Not So Deep Dive: Squarespace Stock (Ticker: SQSP)

Can this SaaS website builder continue to win market share?

Reminder: these are show notes that should be read in conjunction with the podcast. Do not expect these notes to be a polished research report.

***As always, listen to the episode on Spotify, Apple Podcasts, or wherever you are subscribed to the show***

Charts

Show Notes

(Ryan) What they do: “Squarespace is an all-in-one platform with everything to sell anything”. Squarespace is a platform that allows all kinds of users to establish a professional-looking internet presence and conduct their business online. Popular Squarespace customer groups include restaurants, photographers, wedding planners, bloggers, artists, and more.

In terms of the customer journey, users that come to Squarespace can immediately start assembling the website they want, often aided by Squarespace’s 100+ templates, then pay a subscription hosting price at the end if they want to make the site public on a specific URL.

Beyond that, Squarespace offers custom domain emails and a variety of add-ons/commerce solutions. So customers on Squarespace can manage their social media accounts, sell online through payment partners, schedule and take appointments, send out email campaigns, and plenty more. Basically, either through a Squarespace in-house tool or 3rd-party solutions, Squarespace customers can easily set up and run their business online without needing to be too tech-savvy.

(Ryan) History: Pretty remarkable founding story. Squarespace was founded in 2003 by Anthony Casalena out of his dorm room at the University of Maryland. At the time, Anthony wanted to make his own blog and realized there weren’t really any great solutions to easily set one up, so he thought it’d be cool to build his own publishing system. Anthony had grown up using computers and writing code from a young age, so he built a working website maker during his early college years. After catching some interest from friends, he decided he wanted to go after this opportunity and make it a real business so he started on a $30,000 loan from his father.

For the first several years, and even after he left college, Anthony was running Squarespace completely on his own. He wrote all the code, answered all customer questions, ran the marketing for Google Ad Words, etc. And keep in mind, this was when Squarespace had a decent amount of customers (I believe it was $650k or something in ARR). Unsurprisingly, he got pretty burnt out managing all these roles, so he tried to hire a different CEO. This didn’t work out well at all, and there were apparently lots of disagreements on different decisions which eventually led Anthony to take back control. Around this time, in 2010, Anthony raised a $38.5 million funding round from Index and Accel Ventures and really began growing the business in the way he wanted.

Since then, like a lot of other companies in the CMS space, Squarespace acquired several smaller businesses that help its customers run their actual operations, including Acuity Scheduling, Unfold, and Tock. They didn’t go public, however, until March 2021.

(Brett) Industry/Landscape/Competition:

The website builder market is quite small excluding WordPress, at only a few billion dollars in spending a year. Squarespace is one of these non-Wordpress website builders.

However, there are a ton of other products companies like Squarespace offer customers including e-commerce selling, payments, email marketing, social media tools, and more.

WordPress has maintained 50%+ of the CMS market for the last decade. However, there are signs that Shopify, Squarespace, and Wix are finally making meaningful market share gains.

From 2011 to now, Shopify went from 0% to 6% market share, Wix went from 0% to 3.5% market share, and Squarespace went from 0% to 2.9% market share. If these share gains continue, WordPress will likely start losing significant market share this decade.

Competitors: Wix, GoDaddy, WordPress (CMS), Shopify/BigCommerce (e-commerce), and then also GoDaddy, Mailchimp, Sprout Social, and Open Table for various other products they offer small businesses.

(Brett) Management and Ownership:

The founder, CEO, and Chairperson of the board is Anthony Casalena. He is only 39 years old. He has 75% voting power in the business giving him total control of the entity.

The BoD has a very standard makeup. There are executives from the technology industry (Wayfair, Getty Images) and VC partners. There are only six members of the board.

Total BoD compensation of $1.38 million in 2021 or 0.2% of 2021 gross profit

Within ownership, there are a lot of VC funds still associated with the stock, but that is not too relevant since Casalena has full control of this thing.

Squarespace has a fairly simple executive compensation scheme (for a public company). They do base salaries and give executives stock options.

Total Executive compensation was $88 million in 2021 or 13.4% of 2021 gross profit

This executive compensation level looks high, however, this was due to the company starting a long-term stock award for Casalena based on stock price tranches that all had to be realized at the time of the compensation plan. However, these shares will not vest unless various stock prices are hit.

Long story short: Casalena is basically paying himself a lot even though he already owns a ton of stock, but it is not as bad as the 2021 GAAP numbers looked.

Here are the tranches (current price: ~$20) for the long-term stock option plan:

(Shares outstanding: 136,829,645. Source for voting power: 2022 Proxy Statement. Source for ownership: Whale Wisdom)

(Ryan) Earnings:

Last 12 months:

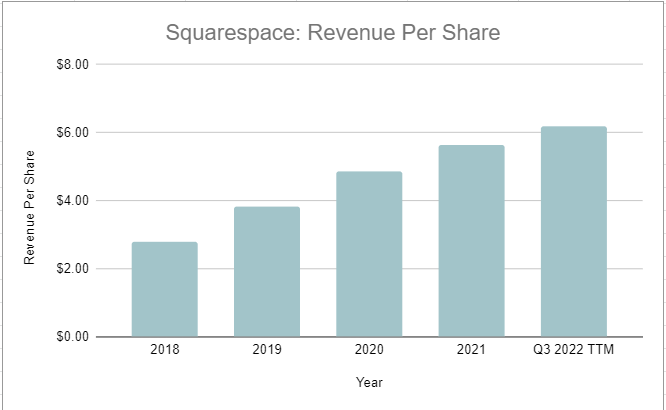

$846 million in revenue, +13% vs the 12 months prior.

83% Gross Margin

$127 million in free cash flow (15% free cash flow margin)

Most recent quarter:

$218 million in total revenue, up 8% YoY

4.2 million unique subscriptions, up 4% YoY (flat sequentially)

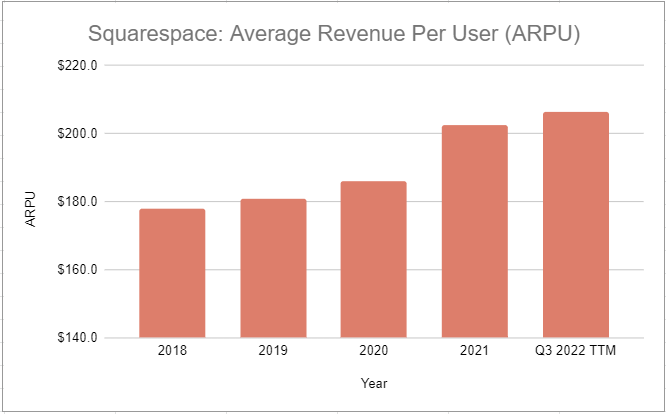

$206.38 average revenue per unique subscription, up 4% YoY

Total bookings increased 10% YoY to $226 million (14% in constant currency)

Commerce revenue grew 13% YoY, but that was driven primarily by the Tock acquisition. Excluding Tock, it looks like commerce GMV actually declined YoY.

$41.4 million in operating cash flow (19% OCF margin), down from last year due to “timing of payments”

They do issue a lot of SBC ($75 million YTD), but authorized a $200 million buyback in Q2 and repurchases have outpaced SBC.

Guiding for ~$140 million in free cash flow for this year

(Ryan) Balance sheet and liquidity:

~$230 million in cash and liquid securities

~$520 million in total debt. Only $30 million of it is current.

Basically, all the debt is in a variable-rate term loan.

In 2019, Squarespace entered into a $350 million term loan then upsized it to $550 million in 2020.

The rate on the term loan is LIBOR + 1.5%. The effective interest rate at the end of the last quarter was 4.63%.

The debt has conditions that Squarespace can’t have a total debt to EBITDA ratio greater than 4.5x, which steps down to 3.75x in 2023.

The current total debt to EBITDA is 4.3x.

But it’s worth including the cash because they could pay some of that debt down early if they wanted, so Net Debt to Adj. EBITDA is 2.4x.

(Brett) Valuation:

Market Cap of $2.78 billion

Enterprise Value of $3.07 billion

EV/GP of 4.39

EV/FCF of 24.2

Anecdotal Evidence:

(Ryan) Feels like the best website-building solution for people trying to showcase their talent or make a portfolio to demonstrate their skills. Especially in categories where design/looks are a top priority.

(Brett) When you visit its product website, you understand right away what Squarespace offers. The first pop-up on Google: “Website builder – Create a website in minutes” with a link to its homepage. When I search “Build a Website” Squarespace is the first ad listing that pops up.

Future growth opportunities:

(Ryan) Tock acquisition. I have some concerns here, but restaurants are a big end market for Squarespace and Tock certainly bolsters Squarespace’s ability to service them. They paid $400 million for Tock right during the heart of COVID, but it basically competes with OpenTable. Starting at $199/month, restaurants can use Tock as their reservation system and for online orders. It seems to have pretty good reviews among restaurant sites from what I’ve seen.

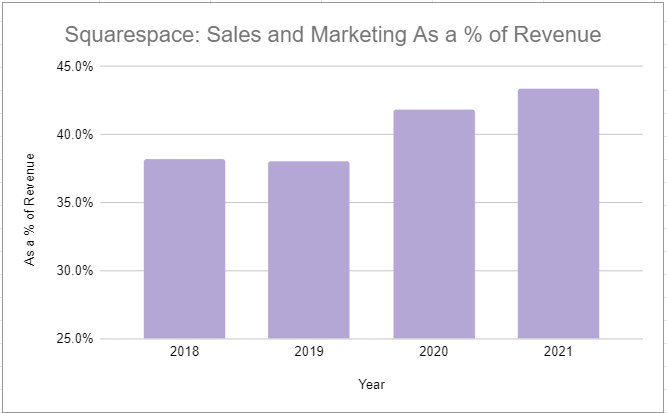

(Brett) Growth in commerce. As with Wix and GoDaddy, Squarespace likely saw how much Shopify has grown with its “arm the rebels” approach to e-commerce/payments for online businesses. Squarespace is trying to replicate that and now offers a ton of e-commerce tools for its website builders. Last quarter, it did $1.4 billion in payment volume through its platform, up 3% year-over-year. For reference, Shopify did $46.2 billion over that same time period. I think you can read that as either bullish or bearish for Squarespace. Why is this so valuable? Because if you get a subscriber that not only pays for website building but uses Squarespace to facilitate transactions, they have much higher lifetime values.

Highlights and lowlights:

Ryan’s Highlights:

Even since the early days, Squarespace has had a focus on profitable growth and management has made it clear that will continue.

I think they have the best-looking designs among website makers and if that’s a user’s focus, Squarespace is probably the go-to solution.

Industry tailwinds. More and more people, even completely non-technical people, are building websites themselves and Squarespace has a well-known brand within the DIY space.

Ryan’s Lowlights:

The Tock acquisition. Tock is a reservation and online ordering system for the hospitality industry that saw robust growth during COVID thanks to its rollout of Tock-to-Go. Squarespace paid $400 million in cash and stock for the business and now with hindsight it feels poorly timed. I’m all for bolstering their commerce offerings but I don’t like paying big price tags to do it.

Floating rate debt. They’ve got a big chunk of debt due mostly in 2025. I think that’s going to limit their ability to buy back too much stock over the next few years.

I’m not 100% sold on Casalena and he controls this ship.

Brett’s Highlights:

My major highlight for website builders is the sustained market share gains in website CMS and the major opportunity that is still out there to take share from WordPress. Squarespace should be one of these beneficiaries. I think investors should ask: what would stop them from doubling their market share over the next five years?

Squarespace is generating cash and returning it to shareholders through repurchases this year while the stock has plummeted. I think this is a good indicator they understand how buybacks can help shareholder returns in the long run.

The combination of fantastic unit economics, recurring revenue, and pricing power capabilities (due to high switching costs) make a website builder like Squarespace an attractive business model.

Brett’s Lowlights:

They were late to the game in e-commerce and online payments, and I worry that – similar to Wix and GoDaddy – Squarespace will lose a lot of customers to Shopify that are e-commerce focused. Given the size of the market opportunity, I don’t think this is a huge failure, but annual GMV might be lower than investors expect a few years from now.

Casalena controls this business from the top down. Yes, given his stock option performance plan he is incentivized to drive shareholder value, but that would already have been the case since he owns 35% of the company. So yes, the fact he decided to give himself this huge stock option plan is a lowlight for me.

The Tock acquisition was expensive. I think the jury is still out on whether this will be a good deal, but they need to execute or else it will end up being a waste of money (the deal was over $400 million).

Bull Case:

(Ryan) Squarespace continues to grow unique subscriptions at 10%+ (3-year CAGR is 16%) while increasing their average revenue per subscription and maintaining ~20% FCF margins. Those 3 things happen, I’d have to think shareholders would have 10%+ returns from here. They’d be generating more than $250 million in FCF within 3 years. 15x on that FCF and you’ve got just under a $4 billion market cap.

(Brett) The thesis for Squarespace is simple: the business continues to gain market share vs. WordPress, driving a steady growth of new customers. ARPU steadily grows through the adoption of commerce tools and price increases. Revenue then grows by 10%+ a year with consistent operating leverage due to strong gross margins. At the current EV/GP multiple, I think it would be hard for shareholders to lose money over any timeframe unless the executive team just makes some boneheaded moves.

Bear Case:

(Ryan) Short-term, I could see some elevated churn as they continue to move away from the accelerated small business formation/website growth that occurred during COVID. If that leads to slower net sub-growth and their interest payments rise due to rising rates, I think it’s possible FCF/share grows at a pretty slow rate.

(Brett) From my seat, the big thesis for non-WordPress builders is that they continue to gain share vs. the open source platform, and I think a little bit of that is reflected in the current stock price. If this doesn’t happen and Squarespace only grows customers by the low single digits each year, I don’t know how well the stock would perform. I do think the floor is pretty high at these prices, though.

More or less interested?

(Ryan) More interested. Bummed to see the floating rate debt on the balance sheet, but the business looks sound and I like the unit economics of these SaaS CMS businesses.

(Brett) More interested. The business model is sound and I think there is a steady tailwind of new customers to acquire.

Stock for next week? (BigCommerce)

Sources and Further Reading

Market share source: https://w3techs.com/technologies/history_overview/content_management/ms/y

Squarespace Review: https://www.sitebuilderreport.com/squarespace-review

Most recent quarterly presentation: https://s27.q4cdn.com/477208693/files/doc_downloads/2022/11/Squarespace-Q3-2022-Shareholder-Letter.pdf

How I Built This: Anthony Casalena: