What Is The Best Type of Moat?

And why it matters

YouTube

Spotify

Apple Podcasts

This week, we welcomed John Rotonti of the JRo Show to the Investing Power Hour live podcast.

John loves studying the philosophy around fundamental investing, so I tweeted a question on moats:

A lot of responses said branding was a weak moat. Others said that economies of scale and/or capital intensity were weak moats.

Most preferred network effects, regulatory capture, and high switching costs (which can all be intertwined, for example Visa/Mastercard).

I agree that branding is a weak moat, on average. Perhaps a better way to think about it is that brands can be strong for a short while and deliver huge outsized profits. But, it is hard to have confidence in brand durability except on rare occasions (Ferrari, Coca-Cola, etc.).

I think brand moats work well when combined with other competitive advantages. American Express earns outsized profits because it is a strong brand and has a network effect. Apple earns outsized profits because it has a strong brand and high switching costs (and blue bubbles, sigh).

Unlike a lot of these responders, I like economies of scale and capital intensity as moat drivers. I think it is much more predictable than a brand-driven moat, giving me confidence in durability. This comes back to the Nick Sleep idea of scaled economies shared (Costco, Amazon) where the low margin and increasing customer value proposition at scale continually separates the company from the competition.

Of course, capital intensity requires, well, a lot of capital. Profits have to be reinvested to maintain and grow the moat, which is money that cannot be redistributed back to shareholders.

This is why asset-light businesses with high switching costs, regulatory capture, and/or network effects are the undisputed superior business models.

Some of the widest moat stocks in this category have delivered phenomenal long-term returns.

FICO has compounded at a 24% clip since 1990

Visa has compounded at a 21% clip since going public in 2008:

Microsoft has compounded at a 22.7% clip since 1990:

(although it is now more capital-intensive)

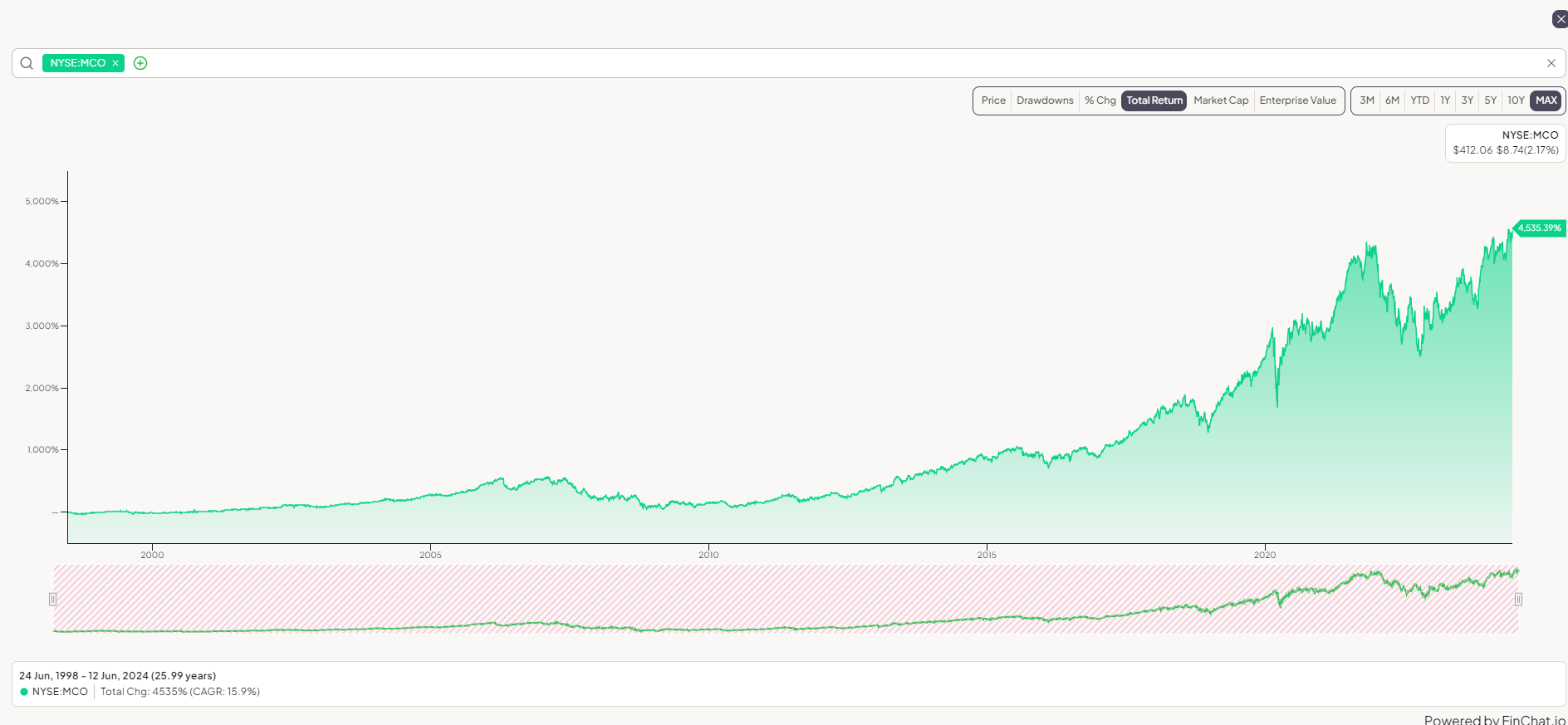

Moody’s has compounded at a 16% clip even with the GFC scandal:

Adobe has compounded at a 19% clip:

I could go on. These are capital-light businesses with major competitive advantages that allow them to generate growing free cash flow over decades. If paired with a decent capital allocator that only needs to say “Hey shareholders, take this cash” you get market-beating returns.

Gross profit royalties, as Buffett calls them.

One might argue a company such as Costco has a wider moat due to its huge economies of scale and cost advantage. I can buy that argument.

But is it a “better” moat? Costco’s stock has compounded at 17% since it went public and is perhaps the best example of economies of scale leading to strong long-term stock performance. It has also had quite the multiple expansion.

It just simply can’t be better than another wide moat stock that is not capital intensive. Because the capital intensity eats up the cash that is supposed to be returned to you as a shareholder:

Source: Buyback Capital.

Therefore, the best businesses are those that:

Have wide moats from network effects and switching costs

Are not capital intensive

Can grow without new capital

Have a rational capital allocator at the helm

Is that so much to ask?

Chit Chat stocks is presented by:

Public.com just launched options trading, and they’re doing something no other brokerage has done before: sharing 50% of their options revenue directly with you.

That means instead of paying to place options trades, you get something back on every single trade.

-Earn $0.18 rebate per contract traded

-No commission fees

-No per-contract fees

Options are not suitable for all investors and carry significant risk. Option investors can rapidly lose the value of their investment in a short period of time and incur permanent loss by expiration date. Certain complex options strategies carry additional risk. There are additional costs associated with option strategies that call for multiple purchases and sales of options, such as spreads, straddles, among others, as compared with a single option trade.

Prior to buying or selling an option, investors must read and understand the “Characteristics and Risks of Standardized Options”, also known as the options disclosure document (ODD) which can be found at: www.theocc.com/company-information/documents-and-archives/options-disclosure-document

Supporting documentation for any claims will be furnished upon request.

If you are enrolled in our Options Order Flow Rebate Program, The exact rebate will depend on the specifics of each transaction and will be previewed for you prior to submitting each trade. This rebate will be deducted from your cost to place the trade and will be reflected on your trade confirmation. Order flow rebates are not available for non-options transactions. To learn more, see our Fee Schedule, Order Flow Rebate FAQ, and Order Flow Rebate Program Terms & Conditions.

Options can be risky and are not suitable for all investors. See the Characteristics and Risks of Standardized Options to learn more.

All investing involves the risk of loss, including loss of principal. Brokerage services for US-listed, registered securities, options and bonds in a self-directed account are offered by Open to the Public Investing, Inc., member FINRA & SIPC. See public.com/#disclosures-main for more information.

So, what 'other' moat does Ferrari or Hermes have? I'd argue that a brand can be one of the most powerful moats, but we just give out the moat 'brand' pretty quickly to a company. Network effects can be very strong, but it can disappear just as fast, because of the same network effect.

I think, without a doubt, economies of scale are the strongest moat (as long as they play their cards right) and then a strong brand.