Why I Own This Boring 100 Bagger Stock (Ticker: ORLY)

When everyone disregards a quality business with a strong management team, magic can happen

YouTube

Spotify

Apple Podcasts

This week, we have another one of our stock research episodes. Ryan leads the research this week, covering O’Reilly Automotive (Ticker: ORLY), a stock he already owns in his portfolio.

You likely know the brand, but did you know the stock is one of the best performers of the last 30 years? This boring business has generated 425x returns for investors since its 1993 IPO.

That means $10,000 turned into $4.25 million for a stock hiding in plain sight.

Need I say anything else?

I would highly recommend listening/watching this week’s episode. Below, we have Ryan’s show notes on O’Reilly, powered by our friends at Finchat.io.

Brett

What does O’Reilly actually do?

I think most people will recognize the O’Reilly name, but if you don’t O’Reilly Automotive is a specialty retailer for automotive aftermarket parts, equipment, accessories, and more. That means they sell everything from hard parts (batteries, chassis parts, belts, etc.) to supplies and equipment (filters, engine additives, oil, wiper blades) or even accessories (floor mats, seat covers, car scents). Basically, anything that you need or want for your car after you have taken it off the lot, you can pretty much get at an O’Reilly’s.

The majority of customer transactions are non-discretionary. I don’t think O’Reilly gives out an exact figure here, but Autozone, which is the most direct competitor O’Reilly has, states that 84% of the products they sell are either critical or maintenance parts. In other words, the vast majority are non-discretionary. O’Reilly groups their customers into 2 buckets: Do-it-Yourself (DIY) and Do-it-for-Me (DIFM). DIY, which accounts for ~53% of sales, is just the standard individual customers. DIFM are more of the professional service providers like the local auto repair shops and that accounts for the remainder of sales so ~47%.

What do their stores look like? How much do they cost to build?

Now when we look at the actual O’Reilly stores, they have standard features across most of their locations that are fairly unique. First off, the signage is very recognizable. The contrasting green “O’Reilly’s” on a bright red painted wall is very easy to see and you know exactly what it is. Secondly, there is always ample parking which is important especially in more urban locations because it gives people an easy way to access the stores.

On average, a new store costs between $3 and $3.3 million to set up. That includes the cost of land acquisition, building construction, fixtures, vehicles, net inventory investment, and computer equipment. And the average O’Reilly store generates $2.6 million in sales annually.

What does their supply chain look like?

O’Reilly’s supply chain is really its secret sauce. It’s the backbone of this business that drives much of its competitive advantages.

They have a reliable and vast assortment of inventory. Given the time-sensitive nature of many customer transactions, they need to have access to a number of parts quickly. And thanks to O’Reilly’s 30 distribution centers and 385 Hub Stores, every O’Reilly location has same-day or overnight access to 152,000 SKUs. Every O’Reilly store has a POS system that is integrated with their proprietary electronic catalog that has been built out over time and a system to easily order parts to be delivered to the stores.

Here’s a quote from a VIC writeup from 2017:

“O’Reilly is the gold standard of inventory management. Approximately 50% of stores receive intraday deliveries 4-8x per day directly from a dedicated distribution center. Another 35% of stores get access to distribution centers up to twice per day from Hub stores. 10% of stores get intraday service from a hub but not directly from a distribution center due to distance constraints. The remaining 5% of stores do not receive intraday deliveries but receive deliveries five times per week. This system allows ORLY to maintain the best coverage of products/parts while maintaining the lowest inventory per store.”

A couple other things I’ll mention quickly:

FirstCallOnline.com. This is the website that pro customers can visit to order any parts they might need.

Delivery. O’Reilly can deliver to local Pro and Individual customers as its stores are equipped with vehicles for just that.

Private label brands. “Our proprietary private label products are produced by respected automotive manufacturers, meet or exceed original equipment manufacturer specifications, and consist of house brands and nationally recognized proprietary brands, which we have acquired or developed over time.”

Bargaining power with suppliers. Their accounts payable is 131% of their inventory. This helps alleviate the big cash flow lags you typically get with a retailer.

Here’s a quote from a more recent VIC writeup:

“Net income has converted to free cash flow (including subtracting minimal stock-based compensation) at 107.3% over the past nearly 14 years. Over that time, ORLY has taken Accounts Payable/Inventory from 44.3% to 133.9% in Q3’23. Inventory turns over that time have increased from 1.4x to 1.7x. Its proprietary brands penetration has steadily grown and now stands at 50% of its mix, which has helped increase its gross margin from 48.6% in 2010 to 51.1% in the LTM.”

Industry Trends

The other thing that really attracts me to this business are the long-term tailwinds that they continue to benefit from.

Cars on the road. The number of cars being driven in America has grown at ~1% a year for the last 30+ years. This is probably even higher in Mexico, where O’Reilly continues to invest.

The average age of vehicles in the United States is getting older. In 2012, the average age was 11.1 years and in 2022 it stood at 12.2 years. Initially I thought that cars lasting longer would maybe be a headwind since it meant they were better engineered, but I was wrong. Most manufacturer warranties end after 7 years, so that sends more cars through aftermarket shops like O’Reilly. Not to mention, the older a car gets, the more frequent the maintenance cycles.

Second industry trend I should call out is the market consolidation. O’Reilly and Autozone have been growing share in both the DIY and Pros markets for the last decade and now combined account for ~40% of the auto parts stores in the US. Advanced auto and the smaller mom-and-pop shops will continue to cede share to O’Reilly.

Capital Allocation Strategy

O’Reilly runs a consistent capital allocation strategy and it has done a phenomenal job of sticking with it. The first priority for the company is investing back into the business where it sees a need. This can be new technology, new software, new stores, new distribution centers, that kinda thing.

But O’Reilly also acquires competitors when the opportunity makes sense. And there are a couple reasons that they’re able to do this. For starters, this can allow them to add new locations in bulk at a fraction of what it might cost to do so one by one. They’re also typically able to get these done at pretty attractive multiples.

The average auto parts store in America makes around $1.5 million in sales a year, and most of the stores aren’t run nearly as efficiently so the margins are slimmer. When a store gets rebranded to O’Reilly’s it gets a nearly automatic lift to sales and profitability for a couple of reasons. 1) It instantly becomes a node in the distribution network to Pros, so that’s a business that didn’t exist prior. 2) People will search for O’Reilly specifically. 3) They then have shared resources and systems so it doesn’t cost as much to run the stores.

Historically, they’ve made about 1 acquisition every 2 or 3 years, and it’s usually to help expand into new areas. For example, they just acquired Groupe del Vasto which gave them 23 new stores in Canada, which is a market they previously did not serve at all. This can sometimes muddy the financials as it tends to drop the consolidated margins a little bit.

And then the last element of the capital allocation strategy is their buyback program. They are extremely consistent about buying back stock and have been able to cut their share count in half over the last decade. They dedicate pretty much 100% of their free cash flow to buybacks.

They also use a little bit of debt to fund various elements of their business. Their current Debt-to-EBITDA ratio is 1.95x, and they said on the last conference call that they target 2.5x. The average interest rate on the debt is a little over 4%.

Corporate History & Current Management Team

O’Reilly Auto Parts was originally founded in 1957 in Springfield, Missouri by Charles and Chub O’Reilly (father and son). They had together been running a different auto parts store before they decided to break out on their own. And initially, they were actually in the Pros business. They were distributing auto parts to people who worked on cars.

The concept was very successful early on but the expansion was gradual. Their 2nd store came in 1965 and it wasn’t until 1975 that they needed to acquire a distribution center and corporate office. They reached 100 stores by 1989 and in 1993 they went public. Then in 1998, O’Reilly had probably its most transformative moment when it acquired Hi/LO Auto Supply. Hi/LO had roughly the same amount of stores and gave O’Reilly an expansion into the Texas and Louisiana markets. It basically doubled the size of the business.

Since that point, it has basically been more of the same playbook. Consistent store expansions where it identifies a need for one and strategic acquisitions when the opportunity is there.

Today, they are on just their 4th CEO after nearly 70 years as a company and it’s Brad Beckham. Beckham joined O’Reilly as a store parts specialist in 1996 and worked his way up throughout the company. In general, I really like what I have heard from Beckham. Here are some quotes from him at the 2022 analyst day:

“At the heart of our culture Is promote from within. Somebody like me that didn't even go to college has been very fortunate to grow up with a company that promoted virtually 100% from within, especially in store operations…This isn't a business that somebody can just walk into. You have to have a good understanding of what make those shops tick, what really happens on the counter every day. Our business is a consulted visit. When you see our stores, we have several 1,000 SKUs that are out on the front floor, but the far majority of the parts are in the backroom so to speak behind that counter. And so even when you move on to the Next level leadership here, we have 13 divisions in the United States and every one of those division vice presidents ran an O'Reilly store. They started out in the stores, every single one of them.”

I didn’t spend too much time on the proxy statement, but I checked it just to make sure the compensation wasn’t crazy. And actually thought it was very reasonable. Like most, you’ve got your base salary, cash bonus, and long-term share based incentives. CEO got paid ~$5 million in total comp but all other executives were between $1M-$3M. And the targets were pretty reasonable.

5% comp sales growth

OI growth of 4%

ROIC of 72%

FCF growth of $2.1 billion. (This has the most variability depending on acquisitions, capex, etc.)

Competitive Advantages

There isn’t really one obvious competitive advantage like you see with a Visa or something.

It feels more like 100 little advantages that they’ve developed over 70 years of serving customers that allow them to be far more profitable than competitors. I’ll go through some of them:

Robust digital catalog - equips in-store personnel with the knowledge needed to serve customers)

Streamlined supply chain - Can deliver 152k SKUs to any of their stores same-day or overnight. Makes it easy for customers to get what they need.

Distribution Capabilities - Can go above and beyond for customers by delivering parts to them.

Name recognition from customers - Helps with a sales lift from Day 1.

National marketing - Can spend less on marketing on a per-store basis than smaller peers while still spending way more overall.

Shared backend systems - Accounting, HR, billing, invoices, etc. Not nearly as costly to install and maintain when spread across a massive store base.

Private label brands - Can offer products where they see a gap or can promote their own products which may have higher margins.

Bargaining power with suppliers - They are probably one of, if not the, largest customer for most of their suppliers, so they’re probably able to get bigger discounts on a per unit basis than peers.

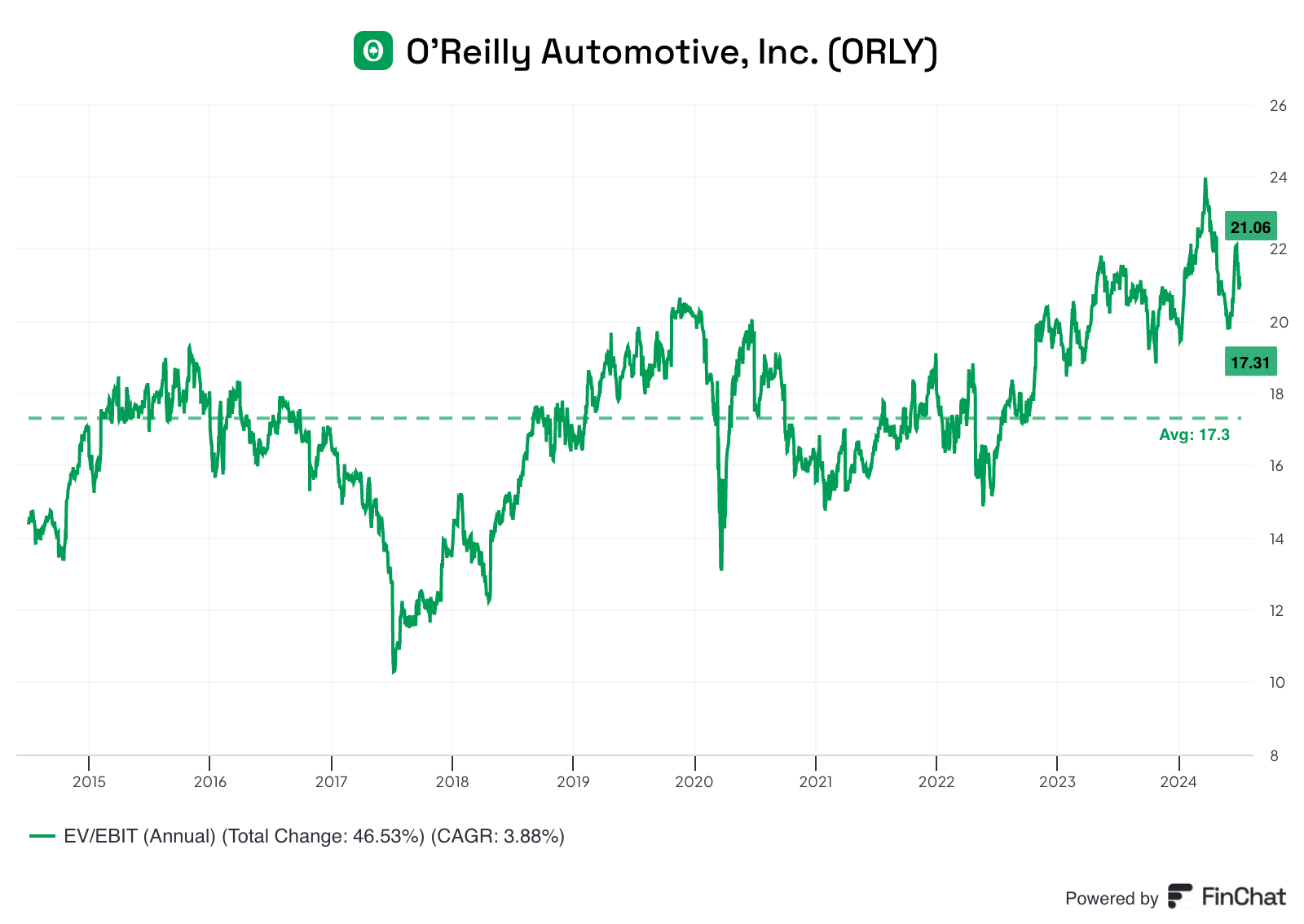

Valuation/Stock Upside

O’Reilly currently trades at an EV/EBIT of 21x, which is above its historical average.

I’ll try to keep the math simple on this one.

I think the tailwinds that have helped the business thus far will continue to do so for a while. I would assume 4%-5% comp store sales growth, then another 2%-3% from new stores each year. Additionally, I suspect margins will continue to expand the same way they have been. So all in all, probably 8% revenue growth per year and 10%-12% earnings growth. With the buyback, maybe 15% EPS growth. Maybe the multiple contracts a little bit (uncertain obviously), so I think there’s potential for 15% annual return.

Biggest risks

The biggest risk to me is the rise of electric vehicles. They don’t need to be serviced nearly as much as ICE vehicles. This is kind of the obvious long-term headwind. My guess is it will still take quite a while before ICE vehicles on the road start declining completely. It’s something to continuously monitor.

Chit Chat stocks is presented by:

Public.com just launched options trading, and they’re doing something no other brokerage has done before: sharing 50% of their options revenue directly with you.

That means instead of paying to place options trades, you get something back on every single trade.

-Earn $0.18 rebate per contract traded

-No commission fees

-No per-contract fees

Options are not suitable for all investors and carry significant risk. Option investors can rapidly lose the value of their investment in a short period of time and incur permanent loss by expiration date. Certain complex options strategies carry additional risk. There are additional costs associated with option strategies that call for multiple purchases and sales of options, such as spreads, straddles, among others, as compared with a single option trade.

Prior to buying or selling an option, investors must read and understand the “Characteristics and Risks of Standardized Options”, also known as the options disclosure document (ODD) which can be found at: www.theocc.com/company-information/documents-and-archives/options-disclosure-document

Supporting documentation for any claims will be furnished upon request.

If you are enrolled in our Options Order Flow Rebate Program, The exact rebate will depend on the specifics of each transaction and will be previewed for you prior to submitting each trade. This rebate will be deducted from your cost to place the trade and will be reflected on your trade confirmation. Order flow rebates are not available for non-options transactions. To learn more, see our Fee Schedule, Order Flow Rebate FAQ, and Order Flow Rebate Program Terms & Conditions.

Options can be risky and are not suitable for all investors. See the Characteristics and Risks of Standardized Options to learn more.

All investing involves the risk of loss, including loss of principal. Brokerage services for US-listed, registered securities, options and bonds in a self-directed account are offered by Open to the Public Investing, Inc., member FINRA & SIPC. See public.com/#disclosures-main for more information.