The Best Investor In Britain?

How Terry Smith beats the market with quality stocks

Reminder: these are show notes that should be read in conjunction with the podcast. Do not expect these notes to be a polished research report. Enjoy the episode and listen wherever you get your podcasts!

YouTube

Spotify

Apple Podcasts

Chit Chat stocks is presented by:

Public.com just launched options trading, and they’re doing something no other brokerage has done before: sharing 50% of their options revenue directly with you.

That means instead of paying to place options trades, you get something back on every single trade.

-Earn $0.18 rebate per contract traded

-No commission fees

-No per-contract fees

By sharing 50% of their options revenue, Public has created a more transparent options trading experience. You’ll know exactly how much they make from each trade because they literally give you half of it.

Activate options trading at Public.com/chitchatstocks by March 31 to lock in your lifetime rebate.

Options are not suitable for all investors and carry significant risk. Certain complex options strategies carry additional risk. Options can be risky and are not suitable for all investors. See the Characteristics and Risks of Standardized Options to learn more.

For each options transaction, Public Investing shares 50% of their order flow revenue as a rebate to help reduce your trading costs. This rebate will be displayed as a negative number in the “Additional Fees” column of your Trade Confirmation Statement and will be immediately reflected in the total dollars paid or received for the transaction. Order flow rebates are only issued for options trades and not for transactions involving other assets, including equities. For more information, refer to the Fee Schedule.

All investing involves the risk of loss, including loss of principal. Brokerage services for US-listed, registered securities, options and bonds in a self-directed account are offered by Open to the Public Investing, Inc., member FINRA & SIPC. See public.com/#disclosures-main for more information.

Show Notes + Follow-up

I hope everyone enjoys this latest episode on Terry Smith as we continue our series of highlighting investors with strong track records. We aim to learn from these great investors to improve our own investing process.

By sharing with you all, we want you to improve your process as well.

Our show notes were not very readable this week, so I have compiled what would work for the newsletter as well as some follow-up thoughts on the recording. For more information on Fundsmith, check out their website (links at the end of the newsletter).

Upcoming episodes for the podcast include interviews with Jim Gillies/Todd Wenning, Devin LaSarre from Invariant, and stock analysis shows on Dream Finders Homes and GoGo. Should be a fun month for Chit Chat Stocks. Thank you to all the loyal listeners!

(Ryan) Who is Terry Smith? Let’s give some background

Terry Smith was born in England in 1953. He attended Stratford Grammar School then went on to study History at University College Cardiff where he graduated in 1974. A bit of an unorthodox background. Nothing there really points to him taking an interest in finance. However, after he graduated, he rejected an offer for a research fellowship and decided he wanted to pursue a career in business, so he joined Barclays Bank.

He was at Barclays for a little over 10 years and during that time he became an associate of the Chartered Institute of Bankers “a global professional education body for bankers, based in the UK”. He got a great education in the banking industry throughout those 10 years. During those 10 years, he also picked up an interest in investing. In 1984, he joined a stock brokerage firm and over the next 6 years was considered the top-rated banking analyst in London.

Ironically, that banking expertise ended up actually deterring him from investing in banks. Here’s what he says about it:

“Having spent the first decade of my career working in a bank and then becoming a top-rated bank analyst, I find that people often express surprise that I never invest in bank shares. But I think it is precisely because I understand banks that I never invest in their shares… Why? Firstly, I never invest in anything that requires leverage to make an adequate return. Banks have a very small amount of equity to support their balance sheet.”

Continuing on with his career, I found this next part pretty interesting. In 1989-1990, he joined UBS as the head of UK Company Research. However, in 1992, he was fired because he wrote an analysts circular called “Accounting for Growth” that dug into the ten intentionally misleading accounting of certain businesses. The article was really well received and people encouraged him to publish it as a book. He decided to, and some of those businesses, who were friends with Terry Smith’s employer, complained. They asked Smith to take it down, and he said no. This is a time when we kind of started to see how smug (is that fair?) Smith could be.

Another example of Smith demonstrating some cojones was actually in the 80’s prior to his book debacle. A week after he joined that brokerage firm (BZW), he wrote a sell suggestion on Barclays. Well, Barclays was the parent company of BZW at the time.

One last story, before we get to the rest of his career. One time, at a black-tie client dinner, there was a certain client who was apparently irritating him, so Terry Smith apparently head-butted him.

Anyway, after he was fired his career seemed to be a little less colorful. He joined an up-and-coming brokerage firm called Collins Stewart that went on to have a lot of success, and in 2010 he launched his own fund management business, Fundsmith. For the first 4 years he was running Fundsmith, and he was also the CEO of a huge brokerage firm. In 2014, he resigned and began focusing solely on Fundsmith.

What is Fundsmith?

Fundsmith was founded by Terry Smith in the United Kingdom on November 1st, 2010. It currently has an estimated $44.5 billion in AUM (using US dollars and the prevailing exchange rate), and $32 billion in the flagship equity fund.

From Nov 1st, 2010 to the end of February 2024, Fundsmith returns net of fees are 596.3% (15.7% annualized).

This compares to these relative benchmarks:

392.1% total return for S&P 500 ETF owners (SPY)

253.7% total return for MSCI World index

746.7% total return for the Nasdaq 100 (QQQ)

Not too shabby. But how have they outperformed the market? What leads to these strong returns?

Fundsmith’s strategy

They articulate it in various ways, but it seems to me that Fundsmith wants to identify high-quality businesses trading at reasonable earnings multiples. Like other “quality” investors, Fundsmith is focused on the combination of high returns on invested capital (ROIC) and a long runway for reinvestment.

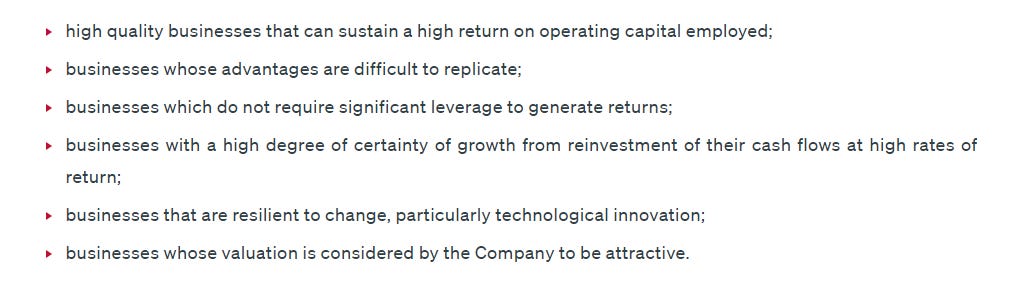

Here are six criteria they have for investments to be included in the portfolio:

This isn’t rocket science. They want strong competitive advantages, no need for leverage, a long runway for reinvestment, minimal technological disruption risk, and a reasonable valuation. Nothing more.

They want to hold businesses for as long as possible but are not afraid to sell off stocks if the valuation gets egregious. Importantly, they also don’t shy away from changing position sizing if a stock they like gets a much more attractive valuation. For example, they increased their weighting into Meta Platforms in late 2022 when everyone hated the stock.

Here are the top 10 holdings in the portfolio, according to the Fundsmith website:

Part of me thinks that they have strayed away from the “no technological risk” criterion (Novo Nordisk, Microsoft, Meta Platforms, etc.) but you can also see that they favor strong consumer brands (L’Oreal, LVMH, Philip Morris) with minimal competitive threats.

They pride themselves in having low portfolio turnover and harp again and again on how transaction costs can add up for highly active investors.

Ten Rules for Investors

Here are 10 rules Smith lays out for investors that he has written publicly a few times in the past:

If you don’t fully understand it, don’t invest

Don’t try to time the market

Minimise fees

Deal as infrequently as possible

Don’t over-diversify

Never invest just to avoid tax

Never invest in poor-quality companies

Buy shares in a business which can be run by an idiot

Don’t engage in “greater fool theory”

If you don’t like what’s happening to your shares, switch off the screen

I think all these are helpful. However, sometimes it can pay to invest in poor-quality businesses. If you are given the opportunity to purchase a balance sheet worth $100 million at a price of $10 million, you take that bet every time.

An underrated part of Fundsmith’s strategy

Fundsmith focuses on cash flow conversion as an indicator a business is of high quality. I think investors underrate the importance of this metric.

The stocks in the Fundsmith portfolio consistently have better cash flow conversion than the market average. This gives the companies more flexibility to reinvest aggressively without the need for leverage and/or return cash to shareholders.

A downfall of the Fundsmith strategy

No investment strategy is perfect. One thing I kept coming back to when reading Fundsmith’s documents and writing is the focus on quantifying ROIC. I’ve never understood what costs should be included in the “invested capital” part of the equation for companies, especially asset-light ones.

Should we be including R&D? What timeline should we use for deprecation (data centers highlighting this dynamic recently)? Among other questions. Different investors could come up with wildly different denominators for their ROIC calculations.

Fundsmith seems to want consistently high ROIC in its portfolio companies. Which has kept them out of Amazon for years, even though it is clear that the company passes the rest of its checklist.

Maybe it is best for Fundsmith to have this high bar in order to keep them from investing in bad companies. But to do that you are giving up the chance to invest in the Amazon’s of the world, companies with strong ROICs that aren’t quantitatively showing it today.

Is this strategy replicable?

The strategy at Fundsmith is easily replicable for individual investors. All they are doing is buying and holding large-cap companies. It is what most of us do.

One piece of pushback investors might give on Fundsmith and its outperformance is the fact it launched in 2010, right when quality large-cap companies began to go on a great run.

I don’t like this line of thinking. First, returns are returns. You can’t just say it was luck someone like Fundsmith decided to buy quality companies in 2010. They chose the strategy for a reason: because it leads to outperformance through the market cycle.

Second, it’s not like Fundsmith seemingly did well while still underperforming index funds. They have beaten the S&P 500 since inception during one of its greatest bull runs ever. Investors shouldn’t expect 16%+ forward returns from Fundsmith in the next two decades, but you shouldn’t expect 10%+ returns from the S&P 500, either.

I think this strategy can slightly outperform the S&P 500 (or most other indices) through all market environments. How much longer do they need to prove themselves?

Listen to our full hour-long episode for all our thoughts!

Have a great week,

Brett

Sources and Further Reading

Fundsmith website:

Latest annual meeting: