Remitly Global: Tipping Point?

Scale, increasing competitive advantages, and reinvestment runway

YouTube

Spotify

Apple Podcasts

*Make sure to check out our latest podcast, links above.

Remitly Global — one of the few stocks I bought in 2024 — reported Q4 earnings last week.

The stock dropped 10% after the report. It is still up around 75% in the last six months. I thought the report was impressive, adding more to my conviction in the company’s growth prospects. I plan on adding to my position soon.

Here’s why.

Decreasing costs at scale

Here are the headline numbers from Remitly’s Q4:

33% YoY revenue growth

7.8 million active customers, up 32% YoY

39% growth in send volume

Record gross margin of 60%

Slight net loss

As Remitly enters more corridors around the world, obtains better deals from payment/banking partners, and achieves more scale, its gross margins improve:

What makes this gross margin expansion impressive is that simultaneously Remitly is lowering its costs for customers. Send volume grew 39% year-over-year last quarter, while net revenue (what Remitly keeps as a take rate) grew 33% year-over-year.

Costs for customers went down. Gross margin went up. While not apples to apples, Remitly is in a position where it can consistently reduce the cost of remittances, keep some of these savings for itself AND simultaneously pass on these savings to customers. That sounds like economies of scale to me.

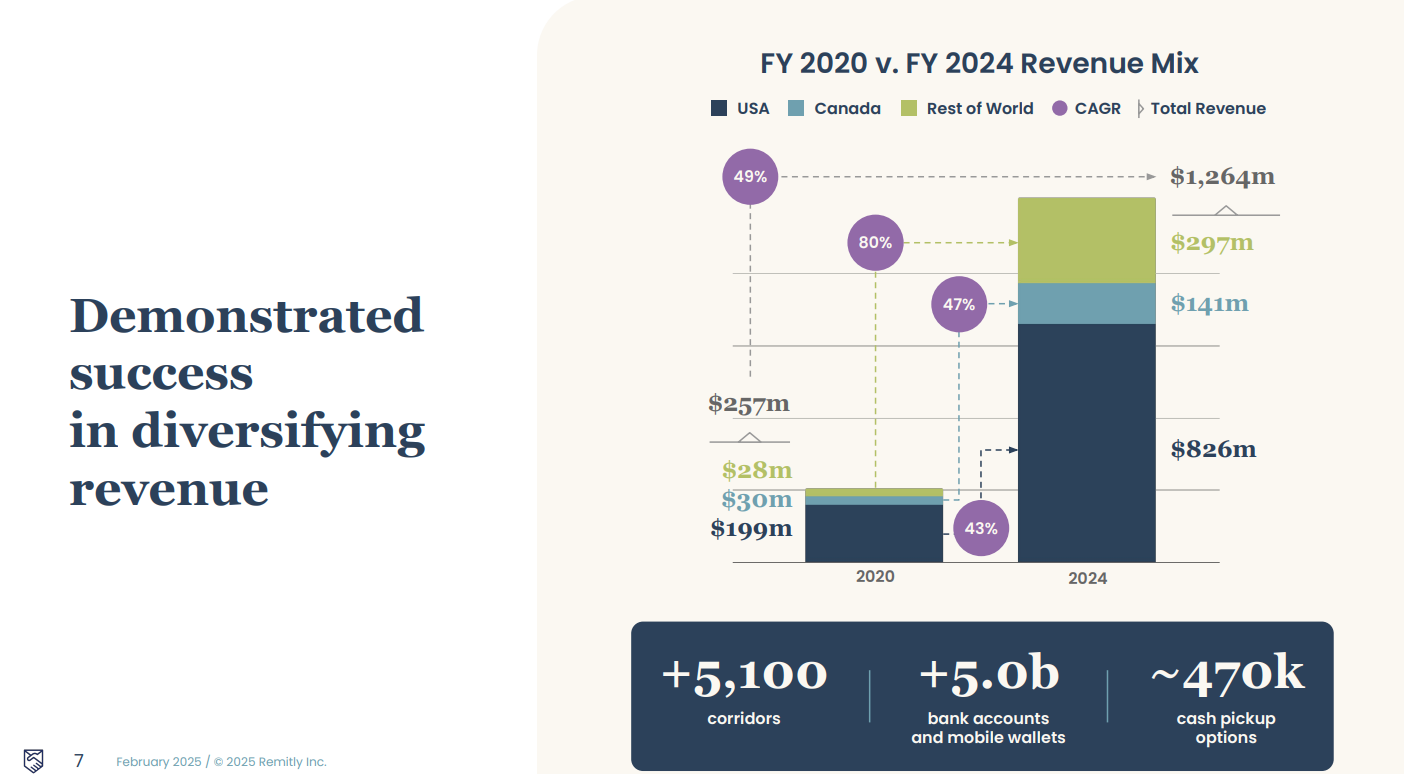

Don’t forget that unlike Wise (which isn’t a true competitor), Remitly serves over 500k cash pick-up locations around the world. This is not an insignificant cost, but improves the value proposition of the Remitly service.

Of course, we can’t forget the economies of scale coming from scaled global marketing spend. Outlined by fellow long Mario Cibelli, Remitly’s digital-first systems and scale give it a competitive edge vs. legacy peers (i.e. Western Union) and any start-up.

Its product is simply better and difficult to replicate, no matter how much money is thrown at the problem. Management is not resting, either. There is plenty of runway left to reduce costs, expand to more corridors, and add on adjacent personal finance tools (like Remitly Circle).

With this advantage, Remitly has the ability to deploy billions of marketing dollars over the next 10 years with fantastic return on ad spend (ROAS).

To illustrate, in 2024 Remitly spent $304 million on marketing. In 2019 it spent $43.5 million.

In 2019, marketing dollars were 34% of revenue. In 2024, it was 24% of revenue. Five years from now, I expect Remitly’s nominal marketing spend will grow to $1 billion while marketing spend as a % of revenue will decrease to 20%.

Have we hit a tipping point?

As of Q3 2024, Remitly was just 3% of the global remittances market. It is still a minnow compared to Western Union.

Given the competitive edge outlined above and management’s sharp focus on scaled marketing with good ROAS and decreasing remittance costs, I think Remitly is hitting a tipping point in global adoption.

Remitly has a chance to deploy a lot of marketing dollars in the next few years. Its target customers will switch to and stay with Remitly because it is the best product on the market. This will lead to consistent revenue growth, gross margin expansion, and eventually leverage on the operating income line.

Ask yourself: what is stopping Remitly from hitting 10% market share in remittances? 25%?

Undemanding valuation

According to our friends at Finchat, Remitly currently has a market cap of $4.8 billion. It is a serial diluter with stock, so let’s say dilution would bring us to a market cap of $6 billion in five years (also assuming any excess cash flow is spent on buybacks, just to simplify the model).

So you have a $6 billion market value today. Okay, well what could Remitly earn five years from now?

I think they can easily surpass 10% market share in global remittances. With the remittance market growing, protection from inflation, and the add-on products such as Remitly Circle, I think revenue can 4x to over $5 billion.

If you chop off $2 billion for fees, $1 billion for marketing, and $1 billion for product development and G&A, that leaves you with $1 billion in operating income.

I think this $1 billion in operating income would be valued at $20 billion, if not much more given that Remitly will have greatly increased its moat and will still have a long runway to grow in 2030. I wouldn’t be shocked if it was valued at $40 billion (depending on broad market sentiment, of course).

Even if the company falls short of these estimates and we hit a bear market, the stock is still wildly attractive here. This is why I plan on adding up when I deposit new cash into my brokerage account.

-Brett

Chit Chat stocks is presented by:

Public.com has just launched its BOND ACCOUNT. Lock-in interest rates of 6% or higher (as of 9/30/24) by signing up today!

With as little as $1,000, the bond account allows you to buy a diversified portfolio of bonds and lock in your yield even if the Federal Reserve cuts rates.

It only takes a couple of minutes, get started today at Public.com/chitchatstocks and open up a bond fund today!

A Bond Account is a self-directed brokerage account with Public Investing, member FINRA/SIPC. Deposits into this account are used to purchase 10 investment-grade and high-yield bonds. As of 9/26/24, the average, annualized yield to worst (YTW) across the Bond Account is greater than 6%. A bond’s yield is a function of its market price, which can fluctuate; therefore, a bond’s YTW is not “locked in” until the bond is purchased, and your yield at time of purchase may be different from the yield shown here. The “locked in” YTW is not guaranteed; you may receive less than the YTW of the bonds in the Bond Account if you sell any of the bonds before maturity or if the issuer defaults on the bond. Public Investing charges a markup on each bond trade. See our Fee Schedule. Bond Accounts are not recommendations of individual bonds or default allocations. The bonds in the Bond Account have not been selected based on your needs or risk profile. See https://public.com/disclosures/bond-account to learn more.