Not So Deep Dive: NVR Corporation (Ticker: NVR)

The only profitable homebuilder that generated positive cash flow every year of the Great Financial Crisis

Research folder with show notes, charts, and valuation: https://drive.google.com/drive/u/0/folders/1QAnSiRwXBJPt-k1uH_fLWPfrfkSMbhmz

Reminder: these are show notes that should be read in conjunction with the podcast. Do not expect these notes to be a polished research report.

As always, listen to the episode on Spotify, Apple Podcasts, or wherever you are subscribed to the show.

Show Notes and Charts

(Ryan) What they do: NVR is one of the largest homebuilders in the United States by revenue. They focus on primarily building single-family homes, townhomes, and condos in several east coast markets under the brands Ryan Homes, NVHomes, and Heartland Homes. NVR breaks its markets up into 4 segments: Mid Atlantic (MD, VA, WV, DE, and DC), North East (NJ & East. PA), Mid East (NY, OH, West. PA, IN, and IL), and South East (NC, SC, FL, and TN). The bulk of NVR’s homes are marketed and sold to first-time and first-time move-up buyers, so these are generally on the more affordable side. In fact, the average price of NVR’s new orders in 2021 was $436,000.

However, unlike most homebuilders, NVR typically doesn’t engage in the actual land development process. Instead, NVR enters into lot purchase agreements with 3rd party land developers to acquire the finished lot once NVR has sold it. In exchange, NVR will pay the land developer a deposit of up to 10% of the estimated purchase price of the finished lot.

While the lot is being developed, NVR markets and sells these soon-to-be-built homes to buyers at a separate furnished model. Once the purchaser agrees to buy the home, NVR can then pay for the finished lot in full and hire subcontractors to construct the actual home design. In that process, NVR also provides mortgage financing for their buyers. Although, since NVR prefers to operate with little debt, after they originate the mortgage loan they then sell it into the secondary market.

(Ryan) History: Limited history of the company, but NVR was first founded in 1980 as NVHomes by Dwight Schar. Six years after its founding, NVR issued some high-yield debt and drew down bank credit lines to acquire Ryan Homes, who Shcar had actually previously worked for. However, in the early 90s, real estate entered a bit of a slump and at the time NVR reportedly had a bunch of land on its balance sheet that quickly declined in value, forcing NVR to file for bankruptcy in 1992.

After reorganizing and emerging from bankruptcy, NVR went public in 1993 and began implementing its new option-based purchasing model. NVR continued to expand this model into some new markets and during the financial crisis in 2008, it served them quite well. NVR was one of the only homebuilders that remained profitable every year throughout the financial crisis. Shortly after, in 2012, NVR acquired Heartland Homes and in 2019 they were added to the S&P 500. Since listing in 1993, NVR’s stock is up ~40,000%.

(Brett) Industry/Landscape/Competition:

The market size of the U.S. homebuilders is estimated to be $129.3 billion, making NVR 7.66% of the market

IBIS World expects the industry to decline by 4.6% in 2022. It has grown by 4.4% a year since 2017

There are a ton of macroeconomic factors that affect the homebuilding market (interest rates, demographics, current housing supply), making it a cyclical industry that is hard to forecast. Rising interest rates have affected mortgage rates and therefore affordability. Here is a good update from Redfin (chart below): https://www.redfin.com/news/housing-market-update-mortgage-payments-hit-new-high/

There is also a housing shortage in the U.S. right now. Unfortunately, the areas with the highest shortages are not where NVR operates (outside the Washington D.C. area): https://www.nar.realtor/research-and-statistics/housing-statistics/housing-shortage-tracker

Competitors: Tons. The largest are D.R. Horton (25% market share) and Lennar (24% market share). Here’s a list: https://csimarket.com/stocks/competitionSEG2.php?code=NVR

(Brett) Management and Ownership:

The CEO is Paul Saville who has been at the helm since 2005. He is a lifer at the company and has been there since 1981. He is 66 years old.

A good chunk of the management team has been there for a long time. The CFO has been with the company since 1994.

They explicitly talk about NVR’s unique compensation structure and how it is a “competitive advantage.” However, it looks pretty similar to other companies to me.

Annual incentive bonuses are based on pre-tax profit and net new order hurdles. Both are good metrics.

Performance-based stock options are given out based on return on capital number vs. homebuilding peers. They have consistently been the highest among homebuilders over the last decade.

Executives are required to own a healthy chunk of stock (as % of base salary), and as you can see from the chart below there is a lot of insider ownership. The flip side is that this has been done through heavy SBC programs.

With Vanguard and Blackrock both large shareholders, it looks like there is a lot of room to continue the buyback program without running into issues finding sellers. For reference, the average 10-day volume has been approximately $77 million worth of shares traded daily (source: Koyfin). I don’t think NVR will have issues continuing its buyback program.

(As of latest Proxy statement)

(Ryan) Earnings:

Last FY:

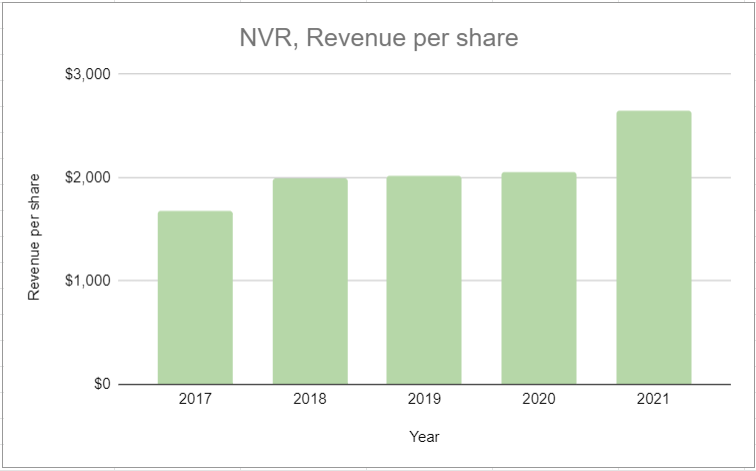

$8.7 billion in revenue, up 19%

22% gross margins

21.5k home settlements (+9%) and 12.7k home orders in the backlog (+10%)

$1.2 billion in operating cash flow, up 34%. Little to no capital expenditures, so free cash flow was about the same.

Most Recent Quarter:

New orders decreased by 16% YoY

New order cancellation rate jumped from 8.3% to 14.3%

The average new order price actually increased by 7%

Generated ~$450 million in free cash flow during the first 6 months

(Ryan) Balance sheet and liquidity:

Assets/Cash Flow:

$1.5 billion in cash and cash equivalents

Generated $450 million in free cash flow over the first 6 months of this year

Liabilities:

$916 million in senior notes. All due in 2030 with a 3% interest rate.

They also have a $300 million available revolving credit agreement that they aren’t using.

And NVR has a $150 million revolving mortgage repurchase agreement, which allows the NVR mortgage subsidiary to borrow if it needed to finance the loans themselves.

(Brett) Valuation:

https://docs.google.com/spreadsheets/d/1PtOrjSuaD79aRlKlInypgvnoP83q5m9TxAao1lDUzpU/edit#gid=0

Market cap of $13.6 billion

Enterprise value of $13 billion

EV/OI of 6.4

EV/FCF of 11.4

Anecdotal Evidence:

(Ryan) I’m going to lay out some information so people can come to their own conclusions on the real estate market today:

Today, the median income earner in the US would have to spend ~50% of their income on mortgage payments to buy an average-priced home.

Today, American homeowners have an all-time record of home equity.

Unlike in 2008 the vast majority of US household debt today is fixed-rate, not variable.

Today, the number of homes listed for sale is near a record low.

And depending on the source, there seems to be significant shortage of available housing relative to demand.

(Brett) We have all seen the data around the real estate market recently. Affordability is off the charts and I am pessimistic about where home prices are going. However, I could be wrong. For NVR specifically, I think it is positive they do mostly build-to-own (BTO) and land options, which should help them from becoming “bagholders” of inventory that needs to be written down. Still, uncertain times for the company and not surprised stock is down.

Future growth opportunities:

(Ryan) The blueprint for growth is pretty simple, so I’ll try to put a little creativity into this. If home prices begin to quickly decline over the next couple of years and homebuilders become reluctant to buy new land, it seems like a great time for NVR to be aggressive in signing new LPAs or in acquiring homebuilders in new markets.

(Brett) For a home builder, it is tough to identify much of a future growth opportunity besides “build more houses and then sell them.” NVR also states it does not like to expand outside of its core markets (the south, Florida, east coast, and eastern Midwest). However, I think over the long-term if they want to improve annual unit volumes there will need to be geographic expansion. Maybe management makes a small acquisition and implements its unique strategy in another market like the Rockies?

Highlights and lowlights:

Ryan’s Highlights:

Proof of success with a much more capital-light model than other home builders.

Over the last ~27 years, NVR has reduced its share count by 82% and they’re accelerating that buyback pace right now. They’ve bought back more than $1 billion in the first half of this year alone. That’s ~8% of the market cap today.

If market conditions deteriorate quickly, NVR’s option-based model gives them more flexibility than competitors to avoid losing money on developments.

Insiders have been buying lately.

Ryan’s Lowlights:

The decrease in new orders. The outlook for home buying looks grim right now. Hard to imagine them actually growing cash flow over the next couple of years.

Brett’s Highlights:

Track record of steady volume growth combined with steady share repurchases. Yes, there is a headwind from heavy stock-based compensation, and the share count hasn’t come down as aggressively in the last five years as the previous 25, but this is a management team that clearly treats shareholders the right way.

Reading what information we have on the business, I get the feeling they are frugal and disciplined (in a good way) and don’t mind being out of the limelight. When combined with a strong capital returns strategy, this is where 100 baggers come from.

The asset-light strategy. It makes sense and is clearly a winning strategy vs. other homebuilders given the numbers NVR puts up.

Brett Lowlights:

I have one lowlight, and it is simply the macroeconomic factors outside of management’s control. No matter how well-run NVR is, it is still a homebuilder that struggles to convert earnings into cash and is at the whims of central banks and housing prices.

Bull Case:

(Ryan) 5 years from now, if NVR sells 25,000 homes at an average price of $400,000, they’ll be generating $10 billion in revenue. Assuming their SG&A expenses/settlement continue to decline, and gross margin goes back to about 20%, they should be earning let’s say $1.5 billion a year (would probably be less but just for round numbers). Assuming they repurchase $2 billion worth of stock at the current price cumulatively over the next 5 years, they’d be sitting at a ~$11 billion market cap. A low teens multiple on those earnings would give you almost a double over the next 5 years.

(Brett) At the current share price, I think you just need to hope the housing market doesn’t take a steep tumble. Given management’s discipline, the healthy repurchases, and starting valuation, I think investors will do fine over 10 years as long as free cash flow generation is stable.

Bear Case:

(Ryan) One of two things has to happen. Prices will decline or volumes will decline. Or more likely a combination of both. If that happens, this might not go anywhere for a couple of years. But I have a hard time seeing investors lose money on this over a decade.

(Brett) There is a combination of margins that revert back to the near-term average of 12% (or lower) and housing prices that collapse even further than they are right now. Unless NVR is able to get volumes up significantly, this would bring down earnings and cash flow generation. Even though the stock looks cheap right now on a trailing basis, it would end up looking expensive from these prices three or four years from now.

More or less interested?

(Ryan) More interested. It seems like a perfect example of the innovator’s dilemma, and if the industry hits hard times over the next couple of years, NVR’s advantages will show up even more.

(Brett) More interested. I worry about the price you are paying today based on what forward earnings could look like, but it is something I am keeping on the watchlist. A well-run business that focuses on creating value for shareholders.

Stock for next week? (Zillow)

Sources and Further Reading

Ensemble Capital Q2 Letter: https://intrinsicinvesting.com/2022/07/20/ensemble-capital-investor-letter-second-quarter-2022/?dataOffset=2680.5

2020 NVR ValueInvestorsClub Writeup: https://www.valueinvestorsclub.com/idea/NVR_INC/3399159131

Cullen Roche views on home affordability: https://www.pragcap.com/three-things-i-think-i-think-its-breaking/

NVR 2021 Annual Report, and historical log: https://nvri.gcs-web.com/financial-information/annual-reports

2022 Proxy Statement: https://nvri.gcs-web.com/static-files/5ed6637f-670a-4206-8ffa-d5021f58f4db