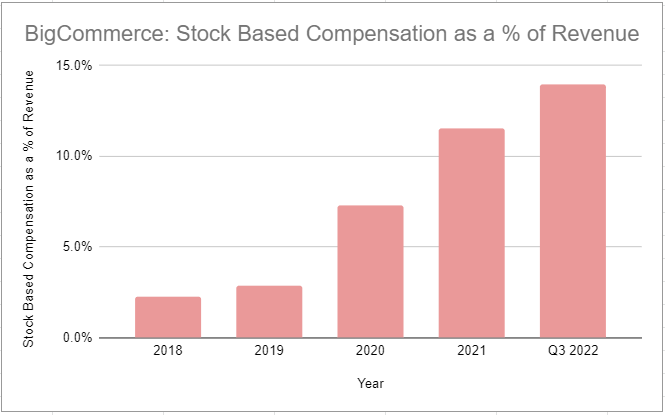

Annual cash bonuses are based on revenue, ARR, and adjusted EBITDA targets. This is a concern because it incentivizes stock-based compensation while pretending they have achieved profitability. The hurdles for these bonuses were also a joke. For example, the adjusted EBITDA margin hurdle was negative 13.7%.

The equity compensation has no performance metrics, but just got moved to 70% RSUs from a 50/50 option/RSU mix.

(Ryan) Earnings:

Last 12 months:

$271.5 million in revenue, +37% YoY

74.9% gross margins

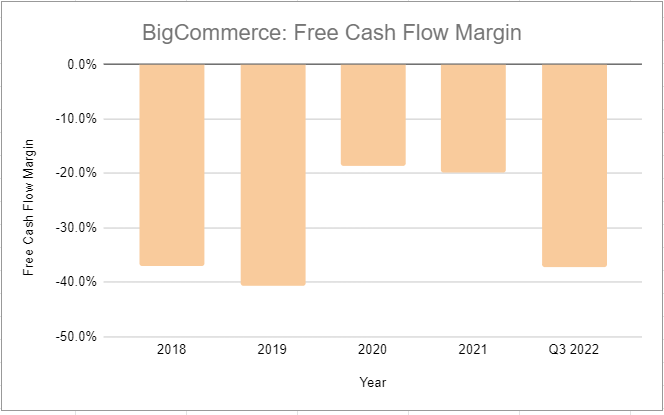

-$101 million in free cash flow (-37% FCF margin)

Most recent quarter:

Total ARR was $305.3 million, +20% YoY

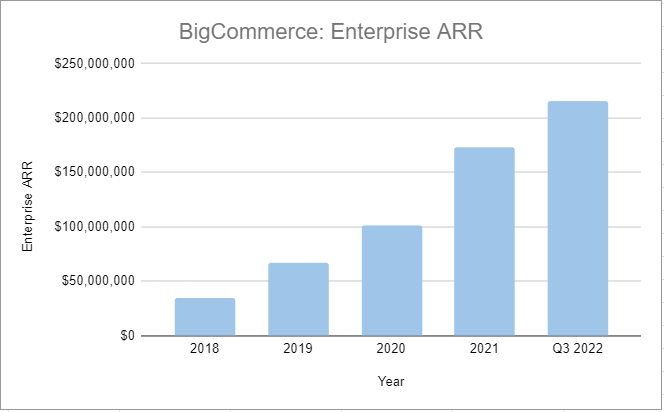

Enterprise ARR grew 35% YoY

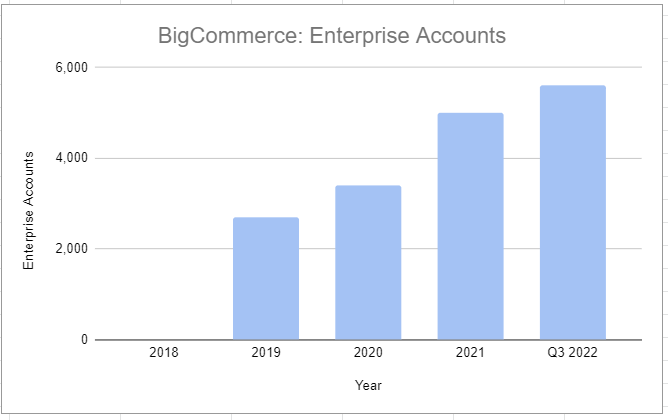

5,560 enterprise accounts, up 16% YoY

Average revenue per enterprise account was $38,885, up 17% YoY

Operating margin for the quarter was -42%

BigCommerce spends 156% of its gross profit on operating expenses. Sales & Marketing accounts for the most at 63% of gross profit.

(Ryan) Balance sheet and liquidity:

$307 million in cash & short-term marketable securities

$337 million in long-term debt

In 2021, BigCommerce issued $345 million worth of convertible senior notes due in 2026. These notes accrue interest at 0.25% and have an initial conversion price of $73.11 (a 722% premium to today’s price).

(Brett) Valuation:

Market cap of $600 million

Enterprise value of $640 million

EV/GP of 3.15

EV/FCF of -6.4

Anecdotal Evidence:

(Ryan) It seems like it has enough functionality to help an enterprise business run, but it has to spend lots of time and money trying to get those enterprises to switch. They just lack the level of notoriety that some of its competitors have.

(Brett) Reading a comprehensive product review, what customers say about the product seems to be in sync with what management pitches its capabilities as. I think this is a good thing, but this is no different than how all of its competitors talk.

Future growth opportunities:

(Ryan) Shifting away from smaller accounts. This is clearly the focus of management right now and they talked about it nonstop on the conference call. According to their Investor Day, the LTV to CAC on enterprise accounts is 8:1 vs. 2:1 for non-enterprise. This will hurt ARR growth in the short term, but they need to start generating cash here soon and this is the way to do that.

(Brett) I think the Feedonomics acquisition has some promise. This was a $145 million deal done in 2021. Feedonomics allows merchants to add inventory to 3rd-party marketplaces like Amazon, Google, eBay, etc. These marketplaces are only growing in size with merchants seemingly able to sell anywhere these days, so the value of Feedonomics for an enterprise merchant seems high. If I was an enterprise, maybe this is the type of tool that brings me over to BigCommerce compared to Shopify Plus.

Highlights and lowlights:

Ryan’s Highlights:

They seem to have carved out a solid solution for certain types of enterprise customers. Those customers are probably going to stick around for a long time and will probably grow as well.

Though it has been muted this year, they still benefit from the massive e-commerce tailwind. Legacy retailers are still in the process of migrating their offerings online.

Ryan’s Lowlights:

On the 3rd quarter conference call, management said “We remain committed to hitting breakeven on an adjusted EBITDA basis in the second half of 2024, and 2023 will therefore be an operating leverage year.” It feels like they’ll have to jump through lots of hoops just to get to breakeven Adj. EBITDA.

I don’t like their competitive position. The way I see it, the economics of a CMS business can be good if users come to you. You offer the platform and the user does the actual work of designing and setting up the shop and then pays you for hosting. But BigCommerce’s model just really doesn’t work like that and I think it shows in the financial statements.

Brett Highlights:

The transition to enterprise accounts. Enterprise ARR has grown at a CAGR of 63% since 2018 and now makes up the majority of BigCommerce’s revenue. Compared to SMBs, enterprises have much better net retention rates and can enable BigCommerce to invest for growth knowing that revenue will most likely be there to back it up. You can also see this with the average revenue per enterprise client growing year after year.

International expansion gives them an easy opportunity to grow with existing enterprise clients. Many enterprise clients are likely clamoring to start selling in as many countries as possible. They have a minimal presence outside of the United States right now but plan to go into all major geographies except Africa over the next few years. This might be expensive at first but should drive solid ROICs if the recent results in the United Kingdom are any indication.

Brett Lowlights:

The expense structure has gone off the rails. Management seems to finally be trying to fix this with a recent layoff, but when you spend over 100% of your gross profit on SG&A you will never achieve profitability.

I do not get a sense that management is focused on allocating dollars to focus on long-term growth in free cash flow per share. The proxy statement had many concerns already addressed on this show, including the negative adjusted EBITDA hurdle target. They also focus way too much on the competition, consultant reports, and stuff that truly isn’t relevant to running their business.

Bull Case:

(Ryan) Let’s just put some numbers on it. BigCommerce is currently on a $305 million annual revenue run rate. Management said in their investor deck that they think they can reach 10%-15% non-GAAP operating margins by 2026 and 20%+ long-term. If we assume they grow total customer count by 5%, average revenue per account by 5%, and convert 75% of that non-GAAP OI to free cash flow, BigCommerce would be generating a little over $40 million in free cash flow annually by 2026. At 20x, you’d have a market cap of $837 million vs. $700 million today.

(Brett) The current EV/GP is 3.15 and enterprise revenue is growing at a solid double-digit rate year-over-year. If the company gets any signs of operating leverage the stock will likely do well for shareholders over the next few years. There is a chance this is a 10-bagger over the next 10 years if this vision is executed. For reference, they believe BigCommerce can grow revenue at a 25% - 30% CAGR through 2026.

Bear Case:

(Ryan) Yep, easy bear case. They can’t hit their target margins or have to fire tons of people to get there which hurts their sales numbers (remember this is a sales-heavy business), and they can’t generate enough cash to pay back that debt.

(Brett) The bear case is super simple to me: profitability never shows up and stock-based compensation heavily dilutes shareholders. BigCommerce is going to need to either fire a lot of people or grow its revenue at a fast clip in order to start generating a profit (probably both). Can they do this with all the initiatives laid out during its investor day? I think there is clearly some uncertainty here.

More or less interested?

(Ryan) Less interested. I generally like the CMS space because there seem to be lots of latent operating leverage, but BigCommerce seems to lack that.

(Brett) Less interested. This is a business I want to like because of the theoretical unit economics, but there are too many hurdles they need to get over in the next few years to be confident in the stock right now.

Sources and Further Reading

BigCommerce review: https://www.stylefactoryproductions.com/blog/bigcommerce-review

2022 Investor Day Presentation: https://investors.bigcommerce.com/static-files/42734bd2-8826-41c6-8cf0-d623906ebbd2

2022 Proxy Statement: https://investors.bigcommerce.com/static-files/4b9140dc-1be0-4a92-8b56-107f23aa4fcb