Why We Own Consorcio Ara (Ticker: ARA.MX)

Come explore this dirt cheap Mexican homebuilder with us

Reminder: these are show notes that should be read in conjunction with the podcast. Do not expect these notes to be a polished research report.

Today, we released our monthly Arch Capital podcast episode. On this month’s show, we go through our thesis on Consorcio Ara, a homebuilder in Mexico that generates consistent cash flow. Below are our show notes that outline our thesis for owning the stock today.

As always, listen to the episode on Spotify, Apple Podcasts, or wherever you are subscribed to the show.

Show Notes and Charts

What is Consorcio ARA?

Consorcio Ara is a homebuilder in Mexico. It has a diversified business that focuses on both affordable, middle-income, and higher-income homes, apartment buildings, and other dwellings across different Mexican states. Its largest operations are in Mexico City and the state with Cancun in it.

Consorcio Ara runs a fairly traditional homebuilding model. It invests in new properties by purchasing land that it will eventually build on. Currently, it has a sizable land bank of 30.7 million square meters, which it estimates is enough to build over 120k homes. For reference, in 2021 the company sold 6,464 homes. If the company keeps up its current home-selling pace, it could build homes for over 18 years without acquiring any more land. Of course, it is unlikely management will stop buying land (it purchased more last quarter), but it is an interesting exercise to go through nonetheless.

2.1 million square meters of Consorcio Ara’s land bank is set aside for commercial activities. The company owns a few retail malls across Mexico, which generate consistent revenue. However, it is only a small part of the business today and is not important to the overall thesis.

One thing that makes Consorcio Ara unique is that it owns its own concrete company. The commodity is a big material cost for its homes. This vertical integration helps Consorcio Ara insulate itself from commodity price increases compared to the competition in Mexico.

Important notes that will give context for our discussion:

Consorcio Ara’s current market cap is a tad over 4 billion Pesos

It has net debt of negative 952 million pesos, putting its enterprise value slightly over 3 billion Pesos

At the end of Q3, it had 15.3 billion Pesos of inventories. This is split up into 4.2 billion Pesos of land currently under development and 11.1 billion Pesos of Works in Progress (WIP)

At the end of Q3, it had a book value of 14.3 billion Pesos. At the current market cap, that gives the stock a price-to-book value (P/B) of 0.28

In 2021, it generated 691 million Pesos of Operating Income, 962 million Pesos of EBITDA, and 872 million Pesos of free cash flow to the firm. These are the metrics Consorcio Ara focuses on and what we do as well

Give some history and important context for the investment:

Consorcio ARA was founded in 1977 by two brothers, German Ahumada Russek and Luis Felipe Ahumada Russek. There’s limited information on the two brothers, but they’re still at the helm and running the company today.

As for the Mexican housing market, since about 2000, US private equity firms began investing quite heavily in homebuilding operations in Mexico (Sam Zell being the most popular example). This led to a significant homebuilding boom, but only to be cut short around 2014. Led primarily by Homex’s bankruptcy, the collapse of the Mexican housing market created a large oversupply of homes. In addition, the Mexican government ended a homebuying subsidy program that curtailed demand. These two factors combined to cut Mexican housing production in half since 2015.

However, throughout these last two decades, while most companies were building at will, the Russek brothers ran the business a little more conservatively. In fact, Consorcio ARA has generated cash each of the last 8 years, and soon to be nine. And to insulate themselves from any major cost increases, they’ve also internalized their concrete production (now own 13 concrete production plants). This has amounted to a remarkable balance sheet improvement. Since Q3 2017, Consorcio ARA has gone from ~$1.5 million in net debt to $48 million in net cash.

Now, they’re in a great position financially to benefit from the demographic tailwind facing Mexico today.

Why do we like the demographic tailwind for the Mexican housing market? How will Consorcio Ara benefit?

Demographics are important for our thesis in Consorcio Ara. Without anyone to buy homes, what good is a 30 million square meter land bank?

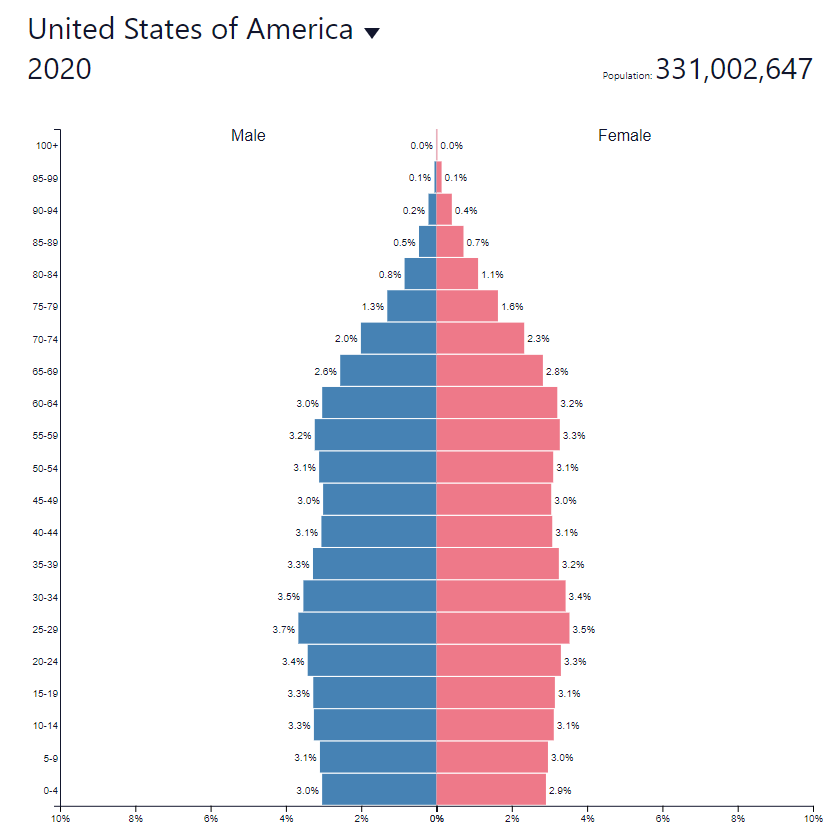

Luckily, Mexico has fantastic demographics that should sustain homebuilding demand for at least this decade. Half of the population is under 29, with a demographic pyramid that should see many people age into their homebuying years over the next two decades. To illustrate this point, let’s compare the Mexican demographic pyramid to the United States:

On top of a demographic tailwind, there is estimated to be a huge housing shortage across Mexico. According to S&P Global, this shortage could be as high as 9.4 million housing units that will only grow as these young people age into their homebuying years. With only 157k units built across the country in 2020, the country will likely need to double or even triple its annual output of homes to fulfill this demand. If not, prices will likely rise with an increasing supply shortage. Either way, Consorcio Ara should benefit from its existing land bank, experienced relationships, and vertically integrated model.

We also believe there is upside with the West (especially the United States) decoupling from China and reshoring manufacturing in North America. Mexico should be able to absorb a lot of this manufacturing capacity, theoretically boosting the economy and the ability for Mexican citizens to buy homes. While not a core part of our thesis, we think there is a high enough chance of this happening to warrant consideration from investors.

Taking all these factors into consideration, we have no problem forecasting consistent demand for Consorcio Ara’s homes over the next decade, even if it greatly increases its annual unit volumes.

What gives us confidence in Consorcio Ara’s management? Why do we trust them with our money?

First off, as I mentioned before, during the housing mania that occurred a decade ago, the Russek brothers maintained operating discipline and survived the collapse. In fact, they not only survived but actually generated profits every year despite diminishing homebuyer demand. In other words, the Russek brothers know how to operate a homebuilding business and they’ve got the scars to prove it.

Additionally, despite being quite financially conservative, management is still capitalizing on the stock’s current cheap valuation. In June, Consorcio ARA bought back 1.6% of their outstanding shares and at the same time, one of the founders of the business bought 2.4% of the company. This comes in addition to “canceling” 1.72% of their outstanding stock in April. And on top of all that, they raised their annual dividend by 45% versus a year ago to P$290 million, which annualized equates to a ~7% yield.

As for ownership, the company doesn’t file a proxy, but I’ve seen estimates stating that German Russek owns ~28% of the company today. So put simply, we trust management because they 1) Have a 40+ year track record of steadily growing a business, 2) They focus on cash generation and don’t take big risks, and 3) They’ve demonstrated their alignment with shareholders through their recent capital allocation decisions.

What are the main downsides of the homebuilder business model? Why do we think Consorcio Ara will do well in spite of this?

The two downsides of the home building industry are tough working capital dynamics and impacts from macroeconomic developments outside of company control. Let’s talk about both and why we are comfortable with Consorcio Ara’s position and ability to generate earnings.

First, the working capital dynamics. Homebuilders generally have a tough time converting their operating income into cash flow because a lot of those earnings get “stuck” in works in progress and inventory. Consorcio Ara definitely has this problem, but in spite of this headwind has generated healthy free cash flow for many years coming out of the housing crisis of 2008.

For example, on the homepage of its website it states that “for the eighth year in a row, we generated positive free cash flow to the firm in 2021, this time totaling P$871.9 million.” We appreciate this focus on cash flow and think it helps us get aligned as shareholders with the company.

Macroeconomic developments include rising interest rates that can hurt home affordability. When interest rates rise, mortgage rates tend to rise as well, which can make it harder for people to buy homes. This is happening in Mexico at the moment as the country tries to fight inflation. The central bank has increased its interest rate from around 4% in the 2020 trough (it also tried to stimulate the economy through interest rate drops) to just over 9% today. While this is a concern, Consorcio Ara generated cash from the 2016 - 2019 period as interest rates rose, and is generating cash in 2022 with them rising again.

With the demographic tailwind and housing shortage, we think Consorcio Ara will do fine even if the macroeconomic picture worsens across Mexico. Could margins deteriorate? Sure. Could the business go into a rough patch if we have a global depression? Definitely. But there are not many stocks that you can hide in if the global economy collapses. We think a stock trading at 0.28x book value is a good bet vs. other parts of the market if this occurs, though.

What does the valuation look like today? How is management taking advantage of it? Why do we think it is cheap?

As of their most recent quarter, Consorcio ARA had 1.26 billion shares outstanding. At its current price of $3.30, that’s a market cap of P$4.16 billion (or $214 million).

On their balance sheet, they have P$4.23 billion ($213 million USD) in land bank value carried at cost. If we include half of the land bank value and the net cash they have on hand ($48M USD) into the enterprise value calculation, Consorcio ARA’s enterprise value sits at approximately $1.1 billion pesos (or $55 million USD).

Over the last 12 months, they’ve earned $32 million in Operating Income and $17 million in free cash flow (working on several big apartments that are hurting working capital). That’s an enterprise value to (depressed) free cash flow multiple of 3X.

In addition, they pay out a dividend currently yielding 7.2% and pledged to buy back $100 million pesos worth of stock (~2.4% of their shares). Between these two, shareholders are getting ~10% of Consorcio ARA’s market cap paid back in cash each year. That provides a pretty high floor for investors here.

Why is the stock down significantly since before the GFC? Why do we think that will change?

This is a more subjective question, but we think there are a few reasons Consorcio Ara’s stock is down significantly from the GFC, which we will discuss:

The company has struggled (or chosen not) to grow unit volumes and revenue since the GFC. This has likely given investors little confidence that management is focused on growing its topline.

It is a dead stock. With the stock down so much and it being a small-cap company, we believe many investors don’t know the opportunity exists. And if they do, they are fed up with what the stock has done over the last 10 years

The company has used the majority of the free cash flow it has generated over the last five years to pay down debt (reversing from a positive to a negative net debt position) and payout dividends

We are not banking on Consorcio Ara to grow its revenue and unit volumes in order for this to be a good investment. All we need is for the company to generate in cash what it has done for the prior few years and the entire enterprise value will have been generated in cash within three to five years. If this happens, with a negative net debt position, the company will be able to return tons of cash to shareholders through dividends and repurchases. This may not drive the stock price higher, however, we still think we can generate acceptable returns due to the company’s dividend payouts.

The big risk with these assumptions is that Consorcio Ara will just keep accumulating pesos on its balance sheet. While we accept this risk, management has recently discussed how it is more comfortable with its financial position compared to five years ago and that it is ready to return capital to shareholders. For example, last conference call they said they plan to buy back approximately 100 million pesos in stock next year, or around 2.5% of its market cap.

What are the main risks we are watching? How will we know if the thesis is wrong?

Ultimately, over the next 3-5 years, if Consorcio ARA generates anywhere near as much as it did in the last 5, this investment will make money. So the big risk that needs to be monitored is homebuyer demand as that’ll primarily determine whether or not the company generates cash.

There’s no perfect way to track demand, but we think the best way to track overall demand is to follow the number of homes sold in Mexico each year and the changes in Mexican interest rates. The Mexican lending rate is currently 9.23% vs. 5.5% at the start of this year (Mortgage rates specifically are 10%+).

There’s also some currency risk here as well. They earn in pesos and we will eventually have to convert them to USD, so if the peso depreciates vs the dollar, our real return could be diminished. Fortunately, they pay out that 7% dividend yield so it alleviates the currency risk somewhat as you can convert each time it’s paid out.

The last risk is that the land value isn’t worth what it’s quoted on the balance sheet. It’s carried at cost but some of this land might be worth less than they bought it for.

Is Mexico a market that investors should avoid? Thoughts on foreign exchange risks?

We believe that the Mexican market is riskier for U.S. investors for a variety of reasons. These include:

Not having “boots on the ground” to study the companies (including the language barrier)

Having less confidence in the political environment to act in the best interest of corporations

The currency could get devalued vs. the U.S. dollar (which is what matters to us)

Because of this, we need to see a huge discount to value and a fantastic risk/reward opportunity for investors if we are going to buy a Mexican stock over an American one. We do not entirely avoid international stocks, but just hold them to a higher return standard to compensate for this risk. With Consorcio Ara, when we look at the stock today, we think there is a fantastic opportunity for shareholders over the next three to five years.

However, if another opportunity comes along with a United States business, it is possible we would replace Consorcio Ara in the fund even if we thought it had higher forward return potential due to the risks of investing outside our home market.

Sources and Further Reading

S&P Global 2020 Report on Mexican Housing: https://www.spglobal.com/ratings/en/research/articles/210217-for-mexico-s-housing-sector-recovery-remains-elusive-11828988

Consorcio Ara Investors Relations:

Consorcio Ara: Why I’m Not a Fan of Mexican Homebuilders (bear case):

Interested in the Arch Capital fund? Check out our website:

https://www.archcapitalfund.com/

Any updated thoughts on ARA? I recently started a position after following the company over the last 2/3 years.