Sunday Finds + 3 Thoughts From Last Week

Warby Parker + Petco

Welcome to Chit Chat Money’s Sunday Finds + 3 Thoughts From Last Week. In this newsletter you will find three topics I thought about last week, links to shows we’ve recently released, and links to some interesting articles, podcasts, and tweets. Check out the archive here.

1. Keep It Simple, Stupid

I highly recommend reading the “Trying Too Hard” speech I linked to as a read this week. I’ve already read it twice, it is really that good. Well, it also confirms my biases, which I enjoyed.

The speech is from 1981, but could easily be talking about investors today.

My big takeaway was that the majority of information we are fed as investors is useless when trying to decide what assets to buy. You can see it with all the topics floating around the industry lately. Will the Fed raise interest rates this month? Will it be 0.50% or 0.75%? Is the economy in a recession? What is the definition of a recession? Will supply chains fix themselves this year or next? Have corporate profit margins peaked? And on, and on, and on it goes.

Frankly, the majority of these topics are useless when deciding to buy a common stock. Why? Because they are unforecastable. We knew this 40 years ago (as discussed in the speech), and yet, we still waste countless hours trying to figure them out today. I’d rather just avoid them altogether

We are big adherents of keeping things as simple as possible when making an investment decision. If a business is complicated, or there are tons of questions we need to get right in order to meet our return hurdle, we pass on the stock. Simple as that. An easy example of this is the energy industry. If a thesis relies on us predicting what the price of Oil or some other commodity will be five years from now, it is unownable in our minds (because commodity prices are unpredictable).

There are only three questions we ask ourselves before making an investment:

Is the company in a durable industry with a competitive advantage? (this is the only way we can be confident in making any estimates on cash flow generation)

Is the stock trading at a reasonable price? (i.e. don’t overpay for the cash it will generate over the next 3 - 10 years)

Do we trust management?

That’s it. These are tough enough questions to answer, and really all we feel comfortable analyzing. Going beyond with fancy modeling or highly complex ideas probably does more harm than good. But it sure does feel smart.

Keep it simple, stupid.

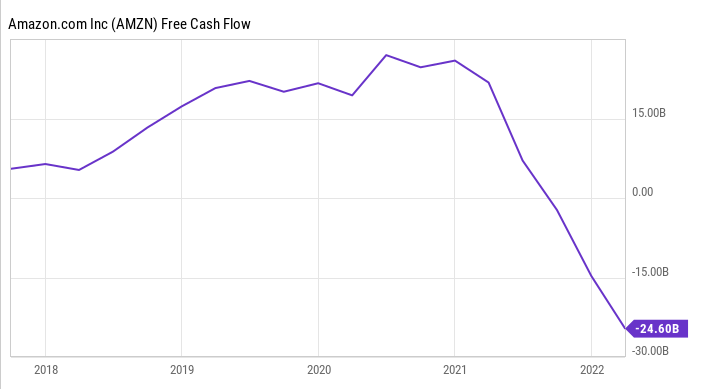

2. Are Amazon’s e-commerce profits determined by gas/shipping prices?

Amazon had a mixed bag with its Q2 results. Of course, AWS continues to be a monster, but what caught my concerning eye was retail.

Through the first half of 2022 Amazon’s North American retail business generated $144 billion in revenue but had an operating loss of $2 billion. Even at its current absurd scale and vertical integration, Amazon is still not insulated from rising input costs. And this is with a healthy Prime membership base and a high margin advertising segment that did almost $9 billion in revenue last quarter. It baffles and concerns me as a potential investor that this segment cannot generate a consistent operating profit.

If gasoline, supply, and labor costs remain elevated (in other words, sustained inflation) is Amazon’s e-commerce model not viable in North America? I don’t know the answer to that question, and maybe they will flip back to profitability in the next few quarters, but it is something to watch for sure.

Eventually, you have to generate cash flow, right?

3. Meta (Facebook) proves its fragile moat

In other big tech news, Meta/Facebook had a bad earnings report with revenue declining by 1% and operating income tanking 32% year-over-year.

Compared to other companies like Google, Amazon, or Apple, Facebook’s moat seems way more fragile to me, and why it deserves a healthy multiple discount. We are seeing this with the chaos over at Instagram right now, which is scrambling to copy Tik-Tok while also keeping its user base happy. So far, it has not gone well. What happens if Instagram fails to execute here? Copying Tik-Tok puts the app at a disadvantaged position and opens it up to competition from new social media apps trying to replicate the old Instagram (like BeReal). There are so many difficult questions to answer here, and this is without considering the absurd spend on Reality Labs/Metaverse.

I sure wouldn’t want to pay up for this business, especially right now. But there’s obviously potential for fantastic returns for shareholders this decade if these are only short-term hiccups.

See you next week,

Brett

***Our fund, Arch Capital, may own securities discussed in this newsletter. Check our holdings page and read our full disclosure to learn more.***

***Want our free weekly wrap-up delivered to your inbox each week? Subscribe here***

Catch up on Our Shows From Last Week

Not So Deep Dive: Warby Parker (paywalled)

Investing Power Hour #17: Q2 Earnings Season, Shorting Crypto, Chipotle Earnings

Sunday Finds is brought to you by CCM+, our subscription podcast/research feed. For $5 a month, subscribers get:

A weekly Not So Deep Dive episode covering the basics of an individual stock.

A newsletter with research notes, charts, and valuation work for that week’s premium podcast episode.

Access to our historical research folder for all of our CCM+ episodes.

A monthly Arch Capital investment fund episode covering a stock we own in our limited partnership.

Sign-up directly through Spotify or Apple Podcasts. On other podcast players, you can build a private RSS feed through this link: https://anchor.fm/chitchatmoney/subscribe

3 Good Reads

Trying too Hard - Dean Williams

The final idea we talked about was that there are two ways we can try to gain an edge over the market. The one that most of us choose is to try to generate superior information. To know more than anyone else. The other choice is to be better at measuring value than others and not to care very much about what other investors think they know. To hold cheaper securities by today’s standards and to let the future speak for itself.

PayPal Deep Dive - The Stock Market Nerd

While PayPal started with a single service, it has built out a vast suite of utility-building products for both merchants and consumers. All of these products are aimed at supporting what PayPal calls its 2-Sided (consumer + merchant) Network scale. The wonderful thing about PayPal’s business model is that its success is intimately based on its stakeholders enjoying more payment volume through their networks, or convenience in their daily lives. It can only thrive by providing more value which eliminates conflict of interests. PayPal teamwork makes the dream work.

Acquisition Accounting and Financial Analysis - 310 Value

So, a business, with some limitations, could write off in the first year of service, 100% of the value of an asset that was purchased. This 100% write off goes from 2017 to 2023. After 2023, the Bonus Depreciation declines 20% per year, until it reaches 20% in 2027. So, if an acquirer buys a business, it is possible that they generate no tax depreciation for making that investment, even if the acquired business is rich in depreciating assets. Furthermore, any amount paid in excess of the target’s net worth is deemed to be “goodwill”, which is not tax deductible. This type of acquisition favors the sellers, as they receive all the cash agreed to and have no ongoing liabilities to worry about.

1 Good Listen

Why Instagram Broke Its Square - Land of the Giants

When Mark Zuckerberg bought Instagram in 2012, he promised he would be hands-off with the company’s curated aesthetic and simple features. But as Facebook scaled the startup into a social media juggernaut, tensions flared. Instagram’s founders would leave, and it’s now a very different app than when it first started. But are the changes setting the company up to compete in the future? Or is Instagram losing the magic that made it great in the first place?

Smart and Funny Tweets: