Why We Own Spotify (Ticker: SPOT)

Our inaugural Arch Capital Update episode

*This is our first Arch Capital Update episode, available only for CCM+ subscribers. We plan on releasing these episodes once a month, covering specific stocks in our portfolio, why we sold a security, and/or other aspects of the limited partnership. Enjoy the episode!

Research folder with show notes, charts, and valuation: https://drive.google.com/drive/u/0/folders/1tiYlIlil-D9yDzyrf8yxFVkwvUn-SAfC

As always, listen to the episode on Spotify, Apple Podcasts, or wherever you are subscribed to the show.

Show Notes and Charts

(Ryan) What does Spotify do?

Spotify is the largest audio platform globally. Through its freemium model, Spotify allows virtually anyone around the globe to access an extensive catalog of music, podcasts, and soon, audiobooks. Subscription prices range depending on users’ geography and subscription type. I.e. a family plan in an emerging market is cheaper on a per-user basis, than an individual plan in the US.

With Spotify, users get curated playlists and recommendations based on their listening habits that allow them to easily discover new content. This not only helps drive retention but also higher engagement among users. According to Daniel Ek, Spotify has “more than 2 or even 3x the amount of engagement per user than some of our competitors do.”

(Brett) What does the unit economics look like today? How could that change in the future?

Spotify breaks out its business into two segments: premium music (subscriptions) and advertising. We will look at both for this episode and why gross margins are at where they are today.

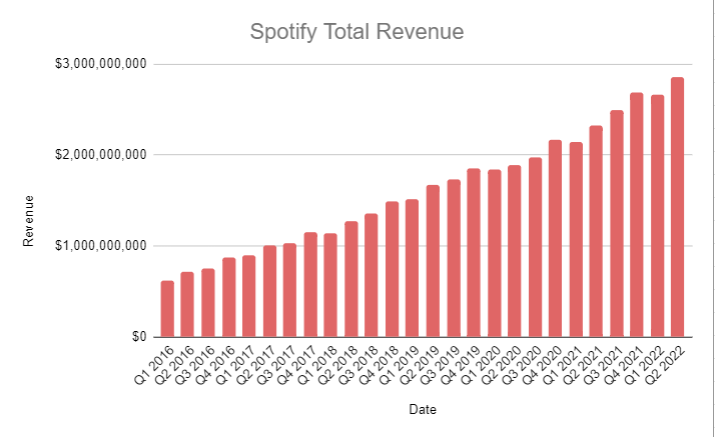

Premium music. This is Spotify’s subscription revenue. At the end of Q2, it had run-rate revenues of $10.25 billion and a gross margin of 28.8% (adjusted for accrual benefits and a one-time charge to closing Car Thing production). The majority of cost of revenue (COR) comes from royalty payments to labels, artists, and publishing rightsholders. Generally, royalty payments are calculated monthly and are based on a combination of a percentage of revenue and a per-user amount. Royalty payments are lower for Duo, Family, and Student plans and changes depending on country. From an investor perspective, there are two important things to know: royalty payments are approximately ⅔ of Spotify’s revenue, and the company has favored nation clauses meaning it has to give similar (if not the exact same) royalty deals to every label. COR also includes payment processing fees, customer support, certain employee costs, cloud computing, and certain equipment costs.

The main way Spotify’s premium gross margins will expand in the future is through its two-sided discovery marketplace (which we will expand upon in the next section). When a label/artist promotes their work on Spotify, the royalty payments as a % of revenue are lowered, which Spotify accounts for as a contra-expense in COR, therefore raising gross margins.

Advertising. Advertising revenue includes both music listening and other audio content (mainly podcasts). For music, the ad-supported revenue has the same COR as the premium business but historically has had worse gross margins that were generally in the teens. For podcasts, there are no royalty payments under the same agreements as music, but COR includes the amortization of Spotify’s content assets (both owned and licensed) and payouts to podcast publishers on its two distribution platforms Anchor and Megaphone. Currently, Spotify’s ad-supported gross margin is only 1.1% and has been depressed for the last two years as the company has ramped up its podcast spending.

The advertising segment can expand its gross margins with the growth of the Spotify Audience Network (SPAN, explained in detail in another section). This is the main way Spotify plans to monetize its ad-supported content, so if it scales up gross margins should expand as well.

(Ryan) Why do we think Spotify has operating leverage? What are the levers it can pull to expand margins?

There are basically 3 ways that we think Spotify can expand its margins in the medium-term.

Two-sided marketplace:

The larger Spotify’s platform gets the more valuable of a place it becomes for artists. Artists that want to grow their audience can do so by leveraging Spotify’s artist marketplace tools. Marquee, SPAN, and Playlist Inclusion.

Learn more about the two-sided marketplace on the Spotify for Artists website: https://artists.spotify.com/en/features

Growth of podcasts overall

Until podcast subscriptions are popularized, the bulk of podcasting revenue is going to come in the form of advertising dollars. And there are two ways that Spotify generates those ad dollars – SPAN and wholly-owned/exclusive shows.

SPAN (or the Spotify Audience Network) is an automated advertising marketplace that leverages Spotify’s streaming-ad insertion technology. So for example, if I’m an advertiser, I can sign-up, pick a budget for my ad campaign, select the target audience I want (20-30-year-old males who are in their cars and are interested in business), and then select the ad inventory I’m looking for (ad-supported music or podcasts). Then that ad will be run automatically in any available ad slots. SPAN is likely high 30% to low 40% gross margins.

Wholly-owned and exclusive is much simpler. Spotify has acquired several podcast studios and licensed several shows in its push into the podcast business. Each of those shows generates its own revenue which Spotify collects. This ad revenue is essentially pure margin, but they require higher fixed costs (paying for exclusivity, salaries for employees at the studios, etc.).

Audiobooks:

Spotify finally closed on its acquisition of Findaway this quarter. Findaway is an audiobook distribution platform much like Megaphone and Anchor are for podcasts. Though it’s unclear how audiobooks would be included on the platform (a higher-priced tier, a la carte, or ad-supported), Spotify pegged its gross margins from this segment at 40-50%. So regardless of size, assuming they’re correct in their margin assessment, this should be a net benefit.

(Brett) What are its podcasting initiatives? How will this impact the business?

Starting three to four years ago, Spotify started heavily investing in the podcast industry. At the start, they only had a few hundred thousand podcasts available. At the end of Q2 2022, there were 4.4 million podcasts available on Spotify, and it is estimated that the platform is now number-one in market share, slightly beating competitors like Apple Podcasts and YouTube, in many markets around the globe.

So how did this happen? Spotify has a three-pronged strategy for user acquisition and growing podcast hours played:

Buying studios. Over the past three years, Spotify has purchased The Ringer (~$200 million), Gimlet (~$230 million), and Parcast (~$50 million). These are three popular podcast studios that helped bolster the amount of content it has full control over. The majority of these shows are available across all podcast players (for now), with Spotify mainly monetizing through advertisements.

Licensing top shows. Spotify’s most well-known strategy has been to license popular podcasts to go exclusive on Spotify, most notably The Joe Rogan Experience, Call Her Daddy, and Armchair Expert. The company is spending hundreds of millions on these deals, which some investors may scoff at because the ROI looks unpromising when you just consider the advertisements that can be run on episodes. However, we like to look at these deals holistically. These can be great customer acquisition tools to convince tens of millions of listeners around the world to choose Spotify for their audio needs. Spotify can then make money by upselling them a premium subscription or convincing them to listen to all their podcasts on Spotify. While hard to parse the data, we believe this has been a key way Spotify has been gaining market share from all other podcast competitors.

Owning the distribution and technology. Spotify has made multiple acquisitions in podcast distribution (Anchor, Megaphone, Whooshka) and podcast technology (Chartable, Podsights, Podz) companies. These will serve as the backbone for both 3rd-party distribution and building the advertising business. For example, the podcast you are listening to right now is distributed through a Spotify-owned entity. Megaphone is one of the leaders for premium podcast publishers, while Anchor covers the long tail of smaller shows. Anchor powers roughly 75% of podcasts on Spotify.

So Spotify has invested over $1 billion in building out a podcast content and distribution ecosystem. How does it plan to monetize and get a good return on investing capital? By building a targeted advertising business.

This is what we were referencing with SPAN above. SPAN was launched around a year ago with the goal of combining all forms of ad-supported content on Spotify (music and podcasts) for advertisers to spend money. The difference between SPAN and historical podcast advertising is twofold. First, advertisers do not have to directly go to every show or advertising agency to get the word out. All they have to do is record the advertisement and set a budget with Spotify. Second, SPAN will be able to target listeners to improve advertising efficacy. For example, many sports shows currently advertise sports gambling stuff globally, even though it is illegal in a lot of regions. There is a ton of wasted advertising here. SPAN will (hopefully) fix this inefficiency by directly targeting listeners with advertisements, therefore improving the ecosystem for listeners, advertisers, and shows. And of course, Spotify will be taking a cut of the revenue.

Because SPAN is barely a year old and a lot of Spotify’s podcast investments are categorized in COR, advertising gross margins have plummeted, as we mentioned above. We will be looking for a full roll-out of SPAN to all Spotify distribution platforms (especially Anchor) and to more regions internationally (currently only available in English-speaking markets) as signs that demand for SPAN is increasing from advertisers. With fewer variable costs than the music business, gross margins should expand if advertising revenue continues growing at a 30%+ rate.

(Ryan) Does Spotify have a moat?

It might be overly optimistic to say that Spotify has a clear moat, so I’m going to say no. But what is clear, however, is that Spotify has a superior user experience and that’s demonstrated by the numbers. Over the last several years, competitors of all kinds have offered significant discounts on their platforms, including:

Free Youtube Premium Music with a Youtube Premium subscription.

6 months of Apple Music for free with the purchase of Airpods, Beats, or the Homepod.

Amazon Music free with a Prime membership (half of Americans are Prime members).

Yet amidst all of these offers, over the last six years, Spotify has increased its total monthly active user count from 104 million to 433 million – far more than any competing service globally and even 1.6x more than Apple Music in the US.

Additionally, Spotify generates more engagement than competing services and monthly active churn is significantly lower than all other peers. If the content library is largely the same across all services, what could possibly be driving Spotify’s relative success? It has to be a better user experience.

(Brett) How are we valuing Spotify today?

Before diving into our financial projections, we should note that forward estimates and complicated discounted cash flows are not a huge part of our investing process. We care about identifying a competitive advantage and industry durability (moat), evaluating management (do we trust them?), and whether the stock is at a reasonable price. Of course, evaluating whether a stock is at a reasonable price requires making some sort of projections about future cash generation, but we just find it foolish to put any precision on the numbers.

With that being said, here are some of the rough numbers we put together for our report on Spotify a year ago. We actually may disagree with some of these numbers which we can discuss for how we would update the model.

First, let’s look at the premium business. Our estimates are that premium subscribers will grow by 10% a year through 2030, gross margins will steadily expand to 36%, and average revenue per user (ARPU) will grow by 3% a year. The ARPU number may shock some people, but we can discuss why we believe Spotify will have consistent pricing power, enabling it to raise prices by 10% or so every few years.

For the premium business, these numbers equate to $6.2 billion in gross profit in 2026. Given Spotify’s propensity to reinvest for growth, it is unclear how much of this gross profit will be converted to operating income/cash flow. But whatever the exact number is, we believe tons of value is getting created for shareholders nonetheless.

For advertising, our projections are for 30% revenue growth through 2030 (remember, this is generally from a low base) and gross margin expansion to 48% by 2026. This equates to $2.3 billion in gross profit from advertising in 2026 which will balloon to $8 billion by 2030.

On a consolidated basis, we believe Spotify has a clear path to generating $7 billion - $9 billion in gross profit annually by 2026 that will flow through to $3 billion - 4$ billion in operating income (free cash flow will generally be slightly higher than OI, due to the permanent working capital advantage).

At a market cap of $22.7 billion today (and close to $40 billion - $45 billion a year ago), we think Spotify is trading at a reasonable price vs. the cash it can generate five years from now.

What would we revise here? (discussion during the episode)

(Ryan) What do we think of management?

It seems to us that there are three important executives at Spotify. Daniel Ek, Gustav Söderström, and Paul Vogel.

Daniel Ek: Daniel is the founder and CEO of Spotify and has been steering the ship since the beginning in 2006. Daniel pioneered music streaming as we know it and navigated Spotify through stiff competition while managing to keep all stakeholders happy. Daniel also owns 17% of the shares outstanding, which gives us a sense of alignment knowing he’ll do what he thinks is right for shareholders over the long term.

Gustav Söderström: Gustav is the Chief Product Officer, and in our opinion, is the most likely successor to Daniel if he ever decides to leave. From the outside looking in, Daniel appears to be focused on the big picture while Gustav is more hands-on and focused on the day-to-day.

Paul Vogel: Paul was promoted to CFO in 2020 after joining Spotify in 2016. Paul’s capital allocation principles seem to align well with Daniel and Gustav’s approach to running the business – invest in the business first because the opportunity is simply too large not to.

Assessing Bear cases:

(Brett) Spotify is a commoditized service providing content that they don’t own. They’ll never be able to expand margins because of that.

This is clearly true (from a music perspective) when taking the products at face value. The music catalogs are 99.99% similar across Apple, Amazon, and YouTube. However, there are multiple indicators we are seeing that Spotify’s service is not a commodity. I’ll speak on two. First, management has said its users engage 2x - 3x as much compared to competitors. If the services were the exact same, why would that be? Second, and this plays off of the higher engagement, is the focus on helping users discover new music to listen to. According to its last update, users discover 16 billion new artists each month on the service, which is just an example of how much value it provides to its hundreds of millions of users. This, in our mind, is where the long-term competitive advantage comes from and why churn is so much lower than competitors.

(Ryan) Heavy competition from Apple, YouTube, and potentially Tik Tok.

The threats from Apple and Youtube have largely been dismissed through execution. As for TikTok, it’s hard to say. TikTok’s parent company Bytedance recently filed to trademark “TikTok Music”. While TikTok has demonstrated how good they are at discovery, there still seems to be some segmentation from consumers around what you do in apps, particularly in western markets. Additionally, TikTok has already launched a music streaming service in Brazil, India, and Indonesia and Spotify is still seeing great adoption in those areas.

(Brett) The Podcast market opportunity is not large enough and/or too fragmented

There is a real concern that Apple Podcasts and others retain market share while smaller advertising marketplaces win advertising spending. This is happening right now to some extent. But there are two reasons we think Spotify can overcome these concerns and become the vertically integrated podcast advertising giant we are projecting. First, with its continued focus on podcasts, it has won market share each and every year vs. Apple Podcasts since the medium launched on Spotify in 2018. There’s no indication this trend will stop anytime soon. Second, with better first-party data, scale, and the only true vertical integration in the industry, Spotify should be able to offer better advertising services (to both podcasts and advertisers) through SPAN compared to the niche marketplaces. Over time, we will see this play out if advertising revenue continues to grow at a high rate.

(Both) Speculative discussion on Audiobooks, Live, and other non-podcast/music categories

(Both) What do you see as the most realistic risk that Spotify ends up being an underperforming investment?

(Brett) I have two risks that I will be watching over the next few years as threats to Spotify’s ecosystem. On premium/music, the threat of a global music streaming app from Tik Tok (all the other competitors don’t concern me seeing as they haven’t slowed down Spotify so far) could hurt MAU growth and churn. Why? Because Spotify’s core differentiator on music is discovery, which Tik Tok is extremely good at. Second, on podcasts, I worry that the advertising market and possibly the entire addressable market is smaller than Spotify believes it is. This will lower the ROIC from all the money it has spent, which we outlined above. For example, podcast costs are generally growing faster than revenue right now. I think this will change, but there is a risk it doesn’t. We haven’t seen either of these risks materialize yet (with Tik Tok it will show up in MAUs, podcasts it will show up in advertising revenue growth), but they are both something to track.

(Ryan) I’ve got two as well.

First risk: Podcasts don’t work out and the value proposition for advertisers isn’t as compelling as other destinations. For the time being, podcast ads are skippable which isn’t all that enticing for advertisers and measuring the return on a marketing campaign isn’t that easy since there isn’t really a direct click to tell you where they came from. Though Spotify is working to improve this, it’s mostly brand advertising for the time being as opposed to performance marketing.

A second risk: Despite gross margin expansion, 10% cash flow margins (or anywhere close) never materialize. In this scenario, it’s likely that profitability would constantly feel theoretical due to management’s choice to reinvest the cash at their disposal into areas that aren’t needed. They’ve made several acquisitions like this that concern me. LockerRoom (live audio), Sonantic (text-to-speech technology), and Whooshka (radio-to-podcast) are the first three that come to mind. But so far Podsights and Chartable would fit that mold as well.

Sources and Further Reading

We’re Doing Much Better Than You Think - The Science of Hitting (Paywall)

Spotify Finds a Way Into Audiobooks - Sleepwell Strategy

Music Streaming Royalties 101 - Sleepwell Strategy

An Audio Lollapalooza - Our Write-up from September 2021