Not So Deep Dive: Meta Platforms (Ticker: META)

The social media darling is at a crossroads. Or is it?

Reminder: these are show notes that should be read in conjunction with the podcast. Do not expect these notes to be a polished research report.

Schedule for upcoming weeks: Salesforce, Alphabet

As always, listen to the episode on Spotify, YouTube, or wherever you are subscribed to the show.

Charts

Data powered by Stratosphere.io

Chit Chat Money is presented by:

Stratosphere.io, a powerful web-based research terminal for fundamental investors.

Stratosphere.io has made it easy for us to get the financial data we need with beautiful out-of-the-box graphs that help us do research for Chit Chat Money.

🎉Stratosphere.io just launched their brand new platform and you can give it a try completely for free.

It gives us the ability to:

Quickly navigate through the company’s financials on their beautiful interface

Go back up to 35 years on 40,000 stocks globally

Compare and contrast different businesses and their KPIs

Easily track insider transactions and news updates for any stock we follow

Get started researching on the Stratosphere.io platform today, for free, or use code “CCM” for 15% off any paid plan.

Show Notes

(Ryan) What they do: Most people know the business already so I don’t think it’s worth going too long on this side. Meta splits its business up into two parts:

Family of Apps (FOA): This consists of Facebook, Instagram, WhatsApp, and Messenger. As of the latest quarter, Meta estimates that 3.7 billion unique people use at least one of these four properties every month. To generate revenue, Facebook offers businesses a really comprehensive advertising platform. Advertisers can run very customizable campaigns across Facebook, Instagram, or Messenger, or they can let Facebook themselves find the optimal placement. WhatsApp, on the other hand, monetizes in a number of ways right now including click-to-message ads (sends people that click on your ads directly into one of their messaging places), payments, and even shopping. In the last 12 months, FOA generated $115 billion in revenue with a 42% operating margin.

Reality Labs: This includes primarily the Meta Quest ecosystem and Facebook Portal products. If you go to the Meta Quest store right now, you can buy one of three pieces of hardware. The Meta Quest 2 ($399), the Meta Quest Pro ($1,499), and accessories for both. But beyond hardware, Meta also develops its own games/apps for its ecosystem, with its most notable being Horizon Worlds (poor man’s Roblox). In addition, from reading through various online chat rooms it looks like Meta has a 30% take rate for 3rd parties that sell within the Quest ecosystem. I imagine there are also some ways to have promoted games, but I couldn’t find that broken out anywhere. In the last 12 months, FRL generated $2.3 billion in revenue and reported $13 billion in operating losses.

(Ryan) History: Similar to last week, people are probably already familiar with the Facebook founding story so I’ll try to condense the history to the last couple of years. Let’s start with 2020. From what I could find, that was the year that Apple announced its new operating system would prohibit advertisers from tracking users unless the user explicitly allowed it. Shortly after that, in Q4 of 2020, Facebook had this now iconic conference call where you could almost timestamp the shift in focus from the company. “We increasingly see Apple as one of our biggest competitors…Apple has every incentive to use their dominant platform position to interfere with how our apps and other apps work, which they regularly do to preference their own.” For reference, in Q1 of 2020 the term VR was only mentioned once and the word “metaverse” wasn’t mentioned at all. They’d been investing in the space really ever since they acquired Oculus in 2014 for $2B, but hadn’t really ramped up the spending until 2020.

One year later, in February of 2022, the company announced that it would begin reporting its revenue into the two categories I mentioned above – FOA and FRL. Three months after that, the company formally changed its name from Facebook to Meta Platforms. Since that conference call, Meta or Facebook’s stock has declined by 46%.

(Brett) Industry/Landscape/Competition:

Meta operates in two industries: digital advertising and virtual reality (you might call it the metaverse if you are Marck Zuckerberg). There are also some messaging features within WhatsApp and Messenger, but for now, those are small parts of the company

The digital advertising industry is large but still growing steadily. Global spending is estimated to have hit $600 billion in 2022 and could get over $1 trillion by the end of this decade

The virtual reality market is a lot smaller, at $21 billion. Third-party analysts predict it will keep growing in the double digits for the foreseeable future. Is this market too small for Meta to go after? Or can they build it themselves?

Competitors in advertising listed on the annual report: Alphabet, Amazon, Apple, Bytedance, Microsoft, Snap, WeChat, Twitter

Competitors for virtual reality: Sony, Microsoft/Xbox, and Apple (working on something apparently).

(Brett) Management and Ownership:

As we all know, the CEO of Meta Platforms is Mark Zuckerberg. Zuckerberg owns almost all the Class B shares of Meta’s stock, giving him greater than 50% voting power.

Curiously, Zuck has been a consistent seller of his shares, with his voting power decreasing from 67.2% in 2013 to 56.9% today. Could we see this trend continue over the next decade?

Last thing on ownership: the alleged co-founder of Facebook Eduardo Saverin still owns 2.0% of the stock and some Class B shares that give him 7.3% voting power. He could have some sort of impact with this voting power but it does not matter until Zuckerberg’s voting power gets below 50% (if it ever does).

In 2022, Meta went through multiple executive shakeups with the longtime COO Sheryl Sandberg and CFO Dave Wehner leaving their positions. It looks like Zuckerberg decided to hire internally to replace these roles

The board of directors is made up of some other tech founders (Dropbox, DoorDash), some other executives, Mark and Sheryl, and Marc Andreessen. They used to have Peter Thiel and Reed Hastings on the board.

Disucssion question: Are you worried that Zuckerberg has surrounded himself with “Yes-men” recently?

Executive compensation follows the standard three-tiered approach: Base pay, annual cash bonuses, and equity awards that vest over four years. The base salaries for executives are all under $1 million a year and pretty reasonable.

The cash bonuses are based on unquantifiable metrics. Take a look at this table and see if you can parse out what they mean:

A quote that concerns me given the recent executive turnover:

“We use equity compensation to align our executive officers' financial interests with those of our shareholders, to attract industry leaders of the highest caliber, and to retain them for the long term”

The equity pay is RSUs that vest over four years. No performance metrics are attached

Zuckerberg famously has a $1 dollar salary, however, he gets $26 million worth of security measures and private aviation paid for by the company each year, so this is a bit of gaslighting.

No giant red flags outside of the obvious dictatorial ownership structure, but I did not like the Meta Proxy statement vs. the other big tech companies we have covered.

(Sources: Proxy Statement and Whale Wisdom. 2,651,548,674 shares outstanding at the end of Q3 2022)

(Ryan) Earnings:

Last 12 Months:

$118 billion in revenue, +5% vs. 12 months prior.

97% of that is from the family of apps

The remaining 3% is from FRL

$35 billion in total operating income, -25% vs. 12 months prior.

$54 billion in operating cash flow

$26 billion in free cash flow (spent $28 billion on capex in the last 12 months, +56%)

Most recent quarter:

Total revenue declined by 4%. Would’ve been +2% on a CC basis.

Active users are still growing gradually, but the average price per ad is coming down.

That’s due to both some macro difficulty as companies have pulled back on their ad budgets, but also a large shift towards Reels which doesn’t monetize at the same level yet.

Operating margin was 20% vs. 36% a year ago.

Next year, management expects:

Total costs and expenses to be $94-$100B, +13% YoY

Capital expenditures to be $34-$37B, +14% YoY

The only real guidance they’ve given is that they want to grow operating income in the long term.

(Ryan) Balance sheet and liquidity:

Pretty straightforward balance sheet compared to the other tech companies we’ve looked at recently.

Cash:

$42 billion in cash and short-term marketable securities. This is all just pretty much US and corporate debt securities. Most of the debt securities they own mature in the next 12 months.

$6.5 billion in longer-term equity investments. Not really sure what’s in this honestly, aside from a quarter of a billion investment in Giphy.

Debt:

$10 billion in long-term debt, which they raised in August of 2022. This is the first time they’ve ever raised debt as far as I can tell.

It consists of a mix of 2027, 2032, 2052, and 2062 notes, and has an effective interest rate of just under 4%.

(Brett) Valuation:

Market cap of $380 billion

Enterprise value of $341 billion

EV/GP of 3.6

EV/OI of 9.7

EV/FCF of 13.0

Anecdotal Evidence:

(Ryan) I no longer use Facebook or Instagram, although I used to. And I never really use WhatsApp unless I’m traveling internationally, but even now with iMessage, it’s pretty rare. I’ve never once tried a VR headset. My friends still use Instagram a ton though. And from what I’ve seen, Reels really is taking off in adoption.

(Brett) I do not use Facebook or Instagram (humblebrag) but did have some experience with WhatsApp in Mexico. The app is very prevalent in Latin America and Asia and has a more social feel to it. They actually had stories on it in Mexico that were fairly popular with locals to use. I wonder whether they can have the same success in Africa with WhatsApp or not?

Future growth opportunities:

(Ryan) Reels. This is their short-form video competitor to TikTok which exists on both Facebook and Instagram. In Q2, management mentioned that Instagram Reels was on a $1B revenue run rate, and a quarter later they said Facebook and Instagram Reels combined were at a $3B revenue run rate. In terms of demand, here’s what management had to say: “There are now more than 140 billion Reels plays across Facebook and Instagram each day. That's a 50% increase from six months ago. Reels are incremental to the time spent on our apps. The trends look good here, and we believe that we're gaining time spent share on competitors like TikTok.”

(Brett) WhatsApp monetization. There are multiple products that seem to be working together to drive strong revenue growth on top of the core messaging/social platform: click-to-message ads, payments, and shopping. These features have been launched in markets like Brazil and India. My only gripe is that they are not investing faster to launch these products in as many markets around the world. With 2 billion DAUs and North America as its fastest-growing market, there could be tens of billions of revenue potential for WhatsApp to go after this decade.

Highlights and lowlights:

Ryan’s Highlights:

I think the core family of apps isn’t going anywhere for a long time. Their ability to integrate the next big thing into their existing user experience has been really impressive with Stories and now with Reels.

The potential of WhatsApp. I know people have been saying this for years, but WhatsApp has the scale and the staying power to give Meta lots of shots on goal when it comes to monetization. And I think we’re seeing that inflection now with Click-to-WhatsApp advertising ($1.5B run rate growing 80% YoY)

Ryan’s Lowlights:

FRL, plain and simple. I watched their 3-hour Meta Connect presentation and I can confidently say now that’s 3 hours of my life I’ll never get back. It seems like they’re exerting an absurd amount of mental effort and financial resources to build out the tech behind their metaverse ambitions without truly considering whether or not people want it. I’m yet to see this take any real effect, and if the rebuttal is that this is early days, then I’d be even more concerned as a shareholder.

I find myself constantly questioning what Zuckerberg’s motivation is. Does he want to drive value for shareholders? Is he on a revenge quest against Apple? Would he be willing to admit that FRL isn’t worth the investment at any point?

Dave Wehner (CFO) leaving the company. For the CFO to leave at this point in time really concerns me.

Brett Highlights:

I struggle to find highlights for Meta which is strange because of how damn profitable the core business is. But my biggest highlight has to be the current durability of Instagram (knock on wood) with the onslaught of apps trying to steal attention like Snap, TikTok, Discord, etc. Yes, TikTok has grown rapidly, but usage on Instagram is still at record highs. With its users skewing to the demographic sweet spot for advertisers (20 - 60-year-old females) that is some of the most valuable real estate on the internet.

WhatsApp potential this decade. It wouldn’t be surprising to see the app hitting 3 billion+ DAUs within five years or so, giving Meta a tremendous opportunity to drive revenue growth. Again, I wish they would focus more on WhatsApp.

Brett Lowlights:

The Zuckerberg dictatorship. Having the Class B shares is a big negative here, as he seems to be lost in his own world about the metaverse. Here’s a quote from a CC: “But I think our work here is going to be of historic importance.” Yikes

The Reality Labs losses. An obvious one where the base case is they burn $100 billion in capital this decade.

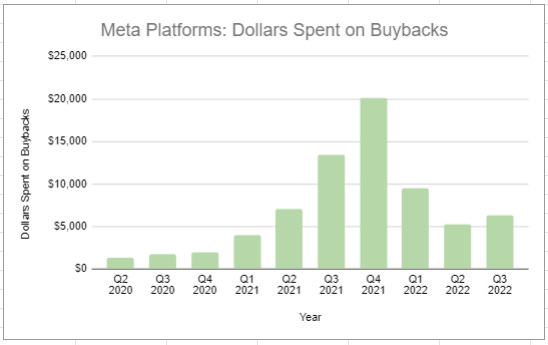

Poor balance sheet management. They started repurchasing a ton of shares during the 2021 bubble which indicates to me they may not have the right mindset when evaluating how to create value over the long term for shareholders

There has been little-to-no growth from the non-advertising part of this business for the last decade with a ton of failed initiatives like crypto, payments, Shops (maybe TBD on that one), etc.

A lot of the content they are monetizing has political, cultural, and ethical red flags for a lot of people. This is a potential downside that is not quantitative but shows that a lot of the time they are not playing a “non-zero-sum game” with all stakeholders, which makes the business a bit more fragile compared to some of the other technology giants.

Bull Case:

(Ryan) The bull case is that they generate the same amount of cash or more in 3-5 years. If that happens, at the current EV/FCF of ~13x, I think you’d get an adequate return.

(Brett) At an EV/OI under 10, all you need to get adequate returns going forward is durable earnings and an executive team that does not mishandle the earnings given to them. If you think this is likely, the stock is an easy buy at today’s prices.

Bear Case:

(Ryan) The range of outcomes seems very wide here. And the downside, over a 3+ year time horizon, I think is entirely dependent on the operating losses within FRL. If they refuse to reign in spending despite little demand, this will be an underperforming investment. The good thing is though, I think the lower the stock goes, the more pressure Zuckerberg has on him to rationalize costs.

(Brett) The anger-inducing level of poor capital allocation continues. Plain and simple.

More or less interested?

(Ryan)

(Brett) Less interested. I have worries about management and durability.

Stock for next week? (Salesforce)

Sources and Further Reading

Sandberg misuse of funds: https://www.bizjournals.com/bizwomen/news/latest-news/2022/06/sheryl-sandberg-meta-workers-foundation-wedding.html?page=all

Horizon Worlds Users: https://www.forbes.com/sites/paultassi/2022/10/17/metas-horizon-worlds-has-somehow-lost-100000-players-in-eight-months/?sh=3a8e05872a1b

WhatsApp Pay and new product developments: https://www.messengerpeople.com/whatsapp-pay-mobile-payment-news-statistics-and-developments/#:~:text=WhatsApp%20sends%20instructions%20to%20banks,India%20and%20Jio%20Payments%20Bank.

The Zuckerberg Flop: