Why We Own Alphabet/Google (Ticker: GOOG)

An exploration into the potential futures for the technology giant

Reminder: these are show notes that should be read in conjunction with the podcast. Do not expect these notes to be a polished research report.

Upcoming schedule: Alphabet/Google and then a month covering financial stocks

As always, listen to the episode on Spotify, YouTube, or wherever you are subscribed to the show.

Charts

Data powered by Stratosphere.io

Chit Chat Money is presented by:

Stratosphere.io, a powerful web-based research terminal for fundamental investors.

Stratosphere.io has made it easy for us to get the financial data we need with beautiful out-of-the-box graphs that help us do research for Chit Chat Money.

🎉Stratosphere.io just launched their brand new platform and you can give it a try completely for free.

It gives us the ability to:

Quickly navigate through the company’s financials on their beautiful interface

Go back up to 35 years on 40,000 stocks globally

Compare and contrast different businesses and their KPIs

Easily track insider transactions and news updates for any stock we follow

Get started researching on the Stratosphere.io platform today, for free, or use code “CCM” for 15% off any paid plan.

Show Notes

(Brett) What is Alphabet?

Alphabet is an internet giant with many subsidiaries:

Google: Search + all the other properties like Maps and Gmail

YouTube: The largest DIY video service in the world

Android: One of the two largest operating systems for smartphones

Google Cloud: One of the three big cloud infrastructure providers. Customers include PayPal, Spotify, Home Depot, and others

Waymo: Self-driving car start-up

Verily: Biosciences start-up

Fitbit + Nest hardware systems

DeepMind: The world’s premier AI research institution. For example, they were the ones that solved a huge protein folding problem for the biosciences market

Alphabet is not run by its founders, Larry Page and Sergey Brin. It is run by Sundar Pichai, a CEO since 2019 and who has been with the company since 2004. The CFO is Ruth Porat, who joined in 2015.

(Ryan) Give any history/important context for the business:

In 1997, Larry Page and Sergey Brin, who were both in the process of getting computer science PhDs at Stanford developed a search engine (I think as a research project) and called it Backrub. It wasn’t the first web search engine, but it did have a slightly different architecture. At the time, big search engines like Yahoo wanted to keep people on their own sites as long as they could because they sold display ads and that’s how they made money. However, Google (or Backrub at the time) came along with a different way of determining page relevance. Google would rank pages based on the number of times it was referenced by another page. This led to better search results than other sites and they’d eventually roll out cost-per-click text ads which we still see today.

Needless to say, this found extraordinary adoption. Let me read off some of the numbers from Google’s S-1 that they filed just before going public in 2004.

In 1999, Google reported $220,000 in revenue.

In 2000: $19 million

In 2001: $86 million

In 2002: $348 million (53% operating margin)

In 2003: $962 million (36% operating margin)

After raising $2 billion during its IPO, Google made a series of acquisitions that have now shaped the company. In 2005, Google acquired a floundering mobile phone business called Android for $50 million. In 2006, they acquired YouTube for $1.65 billion in an all-stock deal. And in 2007, in an all-cash deal, Google paid $3.1 billion for a digital advertising company known as DoubleClick.

Those acquisitions have all largely helped accelerate Google’s top-line growth while simultaneously deepening its competitive advantages. In 2015, the company announced its structural reorganization and changed its name to Alphabet. At this time Sundar Pichai became the CEO of Google, while Larry Page and Sergey Brin became the top guys at the parent company. They remained there until 2019 when they finally stepped down. Today they both still remain on the board of directors and combined own 51% of the voting power.

(Brett) Alphabet by segment:

Alphabet has three different segments with some subsegments within them that I have divided out into categories I think make sense from an investing perspective:

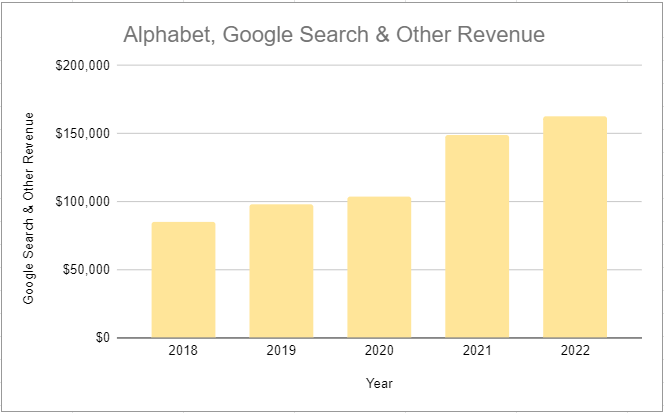

Google Search/Other advertising. This includes advertising on search, Maps, Gmail, and Google Play (56% of revenue last quarter)

YouTube advertising. Self-explanatory (10.5% of revenue last quarter)

Google Network advertising. This is display advertisements on websites through adsense and admob (11.1% of revenue last quarter)

Google Other. This includes non-advertising on Google Play, non-advertising YouTube services, Hardware devices, and “other” (11.1% of revenue last quarter)

Google Cloud. Infrastructure services and Google Workspace subscriptions (Google Drive), and enterprise services (9.6% of revenue last quarter)

Other Bets. Internet services, healthcare services, and autonomous vehicles (0.3% of revenue last quarter)

So the most important category by far is advertising on Google Search/Maps, with the next four categories sharing around equal weight at 10% of revenue each. Further on in this episode, we will go through the long-term potential of the YouTube and cloud businesses.

(Ryan) Who are Google’s competitors and what advantages does Google have over them? Why has Search retained an 85% - 90% market share globally and why do we think that can continue?

It’s no secret that Google has pretty much a monopoly on the search market. Estimates have its PC market share at just over 80% and its mobile share at ~90%. Keep in mind, Google not only dominates mobile search through its Android dominance, but it pays to power Apple’s safari searches. But there are still a couple of competitors. Bing, which is owned by Microsoft, touts about 5.5% share and Yahoo! Which is owned by Apollo Global has about 2.7% market share.

As I mentioned earlier, the pagerank algorithm was an early differentiator for Google’s search results, but that alone is replicable. So it begs the question, why has Google maintained its dominance for 20+ years? I found this quote from Timo Buss, the portfolio manager at Covesto Asset Management to be a near-perfect answer: “For ranking purposes, the company has stopped relying solely on backlinks and today takes over 200 different ranking factors into account. Building on its almost 4 billion users, Search generates the largest data set on global search and click behavior, which serves to continuously fine-tune the quality of its service. This feedback loop is an important economic moat, as competitors may copy Google’s ranking methods but hardly the aggregated usage data.”

This advantage has made the search results that Google generates nearly impossible to compete with. I think Microsoft’s recent search ambitions are a good example of how solid this moat is. In 2015, Microsoft launched its own search browser called Microsoft Edge which was intended to compete with Google Chrome. However, despite owning the dominant operating system, in 2020 Microsoft pivoted from using its own search framework to instead being built on Google’s Chrome’s open source platform, Chromium. Additionally, Microsoft’s recent layoffs are rumored to be focused around the Edge division.

(Brett) What are some “Moat Tests” that Google has passed?

This will be around Google Search’s heavily tested moat as well as how all its other businesses strengthen that moat today.

As the largest single profit pool in business history so far, Google Search has seen numerous competitors over the past 25 years. However, now it has very few true competitors, with Microsoft Bing as the only one who is deliberately trying to gain market share and therefore advertising revenue (Bing market share has gone from around 5% to 10% in the last decade on desktop).

In the early 2000s, Google was mainly a desktop/laptop search business. It had major threats from browsers like Internet Explorer (Microsoft) and incumbents like Yahoo as it was not yet a platform business but merely a great product. In order to fend off these incumbents and tighten its competitive advantage, it layered on new products for customers, almost always for free. These include Google Chrome (2008), Gmail (2004), Google News (2002), Maps (2005) and others. Yes, Google Search was itself a good product compared to the lackluster search engines of the 1990s, but by the 2000’s it was pretty easy to see how a larger technology company could copy them (Microsoft did). These other products, especially Chrome and Maps, enabled Google to pass a major moat test in the 2000s.

In the early 2010s, Google needed to make sure it maintained its search dominance as the smartphone revolution took hold. There were threats that any of the platform owners like Apple, Samsung, etc. could launch their own browser or search engine, kicking Google to the curb as a default search engine for browsers. One moat test the company didn’t care about or feared it wouldn’t pass was with Apple, where it has secured a license for Google Search on all Apple products. This license is now running at an estimated $20 billion a year.

However, outside of Apple Google made a masterstroke in acquiring Android and building it into the second big player in the smartphone market, making it free (most of the time) for hardware providers to use it as their operating system. All they had to do in return was pre-install Google’s core applications like Chrome, YouTube, Google Play, and Maps. This enabled manufacturers to sell phones for cheap around the world, which is (among other reasons) why Android has 70% market share for smartphones today. To further increase its moat in mobile, the company has started to manufacture its own smartphones (the Google Pixel), although it only has a low single-digit % of the market right now.

So Google passed its desktop and mobile moat tests. It also easily passed the “voice technology” moat test, which ended up being a lot of bark and no bite. The Apple license remain a weak link, which we will be watching in the years to come. If Apple decides to build its own search engine and end its relationship with Google, Alphabet will probably see a bump in earnings in the short term but could start to lose significant market share over the long term if Apple has its own search engine on the Safari browser for its devices. However, the holistic offerings from Maps, G Suite, and the YouTube integration should give Alphabet strong defenses if Apple tries to launch its own search engine.

But what about right now? Google is facing a potential threat from Microsoft Bing as it has revived Internet Explorer and is poised to launch the new AI chatbot ChatGPT3 for its user base. Just look at what happens when you search “Google Chrome” on the Internet Explorer homepage:

We will be watching these developments closely but feel confident in Google’s resiliency with all the points Ryan outlined in the above section.

(Ryan) So we believe that the Search business is durable, but fairly low growth. There are two segments we believe have fantastic long-term growth prospects. Let’s explain each. First, YouTube:

Everyone knows YouTube. It’s the largest video-sharing platform globally and is estimated to have roughly 2.5 billion active users. Though estimates vary, most sites assume the average user spends about half an hour to an hour on the platform every day. In fact, behind Google itself, Youtube actually has the second highest amount of search queries among all other platforms.

The core product allows anybody to upload and share videos with the world. Once accounts pass certain subscriber and hours watched thresholds, they then become eligible to monetize their content through Youtube ads. The creators collect 55% of every ad dollar and YouTube captures the remaining 45%. It has those wonderful user-generated content and network effect characteristics that we love. In total, Youtube reported $29 billion in advertising revenue this year.

However, Youtube has also expanded the platform. In 2014, the company first launched Music Key, which would eventually become YouTube Red and then finally, in 2018, they rebranded to YouTube Premium. With YouTube Premium, users pay $12 a month and get unlimited ad-free and downloadable videos, as well as a YouTube music subscription. Last quarter Sundar Pichai mentioned that they had surpassed 80 million subscribers to the service. Although that also includes trials, if we just do the basic math (80 million subs * $12/month * 12 months), YouTube Premium is bringing in just under $12 billion a year, which is up more than 60% from last Spring.

Another wonderful thing about this is that as more consumers convert to YouTube Premium, the available advertising inventory shrinks to a smaller amount of users. This means they can boost the ad load (CPMs for advertisers) on the remaining users, further incentivizing them to switch to Premium.

But perhaps the most exciting part about YouTube in my opinion, is the growth in streaming TV. In 2017, YouTube launched a live TV streaming platform called YouTube TV, which today costs about $64 per month. Some estimates have the service at a little over 5 million subs, but it’s difficult to tell since they don’t give out the number regularly. This has been a major success for them and paired with the core YouTube CTV app, YouTube claims more streaming time than any other connected TV service according to Nielsen.

This gives them a perfect introduction into the booming CTV ad market. For reference, right now, streaming accounts for about 40% of all TV viewing in the United States. However, it claims less than 10% of TV advertising. About $66 billion is currently spent on Linear TV ads in the US right now. I’d suspect the lion’s share (eventually all) of that transitions to streaming over time.

Primetime channels: “to combat the growing complication of subscribing to multiple streaming services to find the shows and movies you want to see, YouTube has devised a new feature called Primetime Channels. Primetime Channels allow you to view 30+ streaming services all from the YouTube app”

(Brett) Second, Google Cloud:

The cloud business is one that we have the least knowledge about but also possibly has the highest probability to 10x revenue over the next 10 - 15 years.

Google Cloud is a competitor to AWS, Azure, and other cloud infrastructure providers, while also powering Alphabet’s internet services like search, YouTube, and its AI tools. Last quarter, Google Cloud hit $7.3 billion in revenue for a run rate of $29.2 billion. That is up from a run rate of just $6.85 billion in Q4 of 2018, or more than 4x the revenue base in less than five years.

While it looks like late 2022 and early 2023 will be a slower period for cloud growth given what all the major CEOs have said on the recent earnings calls, we still believe there is an easy path for the industry to grow by 10% - 15% a year on average this decade as almost all of IT around the globe adopts the cloud due to its flexibility and cost savings as the big 3 achieve further economies of scale.

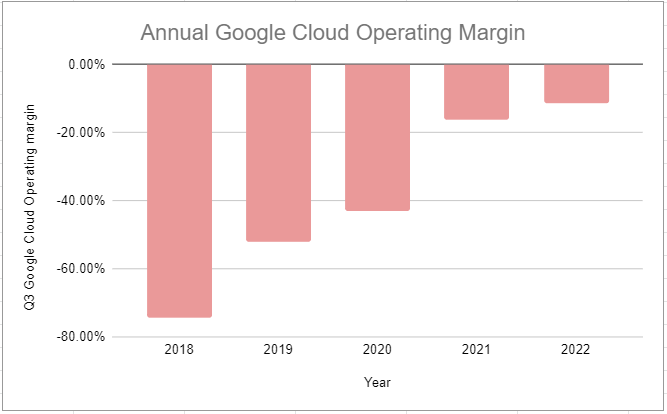

If Google Cloud retains a 10% market share, we think it is likely the segment eventually hits $100 billion in annual revenue (how soon, we have no idea). On 20% operating margins that is $20 billion in annual profits for a business with extremely high switching costs for its customers.

It is also important to note that today Google Cloud operates at a loss (7% operating loss last quarter). This has been a headwind to Alphabet’s consolidated earnings but will start to become margin accretive in the next few years. Of course, we have no clue what Google Cloud’s exact operating margins will be, but with AWS hovering in the 25% - 20% range we think at least 20% for Google Cloud is reasonable.

(Ryan) What does the valuation look like today? What assumptions lead us to believe that this deserves to be in the portfolio?

As of today, Alphabet has a market cap of $1.26 trillion (Class A: $105.33, Class C: $105.7). They’ve got $114 billion in cash and $30B in non-marketable securities, some of which are public equities. I included half of that. So $130B in cash and then they’ve got just $15 billion in long-term debt. So $1.26T market cap minus $115 billion in net cash, give it an EV of $1.14T.

In the last 12 months, they generated $60 billion in free cash flow. So at today’s price, it trades at an EV/FCF of 19x. Over the last 5 years, they’ve reduced the share count by about 1% annually, but they’ve ramped that up as of late so I’d expect that to accelerate.

Truth is, it’s a little difficult to make growth assumptions for Alphabet because of all the different moving parts, so I’m going to make it really simple. Here are my 5-year assumptions:

Services: With the steady growth of search and the upside of YouTube, I think revenue can grow from here by 10% annually. I’m also assuming steady-state operating margins are at 38% (that’s what they reached last year). Services would generate more than $150 billion in annual operating income.

Cloud: If we assume Google Cloud revenue grows at 15% annually and reaches 15% operating margins, it’d be generating just under $8 billion in annual operating income.

Other Bets: Pretty much impossible to predict, so I’m just going to say assume it burns $7 billion a year in operating income for each of the next 5 years.

If those assumptions are correct and they continue converting 80% of operating income into free cash flow and using that cash to buy back shares, we’d be looking at $125B in FCF or $12 in FCF/share. Applying a FCF multiple of 17x, you get a $204 share price or a 14% CAGR.

(Both) Pre-mortem: Why could we be wrong about Alphabet? What are we looking for as reasons to sell?

Ryan: The primary reason I think our assumptions could be wrong is just around margins or lack of cost control. Obviously, a deeper recession could hurt advertising budgets a bit more, but with the moat around search and the strength across YouTube right now, I’d be very surprised if Alphabet’s services revenue didn’t grow at a healthy rate over the next 5 years.

As far as costs go, I think Ruth Porat said something that was important on the most recent conference call. Even though the entire conference call and discussion around reducing costs were incredibly vague, she said “when we talk about being focused on delivering sustainable financial value, that obviously means that expense growth cannot be growing ahead of revenue growth.” If they execute that, I don’t see why they wouldn’t be able to achieve the profit assumptions I laid out.

Brett: There are a few things I am looking for as a reason to sell Alphabet. One is our thesis is incorrect on the outsized growth potential at YouTube and Google Cloud (this is a 2 - 3 year time horizon). Second, the company is unable to bring in costs for its research projects and employee headcount. Management said this will be addressed in 2023 and 2024 but it is still TBD. Third, is continued market share losses to Bing and/or the outside threats like TikTok/Instagram taking up more advertising market share (there is also the risk Apple decides to “decouple”).

I have strong confidence Alphabet meets our three criteria (durability, cheap valuation, and trustworthy management) but will be watching to see if either of these erode over the next three to five years. I do not put too much weight on what the numbers look like in 2023 from a profitability standpoint but will be looking for margins to get back to normal in Q3 and Q4 unless something materially changes.

Sources and Further Reading

Covesto Patient Capital Annual Letter: https://static1.squarespace.com/static/5d8b3d89ba59d07f93b338d0/t/63c6b28ceda958605e2be9eb/1673966221740/Investor+Letter+2022+ENG.pdf

Market share for mobile operating systems: https://www.statista.com/statistics/272698/global-market-share-held-by-mobile-operating-systems-since-2009/#:~:text=Android%20maintained%20its%20position%20as,the%20mobile%20operating%20system%20market.

Alphabet product history: https://www.verdict.co.uk/20-years-of-google-20-products-that-shaped-the-company/

Search engine market share: https://www.statista.com/statistics/216573/worldwide-market-share-of-search-engines/

Q4 2022 Results: https://abc.xyz/investor/static/pdf/2022Q4_alphabet_earnings_release.pdf?cache=9de1a6b