Sunday Finds + 3 Thoughts From Last Week

Podcasts on GoDaddy and Blackstone this week

Welcome to Chit Chat Money’s Sunday Finds + 3 Thoughts From Last Week. In this newsletter you will find three topics I thought about last week, links to shows we’ve recently released, and links to some interesting articles, podcasts, and tweets. Check out the archive here.

Podcasts From Last Week:

Is Blackstone a Misunderstood Compounder? With John Rotonti (Ticker: BX)

Investing Power Hour #37: FTX Testimony, State of Video Games, Private Equity Software Investments

Chit Chat Money is presented by:

7investing, an investing service where you get monthly stock recommendations, best buy portfolio analysis, and in-depth market research. Use our code “MONEY” at check out and get $100 off your annual subscription for life!

1. Avoiding Getting Sniped by Takeout Bids

This week, Coupa Software announced an $8 billion takeover bid from Thoma Bravo:

Coupa shareholders will receive $81.00 per share in cash, which represents a 77% premium to Coupa's closing stock price on November 22, 2022, the last full trading day prior to media reports regarding a possible sale transaction involving the company. The transaction consideration also represents a premium of approximately 64% to the volume weighted average closing price of Coupa stock for the 30 trading days ending on November 22, 2022.

A 77% premium seems pretty darn great, right? Well, in this case, not so much. Here’s Coupa’s three-year price chart:

Unless you bought shares this Fall, Thoma Bravo’s takeout bid will likely give you a permanent loss if you were invested in Coupa Software.

These “snipings” can be extra frustrating because you can lose money even if you end up being right about the business three or five years from now.

With tons of dry powder at private equity firms and the software bear market, these undercutting bids could get more and more frequent in the coming quarters.

So, as investors with no control over what a management team does, how can we avoid these snipings? I think it is pretty simple:

Focus on valuation. If you don’t overpay (as Coupa investors definitely did in 2020/2021), it is less likely you’ll get taken out under your cost basis.

Invest in businesses where you trust management.

Keeping these two factors in mind will not guarantee you avoid a takeover snipe, but I think it makes it much less likely.

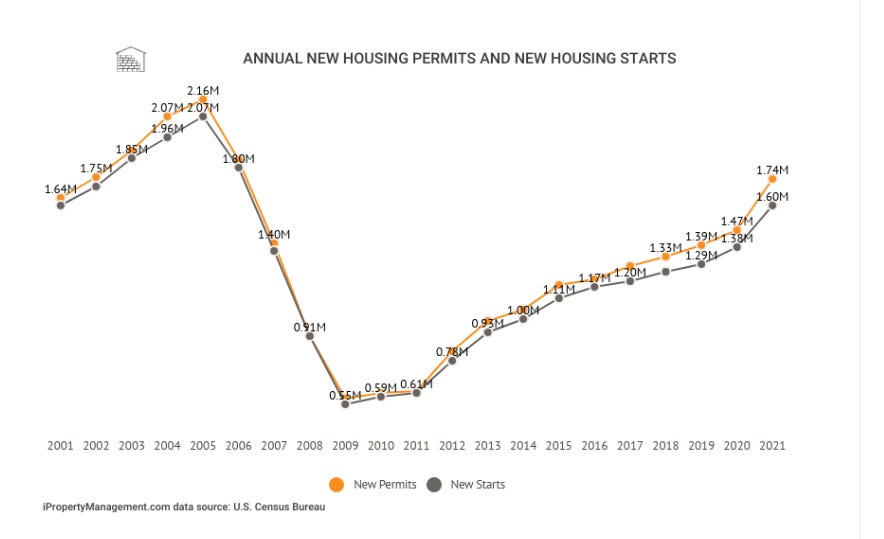

2. Is Airbnb causing a housing “shortage”?

There was an interesting paper I found this week analyzing how Airbnb and short-term rentals affect housing prices. From the abstract:

At the median owner-occupancy rate zipcode, we find that a 1% increase in Airbnb listings leads to a 0.018% increase in rents and a 0.026% increase in house prices.

Of course, correlation does not equal causation, but I think this idea has some merit. Using the paper’s numbers, a 200% increase in Airbnb listings equates to a 5.2% increase in home prices for the area. While not astronomical, many regions have experienced this sort of growth or worse in the last five to ten years.

This trend of turning into a mini-landlord seems to have accelerated greatly during the pandemic:

The key part of that tweet is “buying a new home and keeping their old home.” Every time this happens and one of the properties turns into a short-term rental, it’s almost like the supply increase should be negated, as it is not increasing shelter supply for local citizens. So yeah, I think the growth of Airbnb definitely has an effect on the housing affordability crisis and may be creating a phantom shortage if a bubble in short-term rentals has formed.

Over time, Airbnb can help to solve these issues by moving more towards long-term rentals. For example, they just launched a new partnership for apartment renters to work with their landlords to list units on Airbnb. But the problem won’t get solved overnight and may get worse before it gets better.

You can talk in circles all day about factors affecting U.S. housing affordability. But I know one way guaranteed to solve this crisis: build a lot more housing. And it looks like the country is slowly but surely starting to do this:

I’m very interested in watching what the housing market does over the next 2 - 3 years. There are so many dynamic variables at play it feels impossible to predict.

3. Is Iger the Jack Welch of Disney?

There’s more and more evidence coming out that Bob Iger (current CEO at Disney) doesn’t really care about anyone but himself:

He made a fantastic acquisition to purchase Marvel. But ever since then, his decision-making has not aged well. Reasoning:

The Fox acquisition. Terrible misallocation of capital.

Late to the internet/streaming. Inexcusable.

Embracing China at the worst possible time.

Mangling the Star Wars franchise just to get some billion-dollar box office numbers in the first few years after the acquisition.

Did I mention the Fox acquisition?

He also seems to have undermined the company in order to make himself look better. Yes, hindsight is 20/20, but these are some absurd missteps for a man getting paid a boatload of money each year. Disney in the 21st century is/was one of the easiest businesses to run. The only way to destroy it is through huge cultural problems, which Iger seems deadset on doing to serve his own ego.

It’s no surprise then to see Disney’s stock price essentially flat since 2014. I don’t think it is crazy to expect the world to look at Bob Iger in 2030 the same way we look at Jack Welch today. Admired for decades, but once you peel back the onion you see that there was something rotten at the core.

See you next week,

Brett

***Our fund, Arch Capital, may own securities discussed in this newsletter. Check our holdings page and read our full disclosure to learn more.***

***Want our FREE weekly wrap-up delivered to your inbox each week? Subscribe here***

3 Good Reads

Consoles and Competition - Stratechery

Sony’s pivot after the (relatively) disappointing PlayStation 3 was brilliant: if the economic imperative for 3rd-party developers was to be on both Xbox and PlayStation (and the PC), and if game engines made that easy to implement, then there was no longer any differentiation to be had in catering to 3rd-party developers.

Instead Sony beefed up its internal game development studios and bought up several external ones, with the goal of creating PlayStation 4 exclusives. Now some portion of new games would not be available on Xbox not because it had crappy cartridges or underpowered graphics, but because Sony could decide to limit its profit on individual titles for the sake of the broader PlayStation 4 ecosystem. After all, there would still be a lot of 3rd-party developers; if Sony had more consoles than Microsoft because of its exclusives, then it would harvest more of those 3rd-party royalty fees.

The Triumph of Experience Over Hope - Lindsell Train

But whilst others may operate in isolation from longer-term events, our time frames expose us to the constant flux of modern life. Think how much has changed over the past 25 years. The millennium bubble and bug, 9/11, smartphones and social media, the GFC, Brexit, and so on. Personal experience emphasises recency, but change is not just a 21st century phenomenon. Over the past 100 years, the shape of industry has transformed completely. In the 1900s railways dominated, making up around two thirds of the US market (according to data compiled by the LBS’s Elroy Dimson, Paul Marsh, and Mike Staunton for their landmark Triumph of the Optimists book). Today however, railways contribute less than 1%, ceding authority to the internet. Multifarious ‘tech’ has swelled to a third of the US equity market, with the bulk of this coming from just five businesses (Apple, Microsoft, Alphabet, Amazon, and Tesla at the time of writing), only two of which are older than our implied 25-year time horizon. As Dimson and co. note, “Of the US firms listed in 1900, more than 80% of their value was in industries that are today small or extinct”. Clearly, we face both disruption and opportunity, each paced to challenge long-term investors like us.

Ideas That Changed My Life - Morgan Housel

Room for error is underappreciated and misunderstood. It’s usually viewed as a conservative hedge, used by those who don’t want to take much risk. But when used appropriately it’s the opposite. Room for error lets you stick around long enough to let the odds of benefiting from a low-probability outcome fall in your favor. Since the biggest gains occur the most infrequently – either because they don’t happen often or because they take time to compound – the person with enough room for error in part of their strategy to let them endure hardship in the other part of their strategy has an edge over the person who gets wiped out, game over, insert more tokens, at the first hiccup.

1 Good Podcast

The Most Amazing Breakthroughs of 2022 - Plain English

Derek talks to economist and writer Eli Dourado about the most exciting scientific and technological discoveries of the year, from the AI toys that everybody seems to be playing with to lesser-known breakthroughs in bioscience, clean energy hardware, and precise atomic manipulation.

Smart and Funny Tweets: