Sunday Finds + 3 Thoughts From Last Week

Charter Communications + The Joint Corp.

Welcome to Chit Chat Money’s Sunday Finds + 3 Thoughts From Last Week. In this newsletter you will find three topics I thought about last week, links to shows we’ve recently released, and links to some interesting articles, podcasts, and tweets. Check out the archive here.

1. Is Tik-Tok on the outs in the West?

Potentially big news came out this week from the Federal Communications Commission (FCC, link to tweet also below):

An FCC Commissioner, Brendan Carr, wrote to Apple and Google on Tuesday, requesting the companies remove TikTok from their app stores for “its pattern of surreptitious data practices.” This comes after BuzzFeed News reported last week that TikTok’s staff in China had access to U.S.-based users’ data up until January.

It’s crazy to think that the United States is allowing an application from one of our top geopolitical rivals to dominate entertainment hours in the country. This is like if in the 1950’s USSR TV was one of the top broadcast TV channels. Even if the app is harmless (the cynic in me says to doubt that), there’s no positive reason to keep it operating.

And it’s not like this is some vital company to the well-being of our nation. In fact, you could argue that Tik-Tok is likely a net negative on society. Yes, China and the United States are tied together in things like pharmaceuticals, commodities, clean energy, and semiconductors, which could get thorny if the relationship between the two nations further deteriorates. But who cares about a short-form video app? All this is doing is transferring advertising dollars (generally) from Western companies to Chinese shareholders. Do we really think this is in the best interest of American citizens and corporations?

China has banned all non-domestic media and communications platforms from operating in its country. It seems like the logical and low-risk move for the United States to return the favor.

Did I just convince myself to get long Facebook/Meta Platforms? Jeez, that stock looks optically cheap right now. If Tik-Tok gets banned, things could be looking pretty cozy for the social media incumbent.

2. Slowing down hiring vs. layoffs

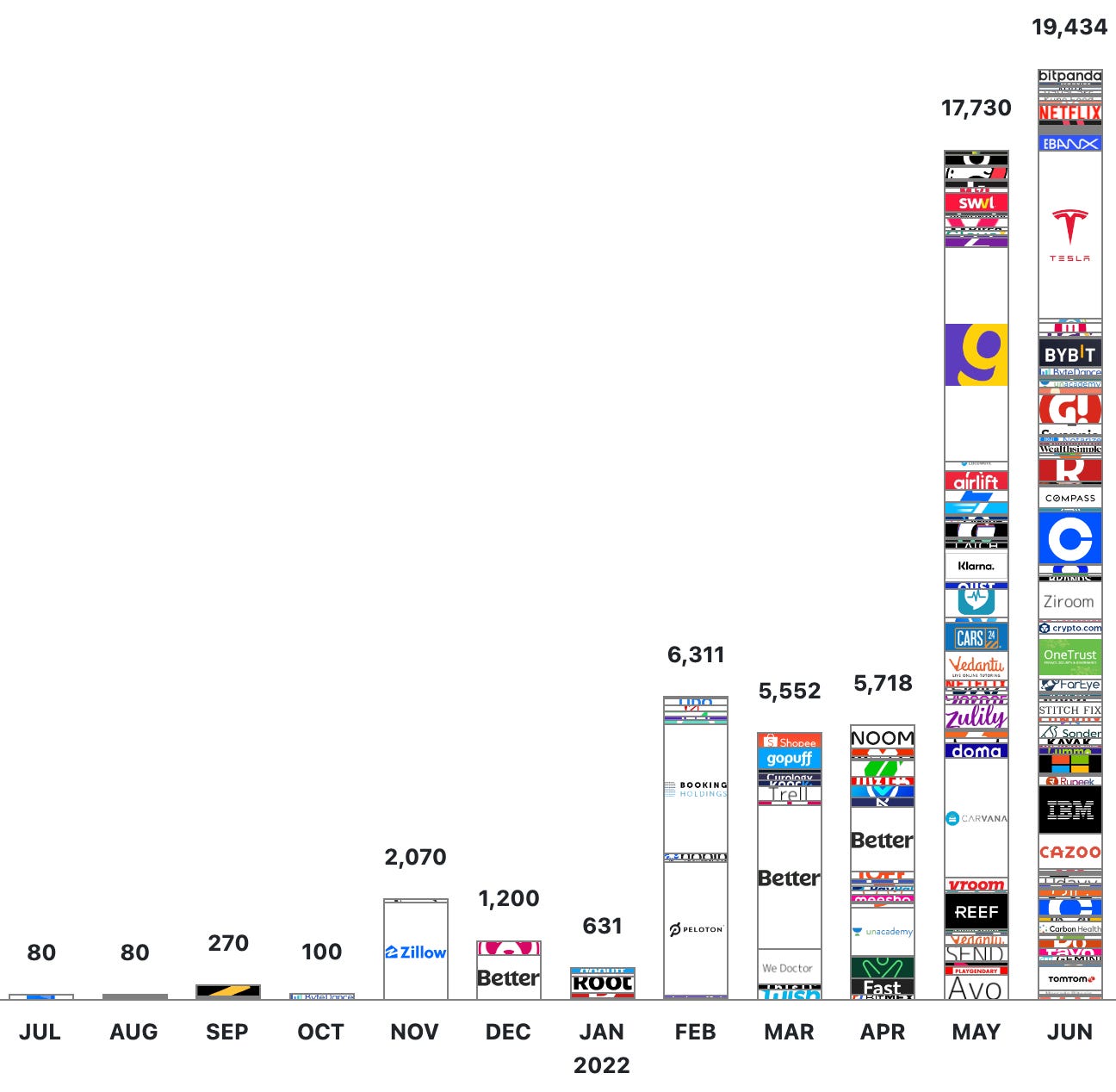

A big theme over the last few months has been a huge downturn in hiring in the software/internet/technology markets (i.e. what you think of as Silicon Valley). There was a nice chart floating around quantifying the layoffs this week:

And these are just the announced firings. You can clearly see a pick-up in February and a huge acceleration over the last two months. If we were in a bubble at some point in the last two years (I think we were), the air is definitely coming out, and quickly.

There have also been negative reactions to companies announcing a “slowing down” of hiring. Two stocks I follow that have done this are Spotify and Meta Platforms, with both share prices taking a hit when the news leaked out. I’m sure there are plenty of others.

While everything can correlate in the short run during a bear market, I think there is a huge difference between a company slowing down hiring compared to another laying off 10% of its workforce. For example, Meta Platforms (Facebook) is still going to hire 6k - 7k employees this year, just not the 10k they originally planned. This is not a company in shambles, even though it may seem like that in the media sometimes. Coinbase, on the other hand, doesn’t look good at all when it lays off 18% of its workforce.

Trimming the fat during a tougher operating environment can be great for a company’s long-term margin structure. You learn what expenses (and people) are not helping your organization succeed, and what are. Hopefully, this is what happens to the true secular growers coming out of this downcycle.

3. FTX is buying BlockFi for parts

The crypto markets continue to repeat the script from 1907:

FTX is swooping in to buy crypto lender BlockFi for pennies on the dollar, sources told CNBC.

The term sheet is almost over the finish line and expected to be signed by the end of the week, according to three sources, who asked not to be named because the deal discussions were confidential. FTX is expected to pay roughly $25 million, one source said, 99% below BlockFi’s last private valuation. Another person with direct knowledge of the deal pegged the price closer to $50 million. Jersey City, New Jersey-based BlockFi was last valued at $4.8 billion, according to PitchBook.

(the situation may change when you are reading this, things are moving fast in crypto right now)

According to the report, equity investors in BlockFi are now completely wiped out. The company supposedly lets people “Do more with your crypto” by lending out users’ cryptocurrencies to speculators. Turns out that high-interest-rate loans on magic beans was not a sustainable business model. Who knew!

FTX seems to have a lot of cash right now, but I don’t understand its endgame. The founder, Sam-Bankman Fried, admitted on Bloomberg that the whole industry is essentially just a Ponzi scheme (his words, not mine). So, what is he buying here? How does this eventually end up creating shareholder value? I get that FTX can’t let the crypto market totally collapse, as that would be the end of its business. But I don’t understand how this will ever (outside of the exchanges) create a business that generates free cash flow for shareholders in a sustainable way.

And if there is a “systemic” risk in crypto, who cares? Unlike a real financial crisis (2008, 1907, etc.), very few people (and most very rich) would get impacted by the decimation of crypto prices. In fact, it might have a huge deflationary effect in the real world by lowering energy prices and opening up semiconductor markets. Which we all could use right now.

See you next week,

Brett

***Our fund, Arch Capital, may own securities discussed in this newsletter. Check our holdings page and read our full disclosure to learn more.***

***Want our free weekly wrap-up delivered to your inbox each week? Subscribe here***

Catch up on Our Shows From Last Week

3 Good Reads

Why I’m Biased Against Stock Options - Geoff Gannon

I am most concerned in situations where the board, top management, etc. have small stock ownership relative to their compensation and where they have very few votes. These two things usually go together. So, like a board where everyone is paid $300,000 a year and nobody owns any stock. That’s concerning because $300,000 a year is definitely large enough to create bad incentives where the director wants to keep their board seat more than they want to increase the stock price in the long-run. Having few votes is also concerning, because it means current control is in the hands of people who can’t necessarily count on continuing control. If the CEO, CFO, board, etc. don’t own a lot of stock – they are basically just running things up to the point where shareholders disagree with them. They seem to be in control. But, their control can be tested and they have no stable support among the shareholder base other than the typical “status quo” bias that you see in a lot of proxy voting.

The proposed shield would be about the size of Brazil, and the bubbles for it could be manufactured and deployed in space, possibly out of silicon — the group has already experimented with creating these “space bubbles” in the lab.

3 Things I Think I Think: Flation, Flation, Flation - Pragmatic Capitalism

Another big theme of mine in recent years was that the Fed was behind the curve both ways. In 2020 I repeatedly said the Fed would have to backpedal by raising rates to get ahead of inflation in 2021. But what I got wrong was that they would panic right when inflation was surging. I’ve actually been shocked by their aggressive stance and I frankly think it’s been a little reckless and overreactive. In short, it looks like inflation was on the verge of turning over at the end of 2021, but then the Russian invasion caused commodities to surge which made the Fed think that inflation was more permanent than they thought. Except it now looks like they panicked into a supply side issue and now they’re exacerbating what was already an underlying demand side problem.

1 Good Listen

'Markets can stay irrational for longer than you can stay solvent' is a classic maxim for investors, but it holds true for journalists too. In this episode, we speak with the Financial Times's Dan McCrum and Paul Murphy (Tracy's old boss) about their multi-year effort to expose fraud at Wirecard, a German payments giant that went spectacularly belly-up after billions of dollars were found to have gone missing. Dan, who's just written a book about his experience called "Money Men," explains how he first spotted problems at what was once described as "Europe's greatest fintech," and how hard it was to convince others of the truth. Rather than going after Wirecard itself, German authorities went after the journalists and short-sellers who were warning of the scheme.

Smart and Funny Tweets: