Sunday Finds + 3 Thoughts From Last Week

Covering tobacco and a fire safety roll-up this week. Buckle up!

Welcome to Chit Chat Money’s Sunday Finds + 3 Thoughts From Last Week. In this newsletter you will find three topics I thought about last week, links to shows we’ve recently released, and links to some interesting articles, podcasts, and tweets. Check out the archive here.

Chit Chat Money Podcasts From Last Week

Chit Chat Money is presented by:

Stratosphere.io, a powerful web-based research terminal for fundamental research. With fundamental charting tools and data aggregation, Stratosphere saves us hours of time each month researching stocks.

Upgrade to one of Stratosphere’s paid plans and get 35+ years of historical financials, advanced KPI tables, and SEC filing aggregation.

Ditch the clunky and advertising-riddled websites like Yahoo Finance and upgrade your investing research using Stratosphere.io.

Get started researching for FREE on the Stratosphere.io platform today, or use code “CCM” for 15% off any paid plan.

1. American Express customers continue to spend

Don’t tell Amex cardholders a recession is “imminent”:

Spending at restaurants continues to be a bright spot with growth accelerating to 28% on an FX adjusted basis year-over-year. In fact, March was a record month for reservations booked through our Resy platform. The platform now has more than 40 million users globally, an increase of 5 million in the last six months.

This was from Amex’s Q1 conference call. They are seeing similar growth in airlines, hotels, and their overall travel & entertainment (T&E) spending line.

28% growth in spending at restaurants does not sound like a consumer that is feeling pinched. Maybe we all underestimated the impact of consumer savings during the pandemic?

The personal savings rate was well above 15% for a full year, more than triple the long-term average. While one would hope people would save this money for a rainy day, the reality is that American people are going to (on average) spend what they have in their bank accounts.

Looking at these Amex numbers, people are trying their darndest to blow through these savings as fast as they can, but if you run a simple estimate they should have plenty of quarters left of “dry powder.” Once all this dry powder normalizes, I think it is plausible that home/car prices continue to decline. Wouldn’t be surprising to see some deflation in CPI, either.

Not that it really matters over the long term, but I have a hunch that Wall Street overrated the potential for an economic downturn by extrapolating what was happening in tech/software/start-ups to the rest of the population. This is one of those situations where anecdotes can greatly mislead you. The data is much more insightful. And surveys of 1,000 people don’t count as data, either…

Look, things can change on a dime with consumer spending, but I don’t think you can look at this Amex report and think “Wow, the economy is in shambles.” In fact, it looks like the majority of Americans are in great shape financially.

Visa/Mastercard earnings next week will either sharpen or hurt this narrative.

2. Three easy ways for Netflix to juice margins

Netflix’s content spending is going to flatline from 2022 - 2024, according to management. Obviously, this is subject to change, but I think it sets up the company to start generating very healthy amounts of cash flow from 2024 onward.

This will be done through its three incremental monetization tactics: better international pricing, advertising tiers, and limiting password sharing.

Netflix is lowering its pricing in many international markets, has launched an ad-supported tier with better per-user revenue than its non-advertising tier, and is going to slowly crack down on password sharing over the next few years.

If (big if!) they can retain current subscribers without growing content spending, these three new initiatives will have very high incremental margins.

Sure, there are some COGS and marketing spending to drive new accounts, but even very low-priced subs in poorer countries can be profitable due to their fixed content costs. 10 million new accounts that pay $4 a month (roughly $50 a year) is $500 million in high-margin revenue. Bring in 15 - 20 million high ARPU accounts from advertising tiers and password sharing and I could see Netflix adding $3 billion - $4 billion in annual cash flow just from these monetization tweaks. Again, as long as content spending stays flat.

The question is, however: how much will the password-sharing crackdown hurt its brand reputation? It is clearly going to cause some noise (I can already smell some sensational blog posts about to go viral) but I think in the long run customers will understand that Netflix is not going to let them freeload on the content they spend billions of dollars each year to produce.

If I had to make a bet, I would guess that Netflix’s free cash flow is above $10 billion in 2025. Sorry to jinx things, bulls.

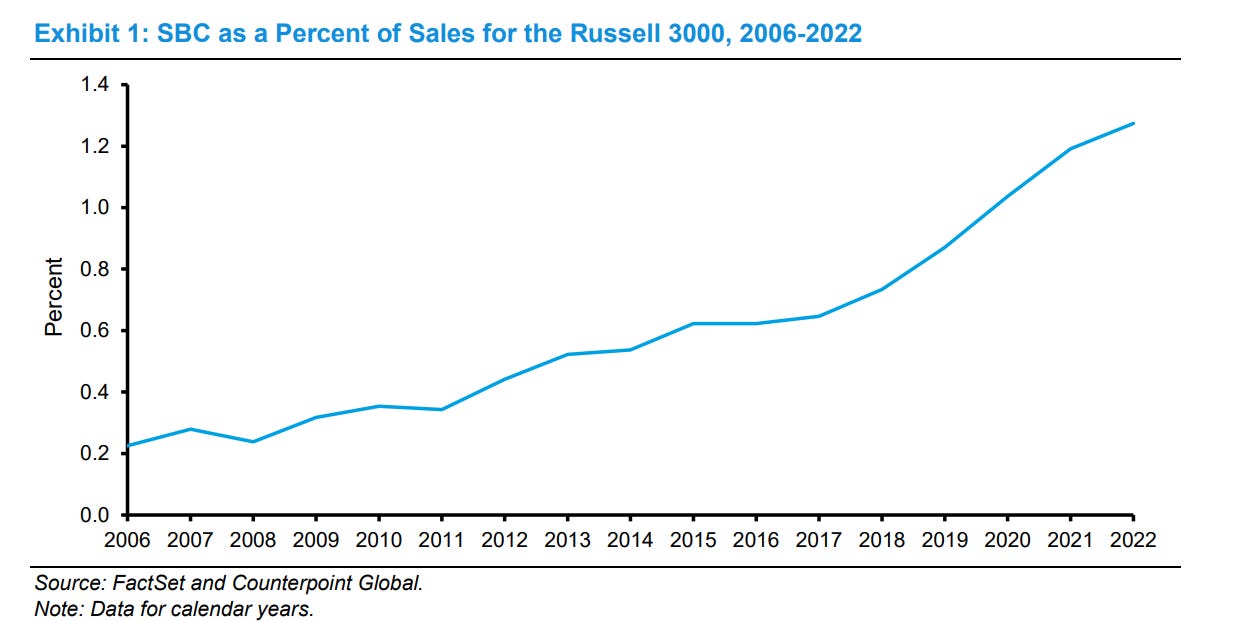

3. Mauboussin on Stock Based Comp

“They are who we thought they were!”

A Mauboussin paper on stock-based compensation (SBC)…yeah there’s no way I’m missing this:

The Russell 3000 is an index that tracks the largest stocks by market capitalization in the United States. We estimate that SBC was about $270 billion in 2022, or 6- 8 percent of total compensation for public companies in the U.S.

I love this paper because it confirms all my biases. SBC has gone up over time, is undervalued by employees, and doesn’t actually “align incentives” like every proxy statement tries to say. There is also a clear ratcheting effect where every company increases SBC because every company is increasing SBC.

I mean for goodness sakes:

For example, a survey of financial executives found that 68 percent indicated that offsetting dilution from SBC was “important” or “very important” in their decision to buy back stock.

I wish more profitable large caps completely avoided SBC. It is so much cleaner…for all stakeholders. And, well, it is idiot-proof.

“I did it. Your parents are gonna do it. Break the cycle, Morty. Rise above. Focus on science cash comp.”

See you next week,

Brett

***Our fund, Arch Capital, may own securities discussed in this newsletter. Check our holdings page and read our full disclosure to learn more.***

***Want our FREE weekly wrap-up delivered to your inbox each week? Subscribe here***

3 Good Reads

Despite the sound, fury and personal drama, in a strictly business sense . . . not much has actually happened. Still, it has got a bit confusing, and even seasoned financial analysts or FT columnists could be forgiven for losing track of things. So FT Alphaville sat down for a fevered quasi-binge of the show and tried to make sense of Succession’s financial plotline(s).

What Was Twitter, Anyway? - New York Magazine

The trouble began, as it usually does, when I saw something funny on my computer. It was the middle of the morning on a Wednesday, a few years back, and I came across news that Le Creuset, the French cookware brand, had made a line of “Star Wars”-themed pots and pans. There was a roaster made to look like Han Solo frozen in carbonite ($450) and a Dutch oven with Tatooine’s twin suns on it (“Our Dutch oven promises an end result that’s anything but dry — unlike the sun-scorched lands of Tatooine”; $900). A set of mini cocottes had been decorated to resemble the lovable droid characters C-3PO, R2-D2 and BB-8.

The Vanishing - Tablet

When activists and journalists and executives talk about how Broadway or NPR or publishing is “too white,” what they really mean is “too Jewish.” When The New York Times says it wants to make its internal demographics look more like New York City’s (excepting the Hasidim, of course), what this means is “fewer Jews.” Twenty years ago, if Pat Robertson spoke along these lines—making the same complaints about the same people and industries and institutions—there would have been a rush to condemn it as antisemitic. Today it passes for social justice.

1 Good Podcast

Smart, Insightful, and Funny Tweets:

So many big "ifs" in the NFLX bull case. The stock has been bid up in anticipation of future revenues from their ad tier and paid-sharing subscriber growth. The promise of both these future revenue streams is yet to be understood, proven and accurately estimated. As an investor, I would not buy it here. As a trader, I would short the stock now.

One analyst on SA said it best a few months ago, “Netflix is a media company in a mature growth stage, and unfortunately, it is being priced like a technology company in hypergrowth.”

If I want to invest in the adtech promise of streaming, I would rather own an SSP or DSP company that earns a piece of the ad revenue pie irrespective of who is advertising and where.

Cheers!