Why We Don't Own Airbnb Stock (Ticker: ABNB)

A disruptive compounder, but a steep valuation

Reminder: these are show notes that should be read in conjunction with the podcast. Do not expect these notes to be a polished research report.

YouTube

Spotify

Chit Chat Money is presented by:

Potentially you! Reach out to our email chitchatmoneypodcast@gmail.com if you are interested in sponsoring our newsletter, podcast, or both.

Show Notes and Charts

(Brett) How did Airbnb begin? What got them to where they are today?

There are a lot of corporate histories on Airbnb (and a few books) so I’m going to keep it succinct but then focus more on how they got to the position they are today so any listener has context for why the numbers look like they do.

In 2007, founders Brian Chesky and Joe Gebbia were looking for some extra money to pay for rent in San Francisco. So they decided to rent out their extra space during a weekend when there was a big conference in the area. They made a site called Airbedandbreakfast and found some people to rent out the space for the weekend as hotels were all booked and jacking up prices.

After the weekend, the two realized there was something to this idea, and contacted their engineer friend Nate (apologies Nate I am not going to be able to spell or pronounce your last name) who was a bit of a coding savant from Harvard.

Then, they actually puttered around in obscurity for a year or so, trying to launch a few times but failing to get any traction. They reached out a to a lot of investors and got no luck with fundraising.

Then, at the 2008 Democratic convention, they launched again but with a unique marketing strategy by selling Obama-style cereal on the street with a promo for Airbnb inside (it may or may not have been shortened to Airbnb by this time). Y Combinator took notice and put them in their accelerator program to improve the product.

Then, they got a $600k initial investment and the rest is history. They went on a blitz scale and by 2011 had 1 million nights booked on the platform. The company raised billions and grew to become one of the premier unicorns in the valley..

So to sum things up:

The three guys had a novel idea and then blitz-scaled it

The company had the classic “grow at all costs” Silicon Valley mindset that got them market share fast…but they were burning a lot of cash

Then, the pandemic hit.

(Ryan) What changed during the pandemic for Airbnb? How have they recovered since then?

If you listen to Brian Chesky at the recent Morgan Stanley Technology conference, he goes into the transition that they experienced in pretty good detail. But I’m going to repeat some of what he said here. Chesky kind of thinks about the changes as internal and external. Here’s what he had to say on the external or the overall market changes: “I think a lot of things have changed. But I think the biggest thing that’s changed is suddenly people have realized they can do their entire job from a laptop… there is an unmistakable trend that people are permanently more flexible.” He said this has really resulted in a shift towards longer-term stays. He goes on to say “I think travel has changed forever. Business travel still exists, but a blurring between business and leisure is probably where it’s all going.” I think we’re seeing that play out. But even if you’re a remote work skeptic, it’s pretty indisputable that the the changes to the travel market brought about by the pandemic are ultimately going to benefit AirBnB.

Now on the internal side, there were a number of big changes made at AirBnB. Prior to the pandemic, Chesky said that AirBnB had become very divisional. They had their homes division, experiences division, transportation division, had a China division, etc. and the decisions were being made at the division level. In addition they were spending about $1 billion a year on performance marketing. He even said he was getting pretty frustrated with what AirBnB had become. Here’s his exact quote: “Our product was looking less different than our competitors every single year. It was getting really hard to get work done. It was bureaucratic, it was political. Basically, we were suffering from big company syndrome.” So it sounds like the pandemic may have been the spark Chesky was actually really hoping for.

In fact, he even says “Then the pandemic occurred. We lose 80% of our business in 8 weeks. We have to rebuild the company from the ground up. And I thought this is a moment for us to build a different kind of company.” So in April of 2020, at the height of the pandemic when lots of people are calling for the demise of AirBnB, they were forced to make several changes. And the first thing they did was shut down all marketing. “What happens if you shut off all of your marketing? The answer was hardly anything. That’s when I realized performance marketing is a drug.” The second thing they did was shut down all of their various divisions and consolidate them into one. “We went back to a functional organization like a startup. We had a marketing department, a design department, and an engineering department and we centralized all decision-making.” And how has that ended up for the company?

Trailing 12-month revenue is expected to hit $9 billion when they report this upcoming quarter. That’s 90% higher than AirBnB’s pre-pandemic levels. However, the real change has come in profitability. EBIT margins (which I think is probably the best way to value the business) have gone from -10% pre-pandemic to 22% over the last 12-months. Now part of that has been driven by the demand vs. supply imbalance driving up ADR’s.

(Brett) How does the business model work?

For a company of its size, Airbnb’s business model today is incredibly simple and in my opinion quite elegant.

As a marketplace with two groups of people looking to make transactions (hosts as the sellers and guests as the buyers) Airbnb takes a cut of every dollar spent through its service. Famously, it has kept its host fee at just 3%, but the fees applied to guests is much higher in the 10% - 15% range.It is not a perfect way to calculate the blended take rate, but Airbnb reports revenue and gross booking value for every financial period. Gross booking value is the total dollars spent by guests in a certain time period but could apply to trips well in the future and not during that time period, which means they

With that being said, if we take 2022 revenue and divide it by 2022 gross booking value, we get a take rate of 13.2%. Generally, I think that is a good estimate. What investors need to know is they charge a small take rate to hosts and a larger one to the guests.

One thing to note is that Airbnb processes payments itself. Since this is the payments month I wanted to discuss this as Airbnb can relate to all the payments companies we have discussed throughout this month. Essentially, they have built their own payment processor without the need for an Adyen, checkout button, or anything like that. What’s incredible is they built this from scratch as a start-up in their early days and it now works seamlessly around the globe. The advantage of this is they are the merchant of record with payments and hold the customer funds before paying the hosts, which allows them to invest the cash into short-term treasuries.

This is what the payment process looks like at checkout today. It may seem simple but they have built the engine for processing payments in every country around the globe internally:

Cost of revenue: payment processing distributions (the credit card companies get their cut), cloud hosting fees (AWS), amortization of internally developed software, and some fraud costs. This was 17.8% of revenue in 2022 and should scale with the business.

Next expense, operations and support: One could argue this should be included in cost of revenue but hey maybe these contractors all get replaced by AI. As you might expect, these are the support lines for Airbnb, a vital part of the value chain that will also probably scale with the business. This was 12.4% of revenue in 2022.

That leaves around 70% of every revenue dollar left to plow into R&D, sales and marketing, and pay for overhead costs. This is a very attractive business model and gives Airbnb a ton of optionality to invest in new initiatives (which we will cover later). And, given the reversal in culture that occurred during the pandemic, the company has started to generate a very healthy profit margin. GAAP EBIT margin was over 20% in 2022 even with Fx headwinds, many regions still down from COVID-19 (especially at the start of the year), and 18% of revenue spent on product development.

Taking all this into consideration, I think we can model the business closing in on 25% profit margins sometime soon, but not much higher given management’s commentary on pushing for growth and continually improving the core product, which they feel has a long runway ahead of it.

We can also discuss the working capital advantage:

(Ryan) Why do we like the founder Brian Chesky and think the management team has a culture we would want to trust with our money?

Brian Chesky is very charismatic which I know can be misleading sometimes, but he seems to truly possess that same insatiable customer-focus that Bezos had. Here’s an example. On May 3rd, Brian Chesky tweeted “You told us what you don’t like about Airbnb. Here are the 50 things we’re doing about it…” and released a long thread with tons of videos explaining all the product changes the company has made in response to customer feedback. Here’s a list of the first 10 upgrades they made:

1. Total price display

2. New mini-pins on maps

3. Redesigned wishlists

4. Improved monthly search

5. Transparent checkout instructions

6. Pay over time

7. Faster maps

8. Persistent pins on maps

9. Smarter search autocomplete

10. Wishlist one-tap save

Then, he turns around the same day and tweets “What else can we improve about Airbnb? We will prioritize your top suggestions” and he instantly came up with a new list of changes that he said the company will try to make this summer.

And if you think about two of the big recent product rollouts – Categories and Aircover – they are very clearly addressing customer painpoints. Categories is more so inspiring people to find new ways to travel, but Aircover directly addresses one of the biggest concerns among potential new hosts. People are always worried about what could happen to their home, so AirBnB rolls out $3 million of protection against theft or property damage. So the execution just really seems to be there.

On the incentives side, I think the executive team is properly aligned. There are some hefty bonuses, but Chesky owns 31% of the voting power, Gebbia (chairman of the board) owns 27%, and Nathan Blecharczyk (current chief strategy officer) owns 20%. So combined, the 3 founders own 75% of the company and have a very clear incentive to drive long-term shareholder value.

(Brett) Why do we think Airbnb has a strong and growing competitive advantage?

The part of the episode where people might start disagreeing with us. If you have any pushback on our bullishness for Airbnb’s moat, we welcome any comments. Do not think it disrespectful to disagree with us about a stock, that is a part of the game and we will thank you if you stop us from making a mistake.

Why we think Airbnb has a strong competitive advantage

The core of Airbnb’s competitive advantage comes down to a network effect. This is the general definition of a network effect:

“the term network effect refers to any situation in which the value of a product, service, or platform depends on the number of buyers, sellers, or users who leverage it. Typically, the greater the number of buyers, sellers, or users, the greater the network effect—and the greater the value created by the offering”

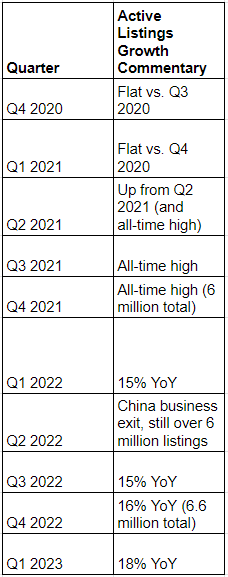

Airbnb has two sides to its marketplace: Hosts (i.e. lodging and experience listings) and guests. As the number of listings on Airbnb grows, the value proposition for guests looking for places to stay also grows, especially if listings are growing faster than the competition. In our mind, this is why the most important KPI for Airbnb is supply growth. Unfortunately, management is a bit opaque about supply on the marketplace, but they have given some good datapoints recently. Here is a chart compiling commentary since it went public:

Conversely, the more active guests searching for places to stay on Airbnb, the more valuable it is for the median host to put up a listing on Airbnb (as there is a higher chance of earning revenue).

What’s nice about this is that Airbnb is playing a non-zero sum game with its three stakeholders (shareholders, guests, hosts). If they get more supply on the platform and get more guests to spend money, the customer experience improves and Airbnb earns more in revenue since they just get a rake on all transactions.

Why we think Airbnb’s moat is widening

The moat (or lack thereof, if you disagree with us) can be talked about ad nasuem and put your head in a pretzel. I want to make it incredibly simple: Airbnb’s moat is growing if the supply on its platform is growing. That’s it. And looking at the last few quarters, the moat expansion is actually accelerating.

What’s special about Airbnb’s competitive advantage is that – unlike other marketplaces like Uber, dating apps, used goods services, etc. – Airbnb’s network effect applies globally. This makes it it much less vulnerable to disruption compared to a marketplace like Uber, in our opinion. Someone could go after Uber in a local city and given enough capital would maybe start stealing market share. But Airbnb is in 100k cities which its guests are all looking for as they search for travel destinations. If you want to disrupt Airbnb, you need to beat its entire supply around the globe (or maybe in a country/continent). This reminds me of Visa.

Where would we rank Airbnb’s moat of businesses we’ve covered/owned?

(Ryan) What do we think drives growth over the next three years and beyond?

There are a number of ways for AirBnB to create additional revenue drivers for its business (and I’ll talk about some of those in a sec) but ultimately, the number one way and the clear focus of management today, is continuing to drive growth in listings. Chesky recently said “Our brand is mainstream, AirBnB has been used 1.5 billion times. We’re now used all over the world. But hosting is a little more underground.” He continues “We had built a demand muscle, but we didn’t yet build a supply muscle.”

They’ve been promoting the hosting side more and more in their marketing and it seems to be working. At the end of last year, AirBnB had 6.6 million active listings and in the most recent quarter that figure grew by 18% YoY, which is the highest since their IPO.

But like I said earlier, there are a lot of other levers they can pull and one of those levers investors have been eager to see is sponsored listings. Perhaps this means hosts would give up some additional take-rate in exchange for preferred placement in searches, but Chesky has some interesting thoughts on this topic: “My CFO is from Amazon, and he used to use this Jeff Bezos quote ‘that you want to focus on the most perishable opportunities first’. And the great thing about sponsored listings is it’s not perishable.” In other words, it sounds like Chesky wants to defer this kind of monetization as long as they can since it’s such an easy lever to pull. He goes on to say “Monetization is great at scale. So you want to get as much scale as possible and we still feel like we’re in land grab mode.”

Another big driver of growth in the short-term could be the resurgence of travel across Asia-Pacific regions. In the most recent shareholder letter, AirBnB said “In Asia Pacific, Nights and Experiences Booked saw the most significant year-over-year growth as travel continues to recover in the region. This region has historically been reliant on cross-border travel. While still down compared to pre-pandemic periods, we have seen continued sequential recovery in the region, with 48% growth in Nights and Experiences Booked in Q1 2023 compared to a year ago.”

But there are a number of other ways to grow too. A loyalty or membership program, a credit-card program, greater hosting adoption from rooms/apartments. The possibilities are really pretty endless.

(Ryan) Why do we think the stock is too expensive at these prices?

I think it’s easy to say that AirBnB checks most of the boxes we look for in an investment. They have durable competitive advantages that should enable them to grow revenue at a double-digit rate for a long time while increasing their profitability. However, even while checking those boxes, it’s hard to see how this would provide incredible returns given the current valuation.

At the current share price of $128, AirBnB has a market cap of $82 billion. They have about $8.6 billion in net cash so that comes out to an enterprise value of ~$73 billion. Over the last 12 months, AirBnB generated ~$2 billion in EBIT. So they trade at an EV/EBIT multiple of 36.5x.

If you assume that AirBnB grows its revenue by 15% this year then 10% the two years after, they’d generate $12 billion in revenue for the year 2025. Now if you believe that margins can expand gradually to around 24%, that would mean AirBnB would be generating roughly $3 billion in operating income that year. Let’s assume investors value them at 30x Price to EBIT (well above the average S&P 500 multiple), that would imply a $90 billion market cap, or 10% higher than the current price.

In other words if AirBnB grows revenues at a double-digit rate and expands operating margins over the next three years, you still might only get a low to mid single digit annual return. We think there are better opportunities available today.

Now if AirBnB begins to get into the $80 range, those same assumptions would result in returns above what we hope to achieve (15%).

(Both) What risks are we watching for the business going forward?

(Brett)

Short-term: A travel slowdown after the post-pandemic bonanza along with some increase in supply (at least in the U.S.) that leads to a decline in daily rates. Airbnb has said they are investing to slow down the growth of daily rates by getting some more affordable listings, and there could be a slowdown if we hit a recession ever due to the central banks wanting to stop inflation. Counterintuitively, since we don’t own the stock today, this is something that I want to happen and tanks the stock so we can buy shares later.

Long-term: I worry that even though I love the product and think the moat is strong, there are a lot of other travel/hosting platforms out there that could succeed (VRBO, Booking, etc.) and this commodification of the service may lead to the need to spend on performance marketing. I have confidence this is not the case, but this is why I will be tracking the total number of listings closely as it is the key way for the business to expand its moat.

(Ryan)

One big risk that keeps popping into mind for me is price instability in the average daily rates. Because this part of the revenue equation really benefits profitability, I worry that a decline in the ADR could really hurt margins. And to some extent this is kind of out of AirBnB’s control.

I’m not too worried about the competitive environment, at least in the US. They have become a verb and businesses are being built on top of the AirBnB platform. It’s truly changing the way people can live and travel.

Sources and Further Reading

Airbnb’s payments advantage: https://www.pymnts.com/platform-payments/2017/payment-processing-platforms-hospitality/

Dallas bans short-term rentals: https://www.sacbee.com/detour/article276582741.html