Not So Deep Dive: Bill.com Stock (Ticker: BILL)

One of the fastest growing SaaS / fintech companies out there

Reminder: these are show notes that should be read in conjunction with the podcast. Do not expect these notes to be a polished research report.

YouTube

Spotify

Charts

Chit Chat Money is presented by:

Potentially you! Reach out to our email chitchatmoneypodcast@gmail.com if you are interested in sponsoring our newsletter, podcast, or both.

Show Notes

(Ryan) What they do: Put simply, Bill Holdings (primarily Bill.com) helps small to medium-sized businesses automate their cash inflows and outflows. And they do this through pretty much three segments:

Accounts Payable Automation: When you sign up for Bill.com, you receive a Bill.com email that your suppliers can then send invoices. All invoices will then begin showing up in your Bill.com dashboard. Or if you receive a physical bill, you can easily scan that bill with the Bill.com mobile app and it can detect the due date, designated dollar amount, and who the associated supplier is. Bill.com users can then approve the bill with a single tap and pay it via multiple methods. Subscribers can either automate ACH Transfers from their account, or they can choose to pay via a physical check and Bill.com will do that on their behalf. Bill.com can also facilitate international transfers if needed. Then, come reporting time, Bill.com integrates with pretty much all small business accounting systems so everything can get easily recorded.

Accounts Receivable Automation: On the flip side of AP Automation, Bill.com customers can easily create electronic invoices customized with their own logo. If required, Bill.com can also print and mail paper invoices to subscribers’ respective customers. When someone receives an invoice from a Bill.com user, they are directed to a link where they can easily put in their card info or ACH transfer data. Each invoice has a progress tracker as well so users can see where the invoice is (delivered, opened, authorized, collected). Once again, this segment easily synchronizes with whatever accounting system that the user needs it to.

Spend and Expense Management: This segment is comprised of their 2021 acquisition of Divvy. With Divvy, businesses can get spending cards for all their employees and track all expenses within the Divvy software system. The software program looks pretty sleek. You can set budgets for different departments, instantly see all payments made at your company, and quickly explain why you made a purchase (typically via the mobile app). Divvy also extends customers up to $15 million in credit through their issuing partner banks. This means they aren’t taking the credit risk on themselves.

(Ryan) History: René Lacerte founded Bill.com around 2005 after being ousted as CEO of the online payroll software startup he founded called PayCycle. The business had apparently been seeing stalled growth and there was some turmoil within the company between Lacerte and his COO, so the VC firm August Capital asked him to step down. Five years after stepping down, PayCycle was sold to Intuit for $170 million.

After being ousted, Lacerte instantly started working on his next project. In fact, it seems like he probably had this idea while working at his old company, but this gave him the excuse to get started. In the early days, Lacerte pitched Bill.com as a time saver for small business owners: “No more opening the mail, checking invoices, juggling when to pay which bill and then writing out, recording and reconciling checks by hand.” After acquiring the domain name for $200,000, they launched their first product in 2008. The initial business model had two forms of monetization, which still exist today, (1) monthly subscriptions + small transaction fees for businesses who subscribe and (2) a fee to nonsubscribers for receiving payments via Bill.com.

To grow fast, Bill.com began partnering with accountants and banks who would recommend Bill.com to the thousands of small businesses that they worked with. This partnership-based strategy helped Bill.com expand quickly, and after reaching a large enough size they were able to start investing some of the customer funds held on their platform into interest-yielding assets. Then in December of 2019, Bill.com came public raising a little over $200 million in the process. However, after pricing their shares at $22, the COVID bubble brought it all the way up to $335 within less than 2 years. That same year, Bill.com used its soaring stock to acquire Divvy for $2.5 billion and Invoice2Go for $625 million. They also held a follow-on offering of their stock that same year.

(Brett) Industry/Landscape/Competition:

The back office payments market is – as you might expect – quite large

Bill estimates there are 70 million SMBs and sole proprietors worldwide. They currently have around 450k people interacting with Bill products, or just 0.6% of this target market. However, not all small businesses are going to need an accounts payable and expense management solution (ex. Chit Chat Money) so this TAM is a bit overstated. Still, it is quite large and if Bill just gets a few % points of penetration the business will likely be much large five to ten years from now.

Competition is hard to cover comprehensively because there are so many point solutions and all these software companies have strange names that are hard to keep track of.

I think the best way to split up the competitive threats is into three categories. First, is Excel/paper solutions. This is the whitespace that Bill.com is going after where companies use older solutions instead of a dedicated back-office payments product.

Second, is the other point solutions that sell an AR, AP, or corporate spending product. This could include Brex (targetting start-ups), Tipalti (direct competitor with hundreds of millions in funding), and many more.

Third, is the frenemy in Intuit Quickbooks. Quickbooks is ubiquitous among SMBs, so there is a lot of customer overlap. Intuit is slowly creeping in on Bill.com’s turf with new products and has invested in a competitor called Melio. This is the biggest competitive threat I am concerned about and could end up being a real “moat test” for Bill.com if Quickbooks integrates its features natively

(Brett) Management and Ownership:

I am going to keep this one short since this is a very boilerplate Silicon Valley software ownership structure.

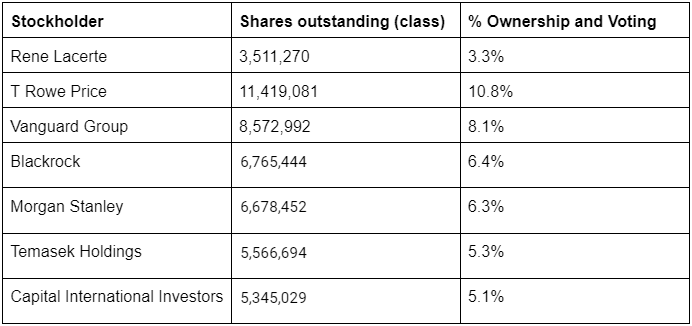

First, the company is founder-led by Rene Lacerte. He owns 3.3% of the company

The board has 13 members who all get paid over $200k a year. There are a bunch of venture capitalists on the board, and executives from Yext, Fastly, and Salesforce. Is this a significant red flag to you?

They do base salaries, cash bonuses, and equity incentives for their executives

Lacerte got $10 million in stock options (or something similar) last year

Cash bonuses based on revenue growth and non-GAAP earnings targets. Bad incentives?

Generally thought the executives were overpaid for a company of this size but I didn’t see any glaring red flags in the proxy filing

It looks like all the VCs except Temasek have gotten out

*Based on 105,632,997 shares outstanding as of latest proxy filing

(Ryan) Earnings:

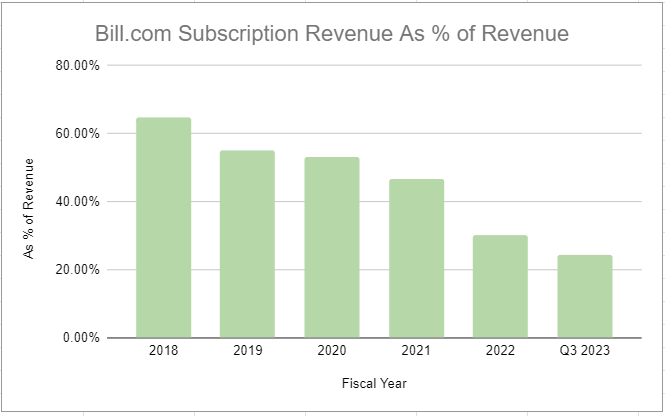

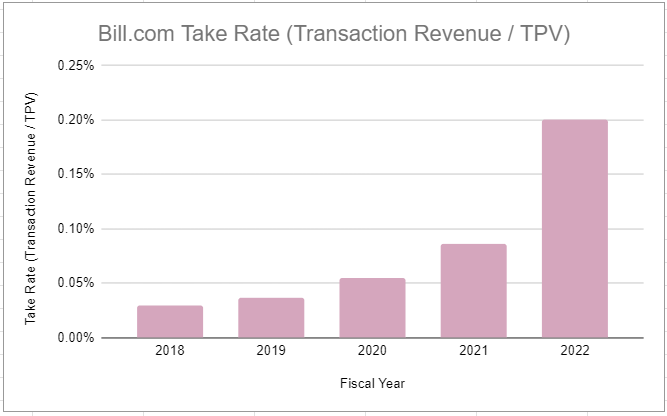

$963 million in revenue (63% is transaction fees, 24% is subscriptions, and 12% is float revenue)

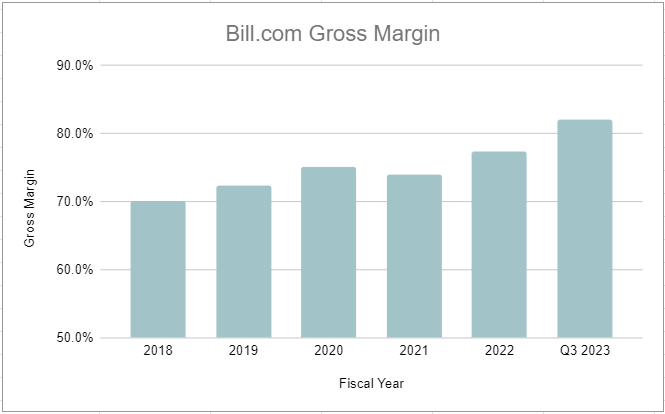

85% gross margins

($334) million in operating earnings, but keep in mind they earn a lot of interest income.

~$90 million in OCF (SBC and Amortization of intangibles are the big difference maker here).

Most recent quarter:

Grew total revenue by 63% YoY (45% excluding float revenue)

Reached 455k customers (customers are growing at 18% YoY)

Bought back $27 million worth of shares. Repurchasing stock?

(Ryan) Balance sheet and liquidity:

Assets:

$2.7 billion in cash and short-term investments

$3.1 billion in funds held for customers

Liabilities:

The real big one here is $1.7 billion in convertible notes

$1.15B due in 2025. Zero interest. $161 initial conversion price. (@ $114 currently)

$575M due in 2027. Also zero interest but has an initial conversion price of $415.

But they also have $135 million in a revolving credit facility

(Brett) Valuation:

Market cap of $11.8 billion

EV of $11 billion

EV/GP of 14.2

EV/OI of -32.6

EV/OI w/ 30% margin of 38.1

Anecdotal Evidence:

(Ryan) If our podcast gets bigger, I could see us using this at some point. Plus, watched a couple youtube videos on customer reviews and they really seemed to like the platform.

(Brett) It seems like a product that so many companies could use, but I think the “TAM” opportunity they talk about is inflated. There are a ton of businesses and sole proprietorships that would not get value from using Bill.com.

Future growth opportunities:

(Ryan) Divvy. I already spoke about the functionality here but I think it looks like a pretty sweet solution. They paid $2.5 billion to acquire them in mostly stock, so they definitely need to prove that it’s worth it and so far so good I think. Divvy actually generates the majority of Bill.com’s transaction revenue and this quarter that was growing 65% YoY. They have 27k business customers using the platform, which is up 50% from last year.

(Brett) Float interest income. I think investors may be underrating how much in interest income Bill.com can start to earn over the next few years if it continues scaling up its operations and interest rates stay around 5%. This could lead to hundreds of millions of dollars in extremely high-margin “revenue” for the business. However, over time this feels like a strength that could be an area of weakness as some competitors have discussed offering the ability to pay merchants part of the interest they earn, similar to a bank.

Highlights and lowlights:

Ryan’s Highlights:

Seems like a great solution for SMBs and they seem to be demonstrating that with their growth rates.

Slightly inflation protected through their transaction fees and the float revenue benefits from higher interest rates.

According to an asset management firm called Kayne Anderson Rudnick: “Eighty percent to ninety percent of businesses still rely on paper checks as a primary form of payment,”. The automated checks component is still a big sell for customers.

Ryan’s Lowlights:

Still seem to have a growth-at-any-cost mentality. They are not profitable (not even close frankly) and they were buying back shares this quarter at 12x sales.

Quickbooks adding native Bill Pay. Last December, Quickbooks announced that it was rolling out its own native bill-paying software for its business customers. Quickbooks has 6 million paying customers, and I imagine there is a substantial overlap between Bill.com’s customers and Quickbooks’. Might not hurt existing customers but it could be harder to attract new ones.

Float revenue could be at risk if the time to clear payment transactions ever shrinks.

Brett Highlights:

Great unit economics that should lead to 30%+ profit margins (according to management) over time. It probably should be even higher too given the float dynamics, but I guess they don’t want to overpromise anything.

The growth track record has been fantastic and it looks like there is still a ton of whitespace for them to go after this decade.

Brett Lowlights:

They do not understand capital allocation. They are buying back shares to “offset dilution.” This is dumb. Not surprising given the makeup of the board of directors.

The competition potential from Quickbooks. A ton of Bill.com customers also use Quickbooks. Could Intuit counterposition itself and undercut Bill.com with a bundled offering? Maybe.

No cost efficiency on S&M expense line. What happens when revenue growth moderates?

Bull Case:

(Ryan) A lot needs to go right for this to work out. You really have to believe in the growth story here. I think you probably have to assume 20% Net Income margins at some point, plus continued 20%-30% revenue growth.

(Brett) If double-digit revenue growth continues and they hit a 30% operating margin the stock will likely work from here. If it doesn’t, then it will probably be a good buying opportunity three to five years from now.

Bear Case:

(Ryan) Competition eats away at new customer growth and multiple compression.

(Brett) My two big concerns are bad management of the income statement and competition from Quickbooks.

More or less interested?

(Ryan) More interested. Reminds me a bit of Remitly. Great brand, great product, but investing a little too much for growth right now. At 4x-5x sales I’d be more interested.

(Brett) More interested. This looks like a good business that could widen its moat and turn into a great business over the next 10 years. At the right price (significantly lower than today) it would look pretty darn compelling.

Stock for next week? (Visa)

Sources and Further Reading

Review from PCMag: https://www.pcmag.com/reviews/billcom

What does Divvy do?: