Our Bet on the Next Berkshire Hathaway

A discounted conglomerate with a great track record based in Nebraska you say?

Reminder: these are show notes that should be read in conjunction with the podcast. Do not expect these notes to be a polished research report. Enjoy the episode and listen wherever you get your podcasts!

YouTube

Spotify

Apple Podcasts

Chit Chat stocks is presented by:

Public.com just launched options trading, and they’re doing something no other brokerage has done before: sharing 50% of their options revenue directly with you.

That means instead of paying to place options trades, you get something back on every single trade.

-Earn $0.18 rebate per contract traded

-No commission fees

-No per-contract fees

By sharing 50% of their options revenue, Public has created a more transparent options trading experience. You’ll know exactly how much they make from each trade because they literally give you half of it.

Activate options trading at Public.com/chitchatstocks by March 31 to lock in your lifetime rebate.

Options are not suitable for all investors and carry significant risk. Certain complex options strategies carry additional risk. Options can be risky and are not suitable for all investors. See the Characteristics and Risks of Standardized Options to learn more.

For each options transaction, Public Investing shares 50% of their order flow revenue as a rebate to help reduce your trading costs. This rebate will be displayed as a negative number in the “Additional Fees” column of your Trade Confirmation Statement and will be immediately reflected in the total dollars paid or received for the transaction. Order flow rebates are only issued for options trades and not for transactions involving other assets, including equities. For more information, refer to the Fee Schedule.

All investing involves the risk of loss, including loss of principal. Brokerage services for US-listed, registered securities, options and bonds in a self-directed account are offered by Open to the Public Investing, Inc., member FINRA & SIPC. See public.com/#disclosures-main for more information.

Show Notes

(Brett) Nelnet Business Services (otherwise called enterprise and payments software for educational organizations)

“It is our belief that on a stand-alone basis this business could arguably be valued nearly equal to the whole of Nelnet at its current market value. Munger would definitely be excited by this business as it creates a lot of cash flow, has dominant market share, a large moat, is not too difficult to understand, and has an industry-leading management team”

Yes, you are going to be confused learning all the names of Nelnet’s subsidiaries. Welcome to the club.

NBS houses Nelnet’s software and payments subsidiaries for educational organizations. These include tuition management, payment processing, and other software tools focused on the administration department at schools, mainly in the United States.

We don’t get a full P&L for NBS, but it looks like a great business with low risks and good cash flow conversion. It probably has decent pricing power as it would be hard to “rip out” these solutions from an administrative office.

It generated close to $500 million in revenue in 2023 and $91 million in operating earnings. I think the operating margin could be slightly higher if they stopped reinvesting for growth, but probably not too much. Perhaps at maturity, we could forecast a 25% margin.

For reference, when we talk about book value, NBS brings barely anything to the “net worth” of Nelnet on its balance sheet. But it is likely much higher than this.

Discussion Q: What is this business worth? Can operating earnings double to ~$200 million by 2030?

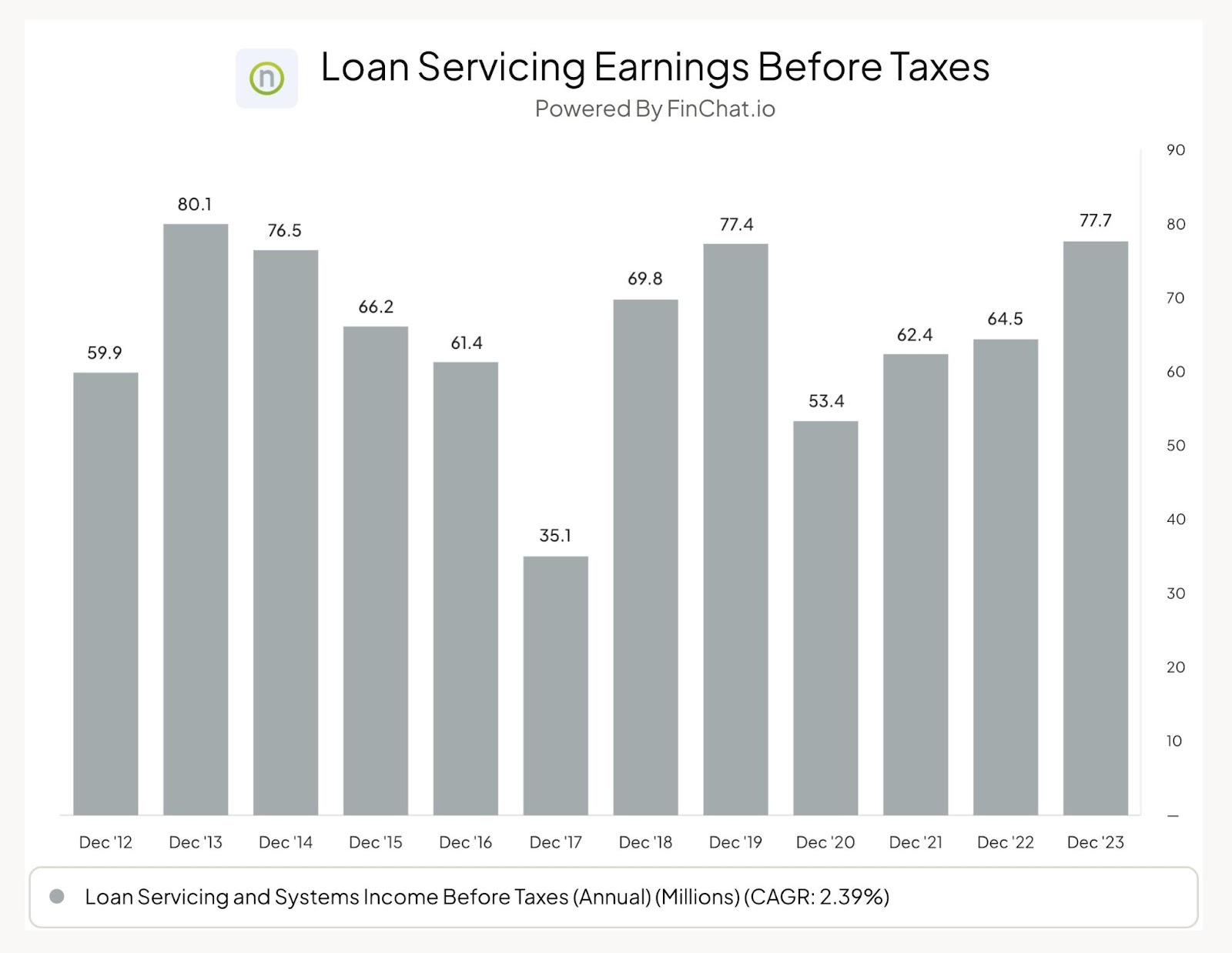

(Ryan) Nelnet Diversified Services (Loan Servicing Division): What happened this year? Do we think this business is important to the thesis?

Quick reminder on what this segment actually does: When a lender lends money to a borrower, there’s a layer of work being done under the hood that tends to go unnoticed. This layer includes the actual distribution and collection of money, maintenance of financial records, and a central dashboard for borrowers to interface with during the payback period. That’s what Nelnet does. In some cases, they are the actual lender themselves, but more often than not they are a 3rd party servicer acting on behalf of a customer (most commonly the US govt.)

Let’s start with what happened this year:

“When the pandemic hit, every federally held loan was put into a non-interest-bearing non-payment status, first using executive authority and then under the Coronavirus Aid, Relief, and Economic Security (CARES) Act. The CARES Act forbearance was extended by President Trump through the 2020 election and then extended multiple times by President Biden. The Biden administration also announced the President’s forgiveness plan utilizing executive authority based upon a unique interpretation of the Health and Economic Recovery Omnibus Emergency Solutions (HEROES) Act passed back in 2003, which they argued gave the President emergency authority to forgive loans in the absence of Congressional student loan forgiveness legislation.”

Noordhoek goes on to say:

“Throughout the 3.5-year CARES Act forbearance period… we were instructed by the U.S. DoE to maintain appropriate staffing levels in preparation for the inevitable and seemingly imminent R2R. We were frequently asked by Congress for our plans for R2R practically each time a repayment date was announced. We were repeatedly promised, “This time is it, we are definitely going back into repayment,” and asked for staffing plans. We ramped up hiring and stayed ready to provide high-quality service in an unprecedented time period, only to be told forbearance would be extended.”

But even with the constant layoffs and a cut to the fees the US govt was willing to pay Nelnet, the segment still generated just under $80 million in earnings before taxes.

Final thoughts here: I don’t love this business. It’s fine because it generates a good amount of earnings, but there’s a lot of customer concentration here and we’ve now seen what can happen when that’s the case. I don’t expect it to grow that quickly. But $724 million in EBT over the last 10 years is nothing to shy away from either.

(Brett) What is going on at Nelnet Financial Services? What is this segment worth?

I would formally like to thank Ryan for letting me take the most confusing and annoying part of Nelnet’s business.

Kidding aside, this is the most important segment for Nelnet in the near term. Likely the long-term as well. If we look at its $3.2 billion+ in book value, over $2.5 billion will come from NFS.

So, what is NFS? Well, it is a few things. Management just consolidated multiple segments into NFS, but it is essentially anything where Nelnet is making a loan or making an investment (excluding solar). These include:

FFELP student loans and other student loans

Real estate investments

Insurance operations

Asset management (White Tail Rock)

Nelnet Bank

Insurance and Asset Management are both small and irrelevant today. I want to focus on FFELP, other loans, and the Nelnet Bank. FFELP is where Nelnet was, unsecured loans and Nelnet Bank are where they will be. Hopefully, all contribute to book value per share increasing.

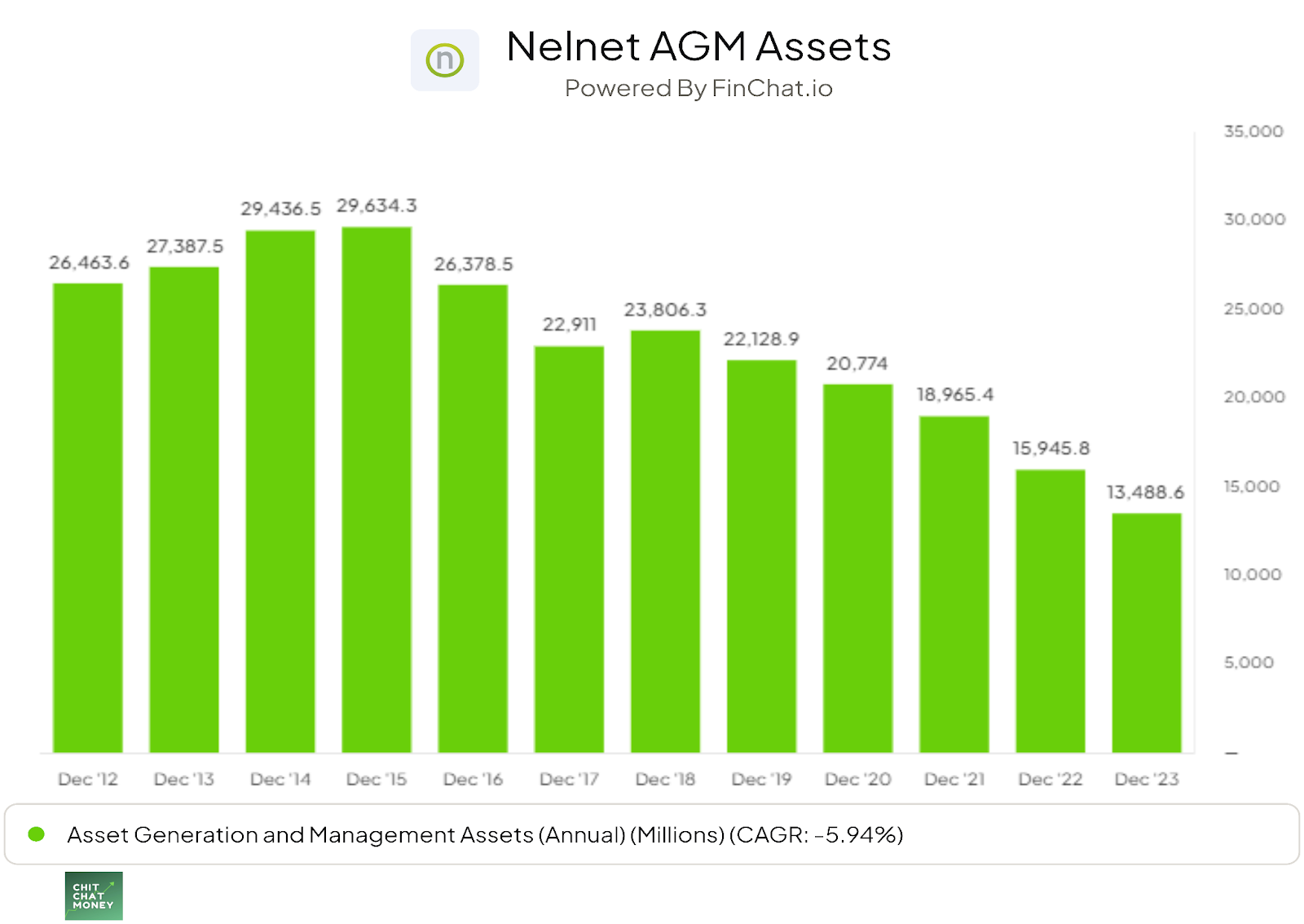

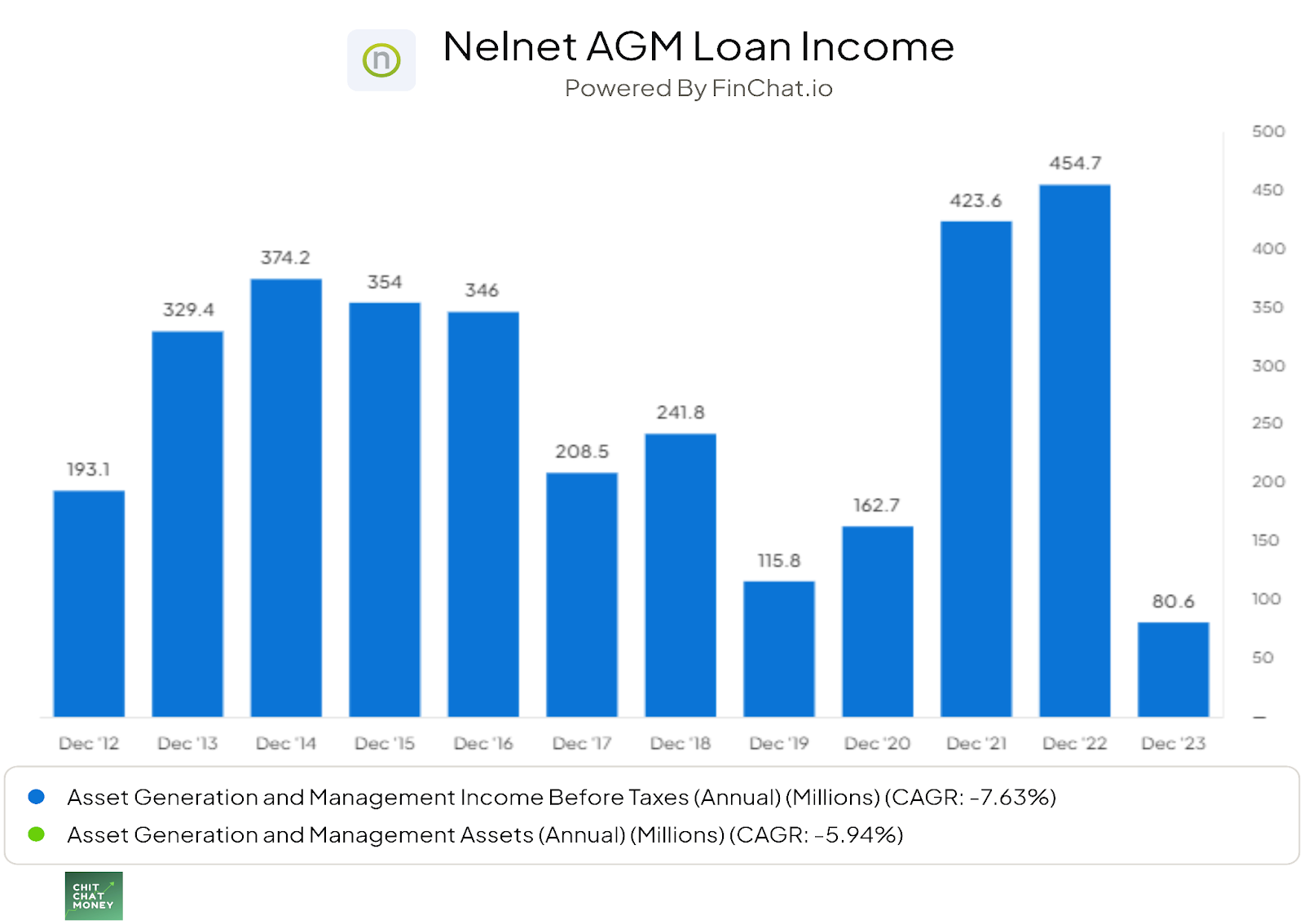

FFELP loans are student loans originated by Nelnet or purchased from third parties where the principal payments are all but guaranteed by the government. The company takes on a lot of leverage and securitizes these loans, which have been quite profitable. However, new loans cannot be made and the segment is in “run-off” mode, which you can see from the charts below.

The downside to having a huge amount of FFELP loans is they are interest rate sensitive. We don’t need to get into the details of this but investors need to understand that as interest rates rise, the cash flow from Nelnet’s loan book can decline. I will also not pretend to fully understand this segment. The good news is, in two years it will be irrelevant to the Nelnet story. Honestly, that day cannot arrive soon enough.

Management tries as best as possible to hedge out the effect of interest rates. They had some hedges in place during the interest-rate hiking cycle of 2022 and 2023. However, during the banking panic of last year, they got spooked about liquidity and decided to unwind hedges:

“To minimize the Company's exposure to market volatility and increase liquidity, on March 15, 2023, the Company terminated its derivative portfolio hedging loans earning fixed rate floor income ($2.8 billion in notional amount of derivatives). Through March 15, 2023, the Company had received cash or had a receivable from the clearinghouse related to variation margin equal to the fair value as of March 15, 2023 of the derivatives used to hedge loans earning fixed rate floor income of $183.2 million, which included $19.1 million related to current period settlements”

Here’s what I like about Nelnet: they admit when mistakes were made. They were caught slightly flat-footed and had to act defensively during the small banking panic in the Spring of 2023. They also may have overreacted. From the 2023 shareholder letter (I will paraphrase for the podcast and leave the full excerpt for the newsletter):

“2023 was a year during which your chairman ate a lot of humble pie served cold with a return on equity (ROE) of 3.4%—not close to our long-term goals. The primary ingredients to my humble pie included a less-than-stellar acquisition and the impact of interest rates and banking industry disruption on our liquidity and investment positions”

“The year was also a painful transitional one for our asset-backed securities investment portfolio. In March, we had roughly $2.0 billion in ABS investments and personal loans on our balance sheet with $1.2 billion in short-term leverage. We also had a large derivative position of $2.8 billion, which carried mark-to-market risk. We got caught with very loose pants when Silicon Valley Bank failed. We didn’t have a lot of opportunistic liquidity as the tide went out, and our pants started to slip down our legs—so we created a lot of liquidity very quickly, which came at an immediate cost of around $6 million to sell $325 million in leveraged ABS and $2 million to refinance one of our student loan securitizations. In total, this freed up almost $500 million in cash. The refinancing of the student loan trust hit GAAP earnings for $26 million (unamortized debt finance costs) but had no impact on longterm cash flow.”

“We also unwound our derivative portfolio, which led to a lost opportunity cost of tens of millions, given what rates did the rest of the year and where they are projected to be at the end of 2024 when $2 billion out of the $2.8 billion derivative portfolio would have fully matured. Recently, we have put $400 million in new derivatives on our balance sheet, which hedge our fixed-rate loans and retained ABS portfolio. We have continued to deleverage our portfolio. In March, we had $2.0 billion in ABS and personal loans on our balance sheet and $1.2 billion in short-term leverage. Today (February 2024), we have approximately $1 billion in ABS and personal loans with approximately $170 million in short-term leverage.”

What I find reassuring with Nelnet is that they:

Admitted their mistake.

Didn’t end up losing that much money in the grand scheme of things.

Still generated a positive ROE in 2023 when facing perhaps the largest headwind they will ever face.

The stated goal from Nelnet is to take the earnings generated from FFELP and reinvest them into other loans, assets, investments, etc.

A lot of the cash flow is reinvested into new loans on the open market that management believes they can get a good rate of return on:

“During 2023, the Company purchased $556.1 million of private education, consumer, and other non-FFELP loans. AGM's competition for the purchase of loan portfolios includes banks, hedge funds, and other finance companies”

Look at the table below. They have invested over $1.5 billion in the last 10 years into originating private consumer loans and loan residuals from third parties. We can track the progress of these loans with the growth of book value on the balance sheet.

I also don’t have many concerns that management will be honest about the successes and failures of this strategy.

The third important piece to NFS is Nelnet Bank. This is a small, fully-owned bank that was given a charter in November 2020. In November 2023 it exited its “de novo” period and can now operate more freely. It is not relevant to earnings today, but something management is excited about investing in. Likely because it will reduce the cost of funding.

Nelnet Bank has not been profitable, likely due to interest rate hikes impacting the deposit side of things. In 2023, the bank’s net interest margin (NIM) was just 1.85%, which I think could be higher if interest rates didn’t rise so much. If interest rates remain stable, we’ll see what they can do. They also need to get to a decent size in order to start getting operating leverage on overhead costs. Growth in loans and growth in deposits will be important to track going forward.

Nelnet Bank is a small portion of Nelnet’s book value today ($140 million). But it is a great asset for them to have that has a chance to reinvest with a huge runway if it can figure out a way to consistently grow deposits.

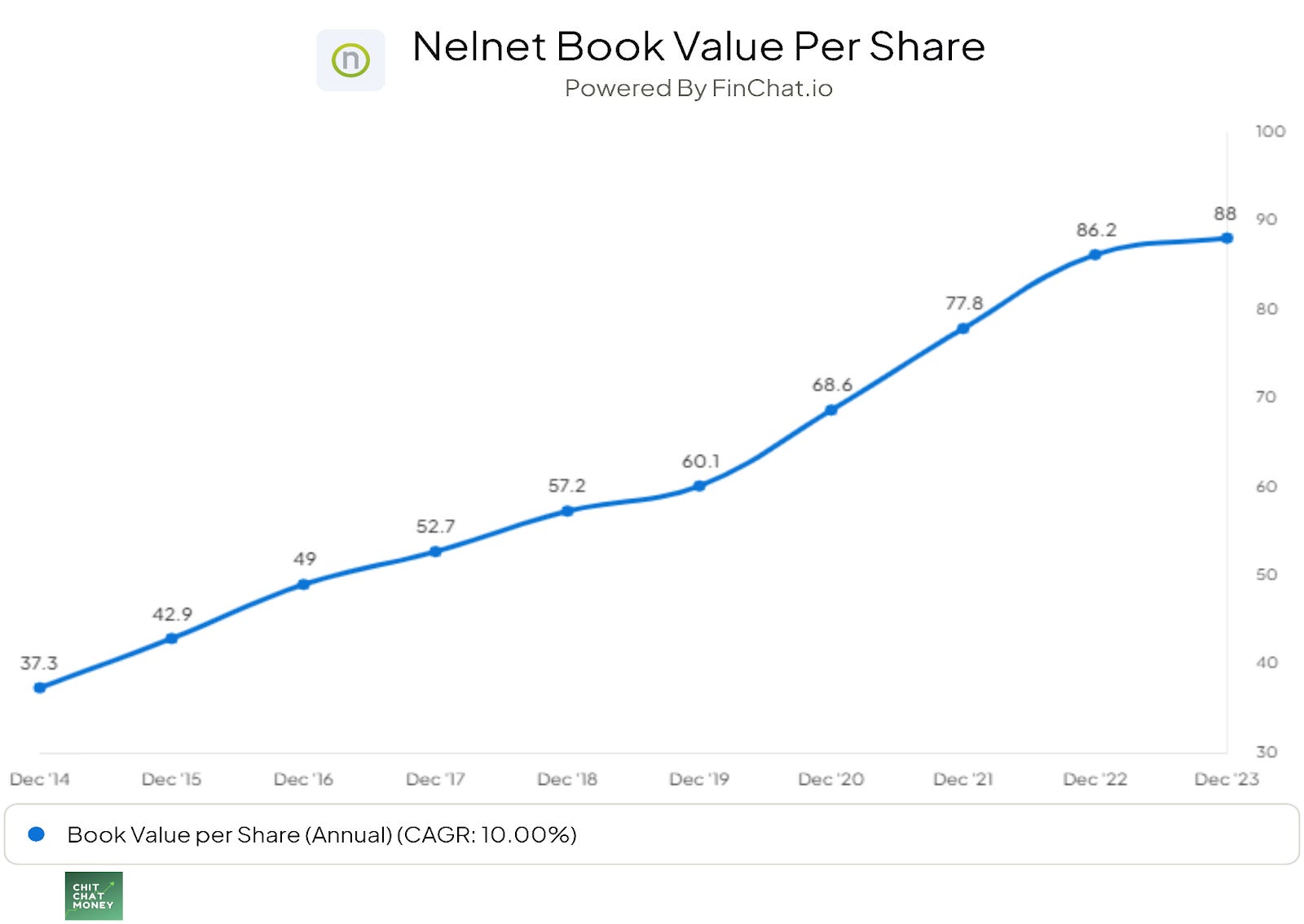

So to bring it all together: How much is NFS worth? I’m not exactly sure. Historically, NFS generated fantastic ROEs and was the main driver of book value per share compounding at 16.2% per year since 2004. However, now we are exiting the “guaranteed return” era of FFELP and entering an era of uncertainty with the bank, unsecured loans on the corporate balance sheet, and maybe even insurance. 2023 was a tough year with interest rates, but they made some mistakes.

Can these strong ROEs continue? I would say probably. But after 2023, I am a little less confident. They need to earn my confidence with these new strategies, which I think is reflected in the under-performing share price.

Does this deserve to trade at 1x BV? 1.5x? 2x? Let’s discuss on the podcast. Today, the equity value of NFS is approximately $2.6 billion.

(Ryan) Solar

They used to call this Nelnet Renewable Services. Nelnet’s role was as a tax equity investor in solar energy partnerships. This meant that Nelnet – along with its co-investors – invested money to develop solar energy projects around the country. In return, the company got cash flow plus tax equity credits, equal to 26% - 30% of the project cost. (It’s 30%-40% now).

But they went ahead and bought a company called GRNE Solar. GRNE Solar is a contracting company that builds solar projects for other people. Here’s what they said on last year’s 10-K versus this year’s shareholder letter:

Last year’s 10-K: “The acquisition of GRNE Solar provides technical know-how, customer relationships, a talented workforce, and revenue streams to Nelnet’s expanding renewable energy business. The acquisition gives the Company an ability to realize a diversified revenue stream by generating a fee-based service from its EPC and operations and maintenance (O&M) services”

This year’s shareholder letter: “In 2022 we acquired a solar construction business to leverage our tax credit and syndication business and expand our development capabilities. We had another good year in the tax credit and syndication business… Our solar construction business, on the other hand, had a very rough year with escalating construction costs. Higher interest rates reduced residential demand and made solar projects more costly. Add in some mispriced projects along with us being (almost over our ski tips) outside our circle of competency, leading us to writing off $21 million dollars in goodwill and intangibles along with an annual pre-tax operating loss of $34 million.”

Not really sure what to think about this segment. I don’t love that they are saying it’s outside of their competency, but the solar partnerships seem fine. They have invested a total of $271.9 million in solar partnerships over the years. Maybe they can sell off the construction business but I would count this as maybe a zero or even worse to the overall Sum of the Parts.

(Brett) What is the value of its Allo Communications stake?

“The Company believes the fair value of its voting membership interests in ALLO is significantly greater than its carrying value”

Nelnet owns a 45% voting stake in Allo Communications, which is a leading fiber-to-the-home provider in Nebraska and some neighboring states. It also has a preferred stock worth $155 million. Let’s say the preferred is actually worth $155 million.

Due to its want to save taxes, Nelnet is using some accounting mambo jumbo (official term) to reduce the stated value of its 45% stake in Allo Communications. It will be “worth” zero at the end of Q1. But, management thinks it is worth much more than this.

Today, Allo has approximately 150k customers (rounding up from EOY 2023). In 2022, it had 131k customers. So growing fairly quickly. It generated $150 million in revenue last year. If you value each customer at $2.5k, this is worth $375 million. Perhaps they are worth more? Perhaps they will reach 200k customers soon and be on the way to $500 million in value? I’m not sure, but I do know these fiber-internet customers are valuable.

They also get support from the government (a key tenet of the Nelnet business model!). There is the BEAD program to get fiber internet to underserved communities. Allo fits this bill and should see continued support in the near future.

The issue I have with valuing Nelnet’s stake in Allo is the fact the company has $715 million in debt outstanding. They are taking on a lot of leverage to grow. I think it can work, but this is where a lot of the enterprise value resides today.

So, perhaps Allo is worth a lot. Perhaps it will be worth a lot more in the future if it keeps up this growth and raises prices. But is Nelnet’s stake worth that much compared to its $3.2 billion market cap? I don’t think so. Software, lending, loan servicing, and HUDL are much more important IMO.

(Ryan) Other Investments (VC Portfolio)

Nelnet has investments in 91 entities and funds in its VC portfolio. The total carrying value of the whole portfolio is $285.5 million.

The largest is Hudl (technically called Agile Sports Technologies). Their investment in Hudl is currently carried on its books at $165.5 million and that’s estimated to be about a 20% stake, last time it was reported. Interestingly “During the first quarter of 2023, the Company acquired additional ownership interests in Hudl for $31.5 million from existing Hudl investors. This transaction was not considered an observable market transaction (not orderly) because it was not subject to customary marketing activities.”

So that carrying value is even more understated. Here’s what they had to say in this year’s letter:

“We remain extremely optimistic about our investment in Hudl. We are currently carrying the value of this investment on our books of $165 million, and we believe the actual market value of this investment is significantly higher than our carrying value… Hudl provides more than 230,000 teams across 40 sports and in 150 countries the insights to be more competitive.”

Let’s try to run the math. Here are the prices for high schools, which is their largest market.

Now if we assume that most companies choose either the gold or platinum service, which seems pretty likely given that most teams want to be able to save more than 100 hours of video, the average price would be right around $2,450/year. $2,450 * 230,000 teams = $564 million in annual recurring revenue.

Now that’s certainly a guess, but that doesn’t seem completely unreasonable. I assume a business like that would probably get 5x-10x ARR in the public markets which means it’d be valued between $2.8B to $5.6B in market cap. On the low end there, that would mean Nelnet’s stake would be worth more than $500 million.

(Both) What do you think this entire business is worth?

(Ryan) I’ll keep my analysis pretty simple. I think if we assign a value to all their subsidiaries on their own, it’d add up to be worth much more than the current market cap.

Education & Payments, I think should be worth at least 20x EBT. That’s $1.8 billion.

Loan servicing is maybe worth ~10x EBT or ~$800 million.

Then is everything else worth at least $500 million. Certainly. You’re getting an understated Hudl investment, a financing arm that is expected to generate $1B in cash flow over the next 5 years, a cable business with loads of recurring revenue customers now, and a bunch of other investments that probably add up to around $300M in carrying value.

So I’m just going to keep owning it. I honestly have no intention of selling this for quite a long time. Management is honest, and they’ve shown an ability to be successful over time. It’s probably in the never-sell camp for me.

(Brett)

I think there are four main contributors to intrinsic value at Nelnet: Financial services/loans/bank, NBS (software/payments), loan servicing, and Hudl. Let’s try to value both

NFS + Nelnet Bank at book value is $2.6 billion. However, they have a history of generating well above 10% ROE and I think this deserves to trade at a slight premium to BV. At 1.25x BV, this is $3.25 billion in value

Education software/payments is probably worth around $2 billion

Loan servicing is probably worth around $1 billion (low growth, uncertainty means lower multiple

The Hudl stake is likely worth $1 billion imo

Sum it together and this business is worth $7.25 billion, Add in the smaller stuff, solar, Allo Communications and give a better premium to BV of NFS (a good financial like this should trade at 1.5x BV) and it might be worth $10 billion. I think I would sell at a $15 billion market cap. So, clearly not today and I think it is quite undervalued.

Sources and Further Reading

Nelnet investor relations: https://www.nelnetinvestors.com/home/default.aspx